Rate cuts help equities, how exactly?

Daily Data: Periodic reminder that Uncle Sam is borrowing more and more and is giving no indication of stopping

In today’s dispatch:

Rate cuts are supposed to help equities, by convincing investors to stop lending to Uncle Sam, and buy stocks instead

Price discrimination matters, monetary policy edition

If rates go down, won’t they go up anyway?

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Will a rate cut help equities?

All major stock indexes are booming, presumably because inflation data was nice and cooling, which means that rate cuts are around the corner, which means boom times for riskier assets, like equity.

Or maybe that’s not why. There are other reasons, as well. But in all events, indexes are booming, and at some point, cuts will come, and people seem to think that’s good for stocks.

Random Walk might have some observations about the inflation data another time, but for now, suffice it to say that (a) inflation is going pretty much as expected (by RW at least), and (b) it’s never not amusing how much month-to-month trend wiggles seem to matter, when they obviously shouldn’t.

Inflation is not the thing I care about today.

The observation in focus for today is the assumption that lower rates will drive liquidity (and therefore gains) to equities. It doesn’t seem right, or it seems very under-considered.

The reason people think that lower rates will be good for equities is pretty straightforward. Lower rates make safer assets, e.g. treasuries, less attractive, so investors have to put their money in riskier assets to generate equivalent yields. In other words, when rates go down, money will shift from Uncle Sam to the stock market.

Uncle Sam’s pain, is Finance Bro’s gain.

Random Walk has mused about this before, but since it’s back en vogue, it bears repeating: how exactly is Uncle Sam going to withstand pain?

And if it won’t, then how exactly do Finance Bros gain?

Uncle Sam needs to borrow, and high rates keep lenders happy

Uncle Sam is going to need to borrow money, whether the stock market likes it or not.

The deficit is growing, and Treasury’s borrowing grows with it:

No one that I’m aware of is forecasting a reversal of Uncle Sam’s borrowing needs. All signs point to “more.”

How does Uncle Sam borrow all that money?

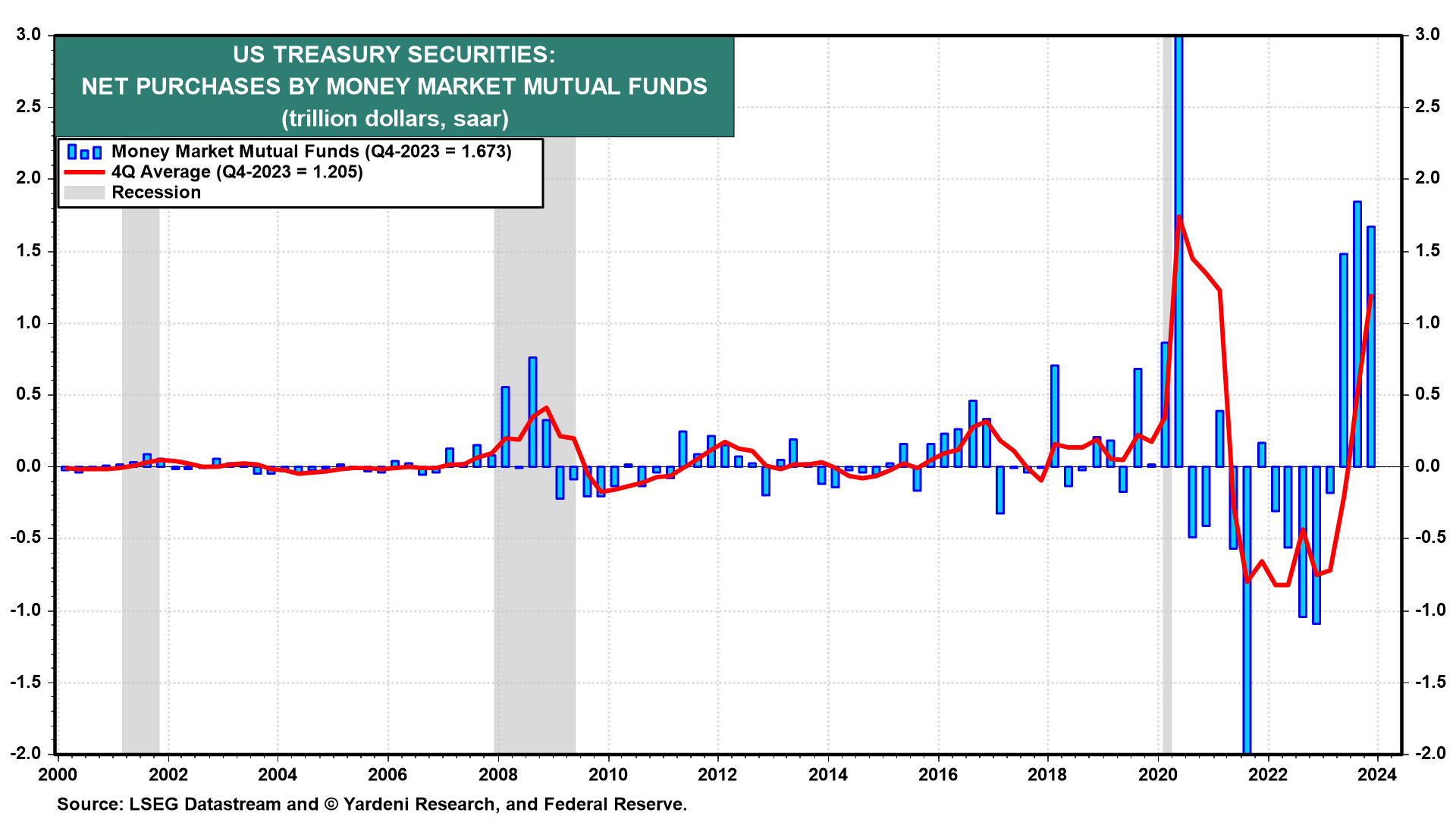

Recently, Uncle Sam has found willing lenders in the form of “US Households,” i.e. investors, or people who care about yield.

Money market funds snapping up high yielding T-Bills is keeping Uncle Sam in business.

High rates might be bad for the Finance Bros, but they’ve made it a lot easier for Uncle Sam to satisfy its borrowing needs.

Yield-sensitive buyers are the only game in town

That these are yield-sensitive lenders is an important distinction.

In the old days, the big buyers of US debt were central banks and sovereign nations. They weren’t buying treasuries for the yield. They bought them as a safe and useful alternative to cash.

But those days are gone.