Secondaries will not save VC (reprise)

An OG of VC secondaries weighs in, plus some actual data

Publishing note: Random Walk is going to experiment with a different publishing cadence over the next few weeks (more details forthcoming). I will endeavor to trade some frequency for depth, at least some of the time.

Random Walk has a few more posts on the state of the exit market lined-up (as well as Sohn recaps, and some White Collar Stagnation chartapaloozas). For now, briefly revisiting the VC secondary sich.

there isn’t enough secondary liquidity to go around;

actually, there is too much liquidity to go around;

an OG of the VC secondary market enters the chat;

some actual data on a seller’s market (but not in the way you’d think)

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Secondaries will not save VC (reprise)

A couple of weeks back, Random Walk wrote Secondaries will not save VC.

Without rehashing the whole thing, the gist of it is pretty straightforward.

There isn’t enough secondary $ to go around

Yes, it’s true that secondary markets for private equity (including VC) are growing at a robust clip, but it would be a mistake to view secondaries as some kind of white knight for the “liquidity crisis” (i.e. the lack of realized gains) in VC.

As per then:

Recently, “secondaries,” as a necessary part of the “exit strategy,” has been a hot topic in the VC ecosystem. It’s now become very important (according to VC), that VC have a secondary path as part of their route to exits—bc waiting for IPOs and M&A just won’t do “because liquidity.”

. . . Now, Random Walk is a big believer that secondary markets for private equity (i.e. the buying and selling of private company stock) are ripe for innovation and change. It starts with fund structures (and regulatory requirements), and better data and reporting. Plus, a lot more connectivity between VC (especially), and the rest of the capital markets . . .

But in this case, it should be clear that secondaries will not save VC, in the sense of “what are we gonna do with all our current investments.”

The reason that secondaries should not be viewed as a fix—however welcome they might be on a go-forward basis—is simple.

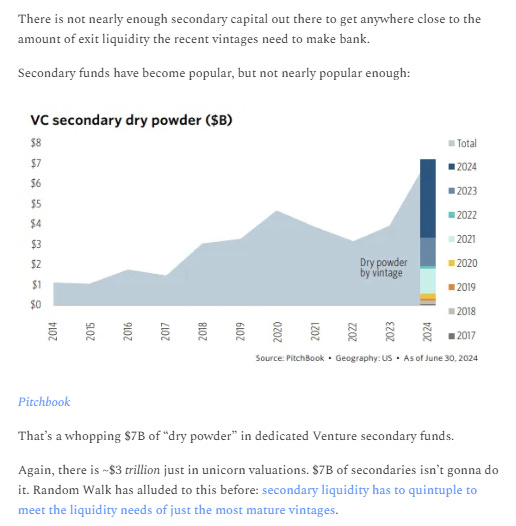

There isn’t nearly enough secondary capital to go around:

It’s going to take a lot more than $7B in secondary funds to unlock ~$3T in liquidity, and that’s assuming the public markets “return to [ab]normal.”

It’s not happening. I take no joy in saying it, but the only way forward is through.

Actually, there is *too much* secondary $ to go around

Random Walk had a little chat with Will Quist of Slow Ventures (“Unlocking Liquidity the Old Fashioned Way”), and Will made the additional point to the effect of “actually, there is no shortage of liquidity.”

There is, if anything, too much liquidity in the private markets. Private buyers have such deep pockets that companies have no particular need to go public.

That doesn’t mean that everything is fine and no changes are welcome.