Insurance and Private Credit, two peas in a pod

Who needs deposits, when you've got annuities? Non-bank lenders have a brand new bag.

Insurance dollars and private credit, two peas in a pod

annuities are the new deposits

Private credit’s demand for insurance dollars is booming

Insurance dollars’ demand for private credit is also booming

chasing yield or just a new, better sheriff in town?

where ordinary people and the “shadowy” world of non-bank lending intersect

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Insurance dollars and private credit, two peas in a pod

An interesting thing that’s happened at the intersection of ordinary people and capital markets is the rise of annuities (and life insurance) as a source of capital for lending.

What I mean by that is that while the old bank-lending model (i.e. lending against deposits) is under pressure—because deposits are expensive and prone to flight—a new non-bank-lending model (lending against annuities) is rising to take its place.

More simply, private credit (i.e. non-bank lending) plays an increasingly important role as a source of credit, and it’s increasingly relying on consumer insurance products to fund its efforts.

It’s unclear that people are really aware.

Annuities > Deposits as a source of funding

But it all makes a good deal of sense, when you think about it.

As Apollo’s co-ceo, Marc Rowan, explained to Tyler Cowen:1

If you think about it at a very macro level — regulators, governments. There are really only two choices for credit. You can have credit come from the banking system, or you can have credit come from the investment marketplace.

. . . [T]he banking system borrows short and lends long. They are always mismatched. If you think about what we [non-bank lenders] do . . . half of our money comes from the insurance industry, including our own affiliated insurer, Athene, and money we manage for Athora, our European affiliate, as well as a number of third-party insurers. Insurers, unlike the banking system — they borrow long and lend long, and everything, therefore, is asset matched. If you look at Apollo today, there is nothing that is daily redeemable.

Borrow-long-to-lend-long > borrow-short-to-lend-long.

If bank-lending is, in fact, passing the baton to non-bank lending, it’s certainly the moment that Rowan has been waiting for:

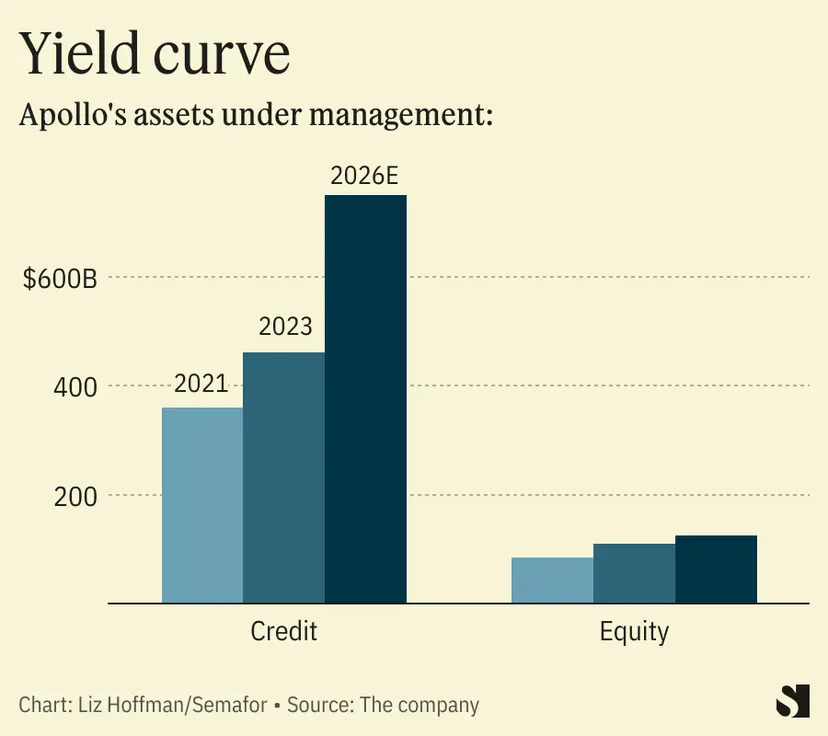

Apollo is growing its credit assets about twice as quickly as its equity.

So Rowan is talking his book, but the point he makes is a sound one.

When someone buys an annuity (or pays into a pension), they don’t expect to withdraw their money, as they would with a bank deposit. What they expect is steady and predictable yield, spaced out over time. For the asset manager, that means (a) no “bank run” risk; and (b) predictable return expectations (that can be modeled to leave room for upside).

Provided there is enough annuity demand to support large scale lending, it’s a win-win-win:

consumers/pensioners get a useful place to park their cash,

lenders get a very sticky source of capital with predictable return targets, and

borrowers get loans from sophisticated and reliable lenders.

Whether consumers know that they’re funding the burgeoning business of non-bank lending is a separate question, but hopefully they have done some homework.

As private credit grows, so too does demand for insurance dollars

Anyways, it’s also the nature of supply-and-demand to be mutually reinforcing.

As private credit grows, it creates demand for sources of funding, which gives annuity-sellers extra pep-in-their-step, which drives annuity-sales upwards, which creates demand for yield, which helps private credit grow, and so on and so forth.

It’s actually been a pretty sharp kick in the pants for the formerly sleepy world of retirement planning.