Private Credit and Insurance, two peas in a pod (reprise), and a chart dump on default rates

Mutually reinforcing gains, and still no sign of pains

five charts on the rise of private credit in life insurance

private credit begets higher yields which beget more competitive retirement products which begets market share which begets private credit . . .

7 charts on default rates: bankruptcies jump, LME defaults, private credit defaults, covenant defaults, and BAD PIKs

Is there trouble on the small side?

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Private Credit and Insurance, two peas in a pod (reprise), and a chart dump on default rates

Data on the rising role of private credit in the life insurance industry (and what drives it), plus seven charts on default rates of various shapes and sizes.

Private Credit is swallowing life insurance, and everyone wins (for now)

Random Walk has written previously about the natural marriage between life insurance (and other annuity/retirement products), and private credit.

The short version is that retirement premiums are a better capital base for lending than bank deposits, because insurance premiums do not have a the duration mismatch that deposits have. Plus, the “silver tsunami” is a secular driver of both (a) premium flows (which non-bank lenders are eager to accept) and (b) demand for retirement yields (which non-bank lenders are eager to provide).

The net result is that private equity (i.e. that universe of non-bank financial firms that include the largest direct lenders in the biz, like Apollo, KKR, and Ares, etc.) have been increasingly swallowing the world of retirement products. PE buys insurance companies to sell higher yielding retirements, the premiums of which are invested into the higher yielding loans originated by their lending platforms.

Is this bad?

Honestly, probably not, but of course there’s some risk at the margins. Life-insurance premiums are, in fact, a better capital base for lending, and private lenders are awfully good at delivering higher yields—especially by going where trad lenders won’t go.

But, of course, it means the nation’s retirement plans are increasingly at the mercy of the sophisticated financial engineering of a small and interwoven set of firms, with relatively less transparency.

Opacity, complexity, and contagion risk, all in one!

But, in the meantime, private credit remains one of the hottest asset classes for good reason.

Chasing premiums to fund loans to generate yields to chase premiums . . .

Anyways, behold some recent research from the Chicago Fed providing more color on the shift.

More private placements

Life insurers have doubled their exposure to private placements in less than 10 years:

Life insurer private placement holdings have gone from ~$400B to ~$850B since 2015.

So, insurers are indeed tapping private markets more and more.

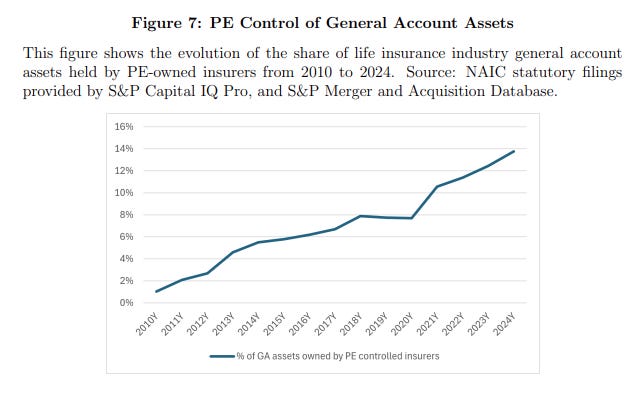

. . . driven by more PE-owned life-insurance

The allocation to private placements has been driven by a shift to PE-backed insurers:

The share of life insurance assets owned by PE-backed insurers has also more than doubled, going from ~6% to ~14%.

It’s PE-backed insurers that hoovering up an increasing share of the investing.

. . . driving flows to ABS

It’s PE-ownership specifically that’s driving flows into private placements, specifically the more complex, higher-yielding kinds.

PE-backed ownership of Life Insurance Cos drives increased allocations to private placements, and more complex structures, like Asset Backed Securities, specifically: