Private capital is borrowing time (and investors are happy to lend)

Daily Data: Lend, but don't buy, is working out fine so far

🚨🚨Before the main event, just a quick plug: please upgrade to a paid subscription.

Random Walk cannot maintain a daily cadence for that much longer, without a big lift in paid subs.

So, if you like Random Walk, and aren’t a paid subscriber, it would cost less than dinner and drinks, to show your support. 🚨🚨

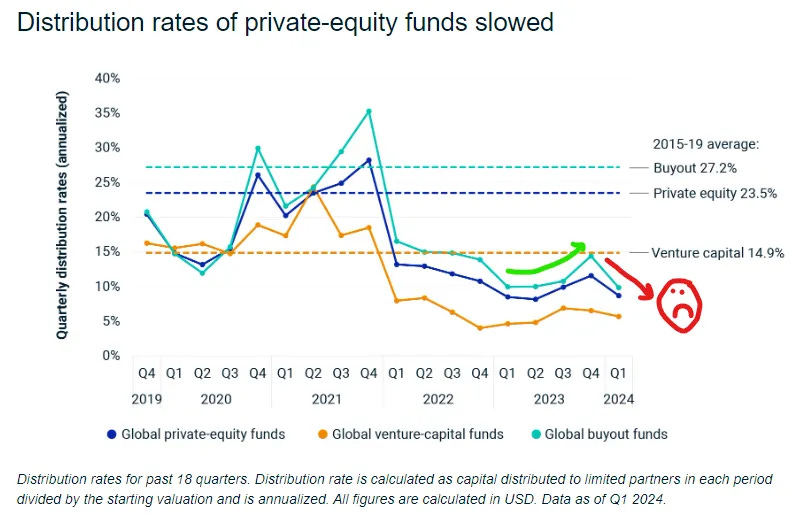

PE/VC distributions to LPs still not the best

Wandering the J-Curve with Persephone

Investors won’t buy, but they will lend

Less reward, more risk, no problem. Really, leveraged loan defaults are . . . down.

While PE/VC borrows money to buy time, there is some creaking, but definitely no breaking

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Private capital is borrowing time (and investors are happy to lend)

The story in private capital markets has been incredible calm, in the face of pretty terrifying underlying conditions.

Higher rates have repriced everything that PE/VC folks invest in, but in the wrong direction.

Without any buyers (or subsequent investors) willing to pay more than what the current investors paid, the assets remain unsold, and if assets remain unsold then no money gets returned to LPs, and if no money gets returned to LPs, then its hard for PE/VCs to raise new capital, and if its hard to raise new capital, then PE/VCs aren’t going to deploy much capital, either.

So, everything just kind of sits on ice, while (in theory), things get gradually worse.

LPs do, eventually want some money back (and the PE/VCs would like to make some money too), and their portfolio companies are (by design) generally not profitable companies—so if they can’t go on forever, without fresh sources of capital.

It’s got all the makings of a cataclysm . . . but it hasn’t really happened.

I mean, all the ‘makings’ have happened: new funds, new deals, acquisitions, distributions, etc. are all very much in the pits—a16z accounted for ~80% of the venture dollars raised from LPs this year—but the cataclysm hasn’t happened.

Not even remotely.

(Still) no exits in private capital

Despite some nice headlines, and a few prize assets getting sold, there are still No Exits in Private Capital:

Distributions, which were already well-below their pre-pandemic ranges, took a turn for the worse, in Q1.

Unsurprisingly, the “cup” of the j-curve—which reflects the part of the fund’s lifecycle where money goes out, before it comes back in—is deeper and wider for the late-teen vintages (that are supposed to be selling off now):

2018-2019 vintages are wandering off in the depths of private capital Hades.

Staying negative for longer is not where anyone wants to be.

And yet, despite it all, everyone seems pretty cheerful, and certainly quite calm.

To be sure, there has been some visible pain: startup closures and consolidations are creeping up, and some big leveraged buyouts have run into trouble, but for the most part, not all that much pain.

Through a mix of secondary sales, continuation funds, bridge rounds, and loans (aka “extend and pretend”), private capital has just kept skimming along, buying time until the capital markets open up again (so they hope).

It may not be pretty, but it’s worked.

Lend, but don’t buy

PE/VC have been able to buy time, because there is still no shortage of cash sloshing about.

The cash just mostly wants to lend to risky companies, rather than buy risky companies, but for now, that works.

For example, leveraged loans have seen historically high inflows (even if June was a relatively slow month, and spreads finally widened, so y’know, famous last words).

In fact, investor interest has been so high, that ~30% of the market is just repricing older, more expensive debt at cheaper prices: