Extend-and-pretend

Daily Data: VC correction continues but they're not the only ones playing out the string

Daily Data: Extend-and-pretend in VC (and elsewhere)

VC correction continues. More down rounds and more bridge rounds

A theory of missing bankruptcies, aka the lawyer version of extend and pretend (and a reminder that credit markets hate surprises)

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. VC Correction Continues

Money continues to be scarce in the start up ecosystem.1

The correction has been happening—it’s one of the few expected consequences of higher rates that has actually materialized—and while there was some hope that recent bullishness would lead to some thaw, it hasn’t really shown up in the data.

Down-rounds are still much more prevalent than ever before:

20% of rounds are at lower valuations than the previous fundraise.

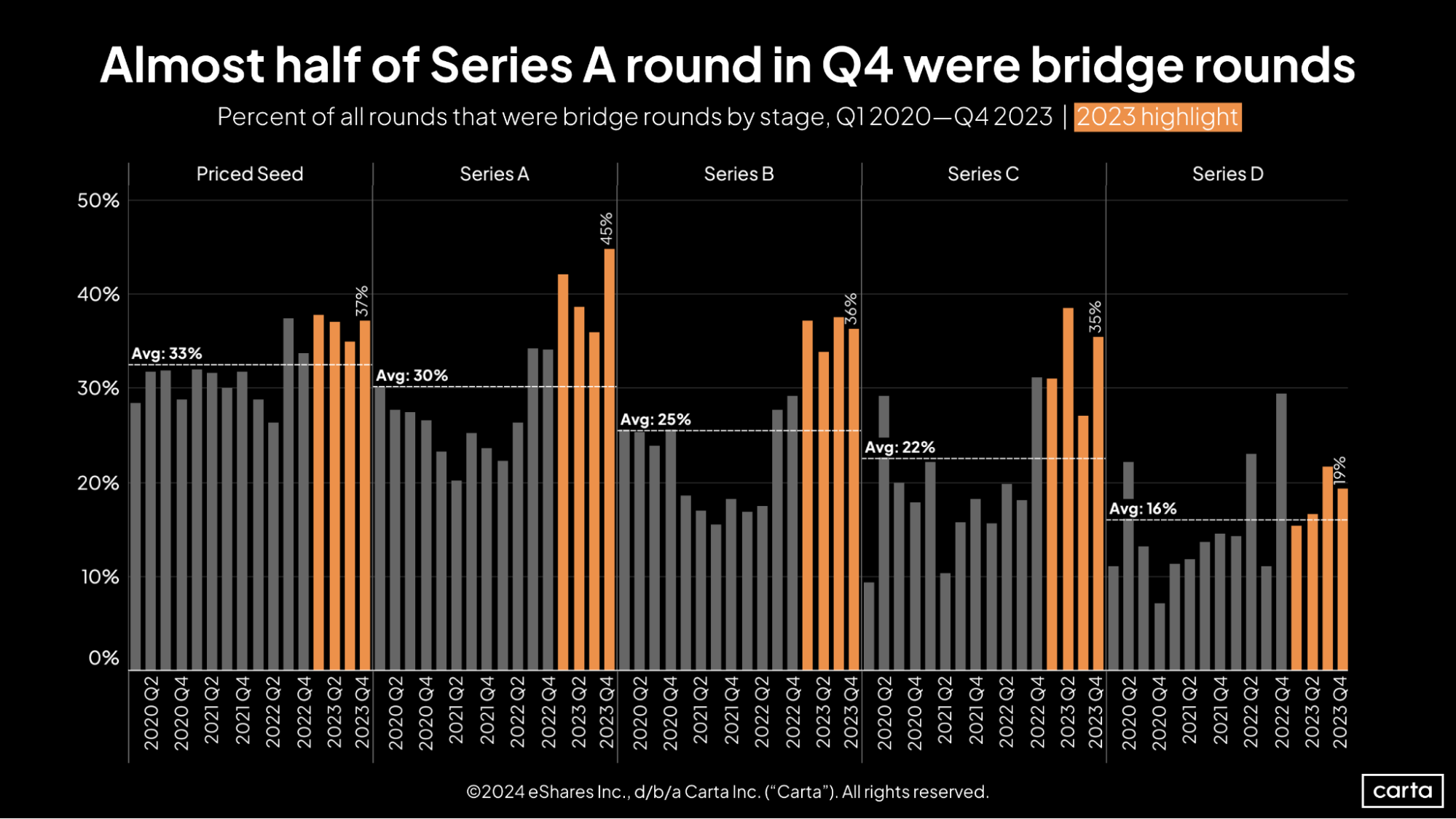

Bridge rounds also continue to be up across the board (except at Series D, a lone bright spot).

Nearly half of Series A rounds were bridge rounds.

So, to summarize, there are fewer rounds in general, and of those that are getting done, a higher percentage of them are getting marked down or stay flat. (It’s amazing that all this discounting doesn’t show up at the fund level…)

This is VC’s version of “extend and pretend.”

If you have the option of kicking the can down the road until the sun comes out again (i.e. ZIRP comes back), then you will. Pretty much everyone involved is heavily incentivized to act as though everything is fine for as long as they possibly can. There’s no “short side” of the trade hectoring for price discovery, and if things do turn around, then everyone will be rewarded for their patience and perseverance. (And if they don’t turn around, it’s unlikely anyone will get penalized more for doubling-down on their mistake.)

Bridge-rounds, down-rounds, lots of preference and structure, aquihires, etc. are all ways of keeping the music going, without the sh*t visibly hitting the fan (and that’s not a bad thing, per se).

Extend-and-pretend, Ch.11 edition, i.e. where’d the bankruptcies go?

Relatedly, lots of people have observed the relative paucity of bankruptcy filings.

Sure, they ticked up a bit, but not nearly as much as one might expect, given how tight funding has been: