Higher rates make companies lean, mean, profit generating machines (reprised, revisited)

Some more observations about the effective transmission of higher rates, and what it means going forward

I didn’t even realize the post didn’t send this morning. Enjoy some late-lunch reading!

when rates went high, firms definitely felt it—CapEx all but disappeared

despite the penny-pinching, cash positions continue to slide (among borrowers)

some pockets of ‘make you wonder what’s really going on underneath the hood’

cutting CapEx makes you stronger (depends a bit on how good at CapEx you might be)

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Higher rates make companies lean, mean, profit-generating machines (reprised, revisited)

Apropos of higher rates making companies lean and strong, I found a few more charts that illustrate what (some) companies do to adapt.

It’s not all smooth-sailing—and indeed, some of it looks like can-kicking or water-treading—but I found it interesting nonetheless.

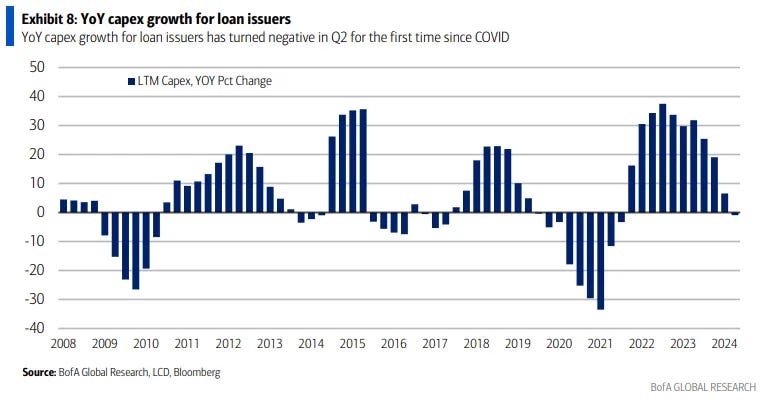

Hold the CapEx

One thing that borrowers have done (in the aggregate) is that they’ve cutback on investing in their businesses:

CapEx for borrowers has been steadily declining and finally went negative in Q2 2024.

The trend is even more extreme when you focus on high yield (i.e. riskier) borrowers specifically:

HY borrowers cut CapEx precipitously.

And these are likely “growth” companies, so CapEx is a big part of their raison d’etre.

That borrowers would conserve their cash and avoid big investments is understandable. It’s also exactly what the Fed had in mind.1

Leaner, but not necessarily stronger

And to be fair, cutting CapEx doesn’t necessarily mean we’re gonna skate clear of this thing (or that companies are better off for it, as per below).

Random Walk already pointed out that bankruptcies have been coming due, slow but steady (and now at 15-year highs).

And despite all that penny-pinching, many borrowers are still burning cash.

Cash reserves for borrowers have been getting lower and lower:

Cash on the balancesheet as a share of short-term debt has decreased rapidly from the ‘21-’22 peak.

Whether cash positions continue to deteriorate, is an open question.

Plus, you gotta figure that for all the low-interest debt that was issued in 2021, at least some of it is coming due, at prices that the borrower can no longer afford:

2021 set-off a bonanza of low-interest borrowing, but borrowing has been much lighter since then.

Borrowing picked up again in 2024, the majority of those were refis (given the brief decline in rates), which again, may reset in a higher rate environment.

Anyways, the point, for now, is that higher rates most definitely “transmitted” some pain and discipline to the street—pennies were, in fact, pinched. (And a quibble with the suggestion that higher rates did not “transmit” is what started this whole thread.)

Some companies just borrowed less, and otherwise got leaner and meaner, others have conserved cash (with mixed success) in other ways.

Pockets of worry?

Random Walk has become generally more optimistic about this evolution, but if you want to know where the pockets of distress could be hiding, there are some pretty obvious guesses.