Can't keep extending and pretending forever, right?

Some signs that everything is A-OK, and some signs that everything is about to burst . . . but at some point, we gotta stop pretending, if we're gonna declare victory . . . right?

I did a little extra buffing and polishing on this, so it’s a little late

recapping the “extend n’ pretend” bag o’ tricks

it all makes sense, and it’s working great—lenders were prepared

at some point, pretend has to end, presumably when things go “back to normal” (but that hasn’t happened yet)

are we delaying the pain trade or being adaptable and resilient? a review of the recent anecdata and spidey-senses

real estate creaking again?

‘higher for longer’ or he that shall not be named

everyone’s a debt scold now

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Can’t keep extending and pretending forever, right?

One of the ongoing wonders of the ‘higher for longer’ era is how resilient private capital markets have been, which includes both privately-owned companies, and their investor/sponsors.

The idea was that when rates went up all these companies (and their investors) who nourished themselves on cheap capital would go belly up.

But it didn’t really happen.

I mean, it happened a little. Certainly startup closures accelerated, bankruptcies have grown, a lot of real estate was sold for a loss, and some banks went under (or were rescued), just to cite some examples, but for the most part, things have been fine. Liquidity-challenged, but fine.

Are funds returning money to investors? Still, no. The bid-ask is still too wide, so unsold companies continue to pile-up on the books of mature funds.

Can funds raise new capital? Again, not so well, outside of the biggest few, or at least it’s quite challenging, and certainly lots of recent VC appear to be out-the-game (which’ll happen when you don’t return any money from the previous fund).

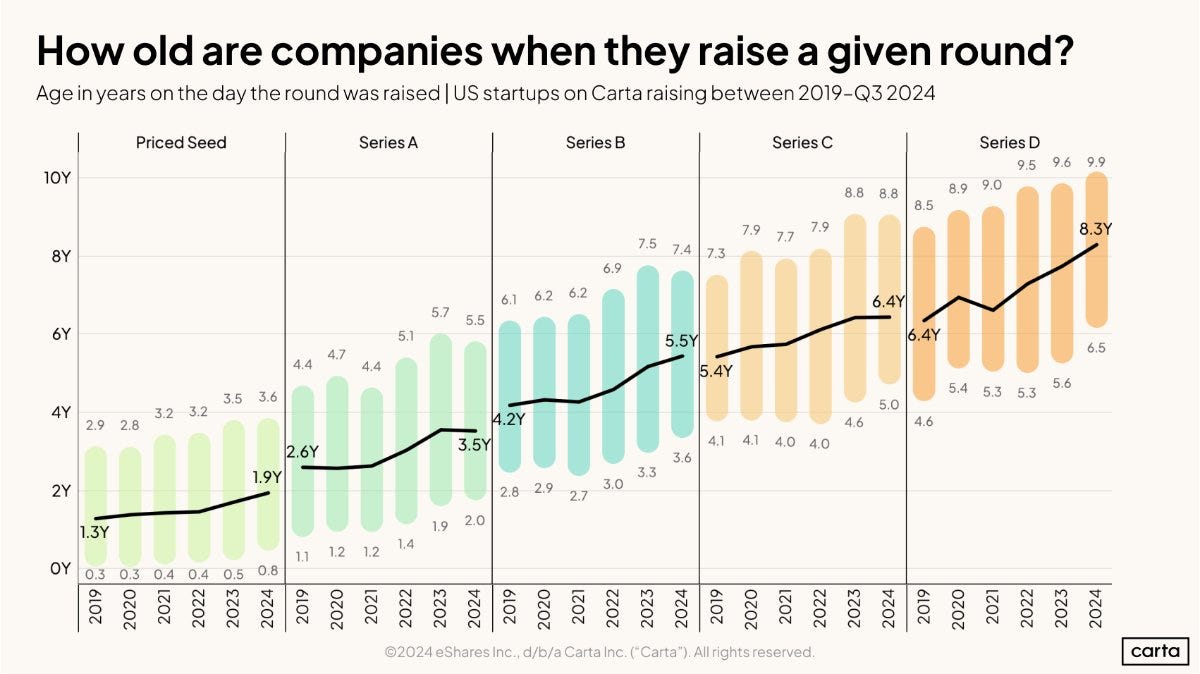

Are companies going longer between rounds? Yes, absolutely.

Startups are extended their own runways.

So there are definitely some challenges.

But this is nothing like the reckoning that many (Random Walk included) expected.

Extend n’ Pretend, bag o’ tricks (recapped)

Part of why the reckoning has been avoided is because the people who run and fund these businesses are quite clever and adaptable.

They’ve deployed a grab bag of can-kicking exercises, variously under the header “extend and pretend.”

Oh, that commercial mortgage is maturing? We’ll refinance and restructure, rather than foreclose. Can’t make a payment? Just call-it a PIK day.

The banks aren’t lending to you anymore? Try one of the private credit shops—it’s a bit more expensive, but they’re very easy to work with.

Ah, you’ve tripped some debt covenants? That’s ok—we’ll do a Liability Management Transaction or perhaps a Distressed Exchange instead of bankruptcy. What’s your dish? You tell us.

There’s no exit market for your portcos? You’ll love a continuation fund.

What’s that? Your LPs demand liquidity? Have you considered secondaries, or better yet, dividend recaps and/or NAV loans?