Banks are playing it safe, sort of

Daily Data: More exposed to non-bank lenders than anyone would like

In today’s dispatch:

banks are lending less

banks are also generating less revenue, and NIM continues to slide (for now)

are Zombie banks good?

bank exposure to non-bank lending is probably higher than Zombie would like

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Banks are playing it safe, sort of

After the Fed nearly killed the banks by torpedoing the value of low-interest loans—the only kind of loans the Fed really allowed for over a decade—there has been a lot of effort to make banks “safer.”

Consistent with that effort, banks have worked pretty hard to not-lend because that’s what tightening up generally requires.

Banks are lending less

Outside of consumer credit card lending, banks have substantially ceded lending to non-bank banks, i.e. Private Credit, who have largely thrived in the higher rate environment.1

Credit card lending tends to be seasonal, so when it went negative last quarter (as it often does), so did bank lending overall:

Q1 loan balances contracted for the first time since early 2023 (which was the thick of the banking crisis).

In fairness, Q1 is historically a slow quarter, because again, seasonality, but the 12m loan balance growth rate is lower than its been since 2014.

Point is that banks are, in fact, lending less.

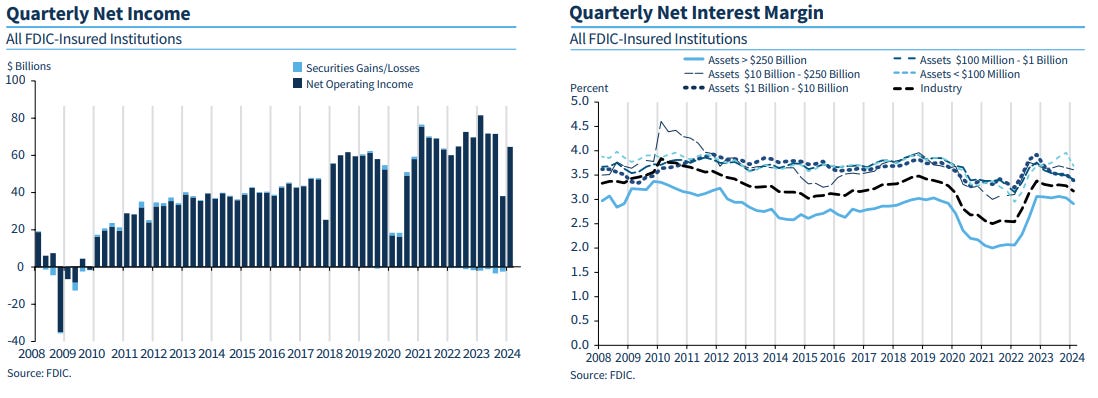

Lending less makes growing revenue hard to do

Of course, one thing about not-lending is that it has made it hard for banks to grow revenues (or balance-out all those low-interest loans they still hold).

Banks may have to pay depositors more, but they should be able to charge borrowers more too . . . except, if they are too busy not-lending:

Bank revenues are flat-to-down, and NIM continues to trend downwards.

OK, so banks are trying to be safer, which means taking less risk, which means getting less-reward.

This is all according to plan. There are tradeoffs in all things, and this is the sort of tradeoff one would expect.2

If banks become some zombies, is that good?

If safer, and less yieldy is indeed the future, it raises some open questions for the future of banks as we know them—if banks are unable or unwilling to find a market for higher cost loans, then they won’t be able to offset their higher cost of funding (and increase NIM).

Keep reading with a 7-day free trial

Subscribe to Random Walk to keep reading this post and get 7 days of free access to the full post archives.