Typoglycemia

Mini-essays on Typoglycemia and things are not as they seem; Start-me-up-start-me-down; Equality before the rates. Reads on Swifties, AI+Akkadian, New Glut City, Manufacturing is hard, Apple & GS

It’s toasty out there, so stay inside and read this instead.

Random Walk Thinks:

Typoglycemia or things are not as they seem

Start-me-up, Start-me-down (reprise)

Equality before the rates (or how interest rates do not effect everything the same all the same time)

Random Walk Reads:

The Economy of Taylor Swift

AI translates cuneiform

New Glut City

Manufacturing is harder than you think

Fintech is harder than you think (or how Apple and GS fell out of love)

So long to July, and a very happy birthday to my wife, who makes it easy for me because (among other things) all she’s ever wanted was a Random Walk shout-out.

Typoglycemia

There’s a genre of ChatGPT discovery called “jailbreaking.” It’s basically clever prompting meant to bypass the various guardrails against bad AI-ing. “Bad” can include wrong think—heaven forfend the robot offer a forbidden utterance—but also other unpleasantness, like writing malicious code or a how-to manual for getting away with murder. When decent people find jailbreak, they post about it and then usually the LLM shuts it down—it’s kind of like bug bounty hunting or whitehat hacking. When less decent people find a jailbreak, well, presumably they exploit it as long as they can.

Anyways, someone found a jailbreak that I thought was pretty neat (and posted about it, so presumably they’re the decent sort). The specific jailbreak they executed was less interesting to me, so much as the particular phenomenon they relied on to trick the AI, called “typoglycemia”:

I don’t know enough about linguistics (let alone large language models) to understand why exactly this works, but the fact that it works, is really cool.

So why mention it? Well, for one thing, learn new things. This is the RW way. For another, it sounds in a theme that RW has been pondering lately along the lines of “cognition and/or understanding does not work the way we generally assumes it does.” Like, if the modal assumption is (and I’m generalizing): “we observe data and then make reasonable inferences from such data to obtain meaning with various degrees of certainty” that’s really really not how it works, at least not nearly as often as we’d like to think.

It’s not a perfect application of the theme, but I always kind of assumed that “reading” followed some linear(ish) application of sounds to word to comprehension. Now, it seems, that is most definitely not the case (at least not once we actually learn how to read). I guess that makes me wnorg and rghit at the smae tmie. I’ll take it.

Start me up start me down (reprise)

Here’s another neat little visualization of the slowdown in venture funding:

Funding is off-trend at every stage.

At the very early stage, the picture is mixed (and kudos to Carta for making such a pretty picture):

Observations (other than the obvious one that this is mostly noise):

Fintech is still a favorite place for VC to put their money.

Real estate is doing surprisingly well, at least with valuations and the number of companies that have been funded.

Web3 ~40% over the median valuation? Ok alright.

Logistics is raising lots of money, but interestingly the increased supply of cash has not put valuations higher.

Adtech and Edtech don’t fare as well. In the former case, there are just lots of Adtech companies (and the FTC has made their lives miserable). In the latter case, there aren’t many successful Edtech exits (and there is no shortage of well-intentioned founders who want to make education better).

“Early stage” is a slightly broader category than pre-seed, but the picture from AngelList isn’t that different:

Healthtech jumps out as the biggest difference between the two datasets. AngelList says the category did a lot of deals and raised a comparable amount of money, whereas Carta says it did a lot of deals, but traded relatively cheaply. Who knows.

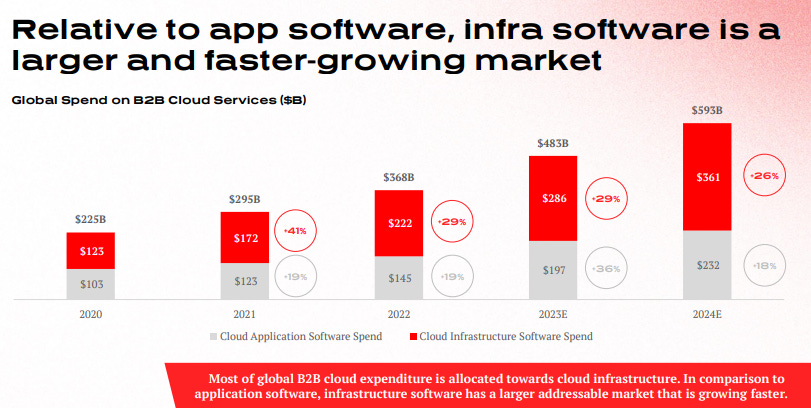

Because this is about technology companies and I’m making it a chart-o-palooza, I figured I’d also drop Redpoint’s new “Cloud Infrastructure Index.”

The index separates the “cloud” companies (storing, watching and orchestrating data) from application software companies (doing specific things), mostly because they are different, both in function, but also trajectory. And VCs like make indexes.

Anyways, the entire presentation is interesting, but this is what stood out to me:

The estimated market sizes for these companies has grown massively in a short period of time

As platform plays, they really do capture an outsized share of spend (which is how the theory would go):

Aside from the useful categorical refinement, it’s also some evidence that investors aren’t just yolo-ing to oblivion. Yes, the price for this growth is pretty outlandish (and expanding growth multiples sure are puzzling), but so is the growth itself. Even if things are ultimately bearish, you can still pick some winners.

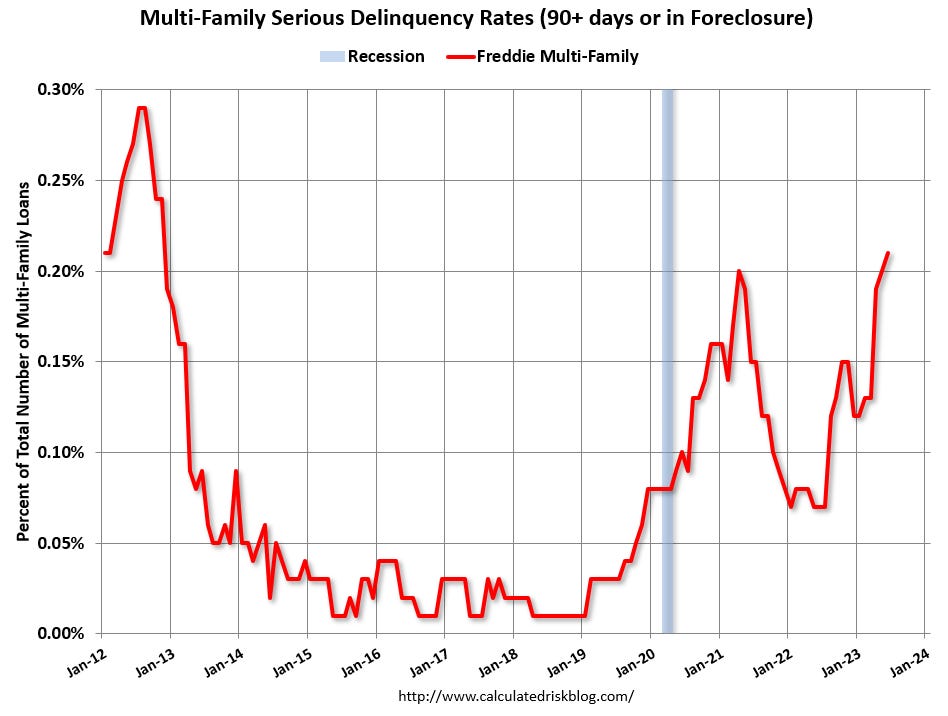

Equality before the rates

RW has variously made the point that evidence of a strong consumer, doesn’t mean that everything is fine, or that a drastic increase in the price of money won’t eventually take its toll. The effects of rate increases take time, particularly when consumers are somewhat insulated from the immediate effects.

To further illustrate the point, here are a few other examples of the ways in which the pain of higher rates do not hit everyone all at once.

Take landlords for example. Their borrowing costs have gone up substantially, and so delinquency rates are starting to rise (h/t CalculatedRisk by Bill McBride):

Single Family homeowners, however, have 30-year mortgages. They pay no nevermind to the rise in interest rates (unless they want to buy a new house), and therefore their delinquency rate is basically at all time lows:

All real estate is not the same.

Here’s another example: bigger companies still get to borrow cheaply, while it’s smaller companies that are paying a lot more (h/t Daily Chartbook) :