A change is gonna come

Are consumers getting complacent? Hopefully not because things are definitely not the same as before

Random Walk is bringing back the long form, so buckle up. There are two parts:

Don’t Get Complacent, a little check-in on the state of things, which depending on your perspective, are either not as they seem, or totally as they seem; and then

Turn and Face the Strange, six big things that will (continue to) be different than before. A sort of “gather my thoughts” on the the various non-fleeting stuff that define (in part) the new normal.

They’re both great. But . . . one of the downsides of trying to resist the urgency of the news cycle is, of course, that not every aspect of what follows reflects all the inputs from the most recent news cycle. Hopefully the extremely informed will forgive me.

Things we think

Don’t get complacent

Heating up?

The recentish macro news was that inflation heated-up slightly, after a few months of welcomed cooling. Higher prices were really driven by the general “services” category (i.e. wages):

Food too remains persistently pricey, but that also reflects services and energy costs:

Despite higher prices, consumers were back in the game, spending ~1.1% more than they did a year before (even on an inflation-adjusted basis).

That prices went up, and consumers still increased their spending by ~1% YoY has people scratching their heads (or rushing to conclusions) . . . normally people spend less when things get more expensive, unless they’ve gotten a lot richer, and that does not appear to be the case.

So what gives?

Nah, just a head fake

Random Walk agrees that it’s a bit puzzling, but at some level, it’s just the push-me-pull-me of the Goldilocks Landing. Prices were up, so consumers pulled back, which meant prices went down, so consumers piled back in, and so on and so forth. I would expect consumers to pullback a bit now that they’ve gotten a little spending out of their system, and so far, that appears to be the case (although woh, services):1

In other words, the “heat up” is a headfake, and while the Fed Chairman threatened to bring more heat, I don’t think we’re going to need it. It’s also true that there other indicators still consistent with a general slowdown (e.g. shipping and manufacturing demand) and the pain of higher rates is triggering all kinds of stress signals. [Update: Major banks going belly up? Yeah, we got that.]

In all events, keep your ‘lectric eye on me, babe

The alternative (and concerning) scenario would be if some complacency has set in.

It occurs to me that outside of car- and house-buyers, consumers haven’t really directly experienced the impact of higher interest rates, just yet. They’re still employed, they’ve still got savings, and things have been so good for so long, that perhaps a “this too shall pass” mindset presides.2

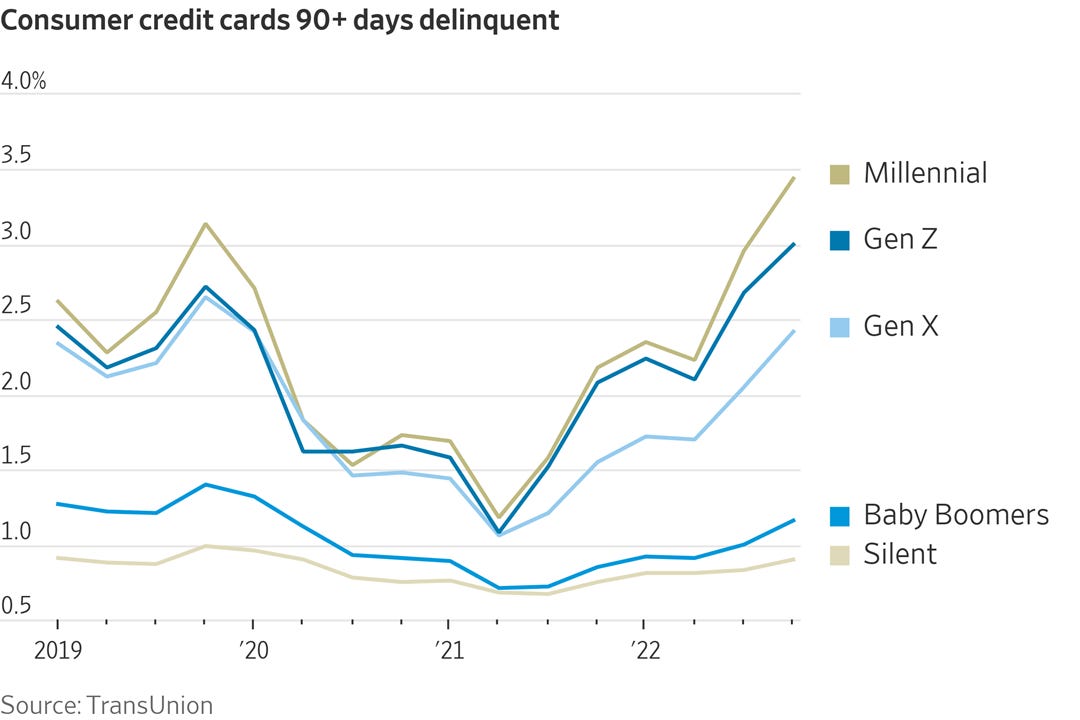

A consumer might say, “it’s OK that I’m carrying a bit more credit card debt than usual—I’ll just pay it back next cycle, or I’ll borrow a bit more home equity, but there’s no need to moderate my spending all that much.” And so, credit card (and other) delinquencies (which are pricier than they were before) are creeping up:

“Luxury items? Sure, of course I plan to buy luxury items . . . why wouldn’t I buy luxury items?”

Here’s the thing, though: money is ~4-8 times more expensive than it was before (depending on who you buy it from), and the price-increase has happened with unprecedented speed:

That’s a big deal. A very big deal. And the fact that consumers haven’t really internalized it yet, doesn’t make it any less true (and, as Random Walk has offered many times in the past, an attenuated feedback loop is an unreliable feedback loop).

At a certain point, that cost will be passed on to consumers in more ways than just houses and cars (although that itself could be enough). If not gradually, then all at once. To speculate, perhaps . . .

investors will eventually decide the “risk free” rate of Treasuries is too tempting to ignore—particularly as earnings continue to decline—and, not only does the stock market go south, but the higher cost of capital leads to layoffs (and insolvencies);

the rising costs of debt (on houses, cars and credit cards) leads consumers to finally appreciate that they are poorer than before, and regret the fact that they didn’t cut their spending sooner because now they’re in trouble and really must cut their spending, with no relief on the horizon;

some large financial institution (or species of institution) finally blows up due to “unforeseen” exposure to bad loans in both consumer and real estate, and everyone freaks out because there’s nothing that reprices more quickly in a bear market than “unforeseen” risk.3

the construction pipeline finally clears (because who’s going to build with rates this high), and all the people who get paid to construct things are suddenly out of a job, perhaps having relocated to parts of the country where constructing things was the best game in town.4

Any and all of the above (just so I can say I was right later on)

The point here isn’t to doomcast. The point is that if rates are this high, things are not the same as before (more on that below). If people continue to act like things are the same, there will be an awakening, and likely a rude one. The only way for rates to not be this high (outside of a recession), is if prices stop increasing, which means that wage-growth needs to stop, which means there can be no raise to offset higher household expenses.5

People simply need to spend less, or else.6 At least until there’s some new source of growth or productivity, which we’re definitely going to need, sooner or later. The meantime doesn’t have to be terrible, but it’s unlikely to be very enjoyable either.

Turn and face the strange

In the spirit of “things are not the same,” Random Walk thought it appropriate to make some claims about enduring changes to the new normal—not the Availability Cascade variety, but the sort of things that will matter for at least the next 10 years (to pick something arbitrary). I think that these will be relevant (although they may feature less prominently in the news cycle), regardless if we have a hard landing, soft-landing or the ongoing middling middle. They’re happening and they’re a big deal.

None of these are new or even that controversial—in fact, most are extensions of preexisting trends—but somehow it feels useful to put them all in one place. Plus, RW has blathered ad nauseum about structural shortages of people, money and energy (“more with less”), so it was time for a slightly more itemized account of the implications.

For now, there are 6. Here's the list for the time- or attention-constrained:7

Keep reading with a 7-day free trial

Subscribe to Random Walk to keep reading this post and get 7 days of free access to the full post archives.