The latest bank data from the FDIC

Daily Data: So how are the banks doing?

The latest banking data is in. How are the Fed’s favorite whipping children holding up?

Everything reads better in your browser or in the app. The footnotes especially, and Random Walk is really leaning into the footnotes. Plus, if you have the app, you can set delivery to “app only” and then my daily barrage will feel less like a barrage. Unfortunately, substack does not yet have a “Weekly Digest” option, but I’m hectoring them aplenty.

If this email was forwarded to you, please click the shiny blue button:Daily Data

Banks are hanging in there

The FDIC released updated data on the health and performance of FDIC-insured institutions.

Banks have born the substantial brunt of the Fed’s interest rate rug-pull, but they’ve been hanging in there, for the most part. The data is lagged, so if a specific bank had run into acute trouble, we’d probably already know that by now, but it’s interesting nonetheless.1

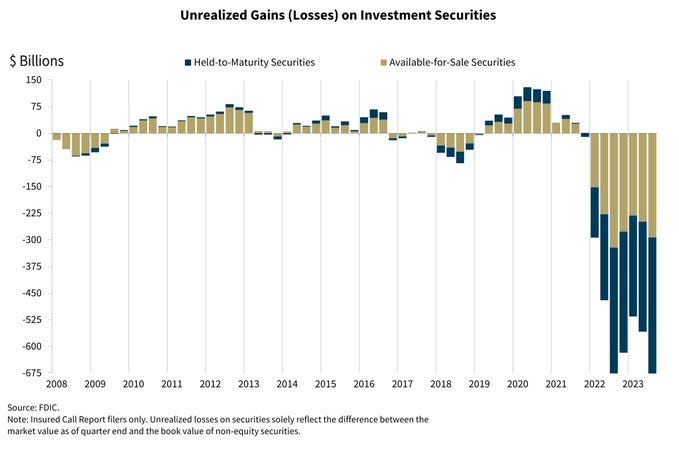

Unrealized losses

The first chart that jumps out are unrealized losses on securities.2

This is the meat of the rug pull, where a sudden increase in rates devalued all the loans that were issued at ZIRP prices—huge losses on low-interest loans is part of what brought SVB to its maker, for example.

After a positive reprieve for the first part of 2023, unrealized losses are going in the wrong direction:

Unrealized losses are now just ~$5B off of their 2022 peak.3

I suppose this was to be expected, given the steady rise in yields, and presumably it will look a little better next quarter, if the 10-year continues to de-froth a bit. The FDIC seems remarkably calm about it, so maybe that’s all there is to it.

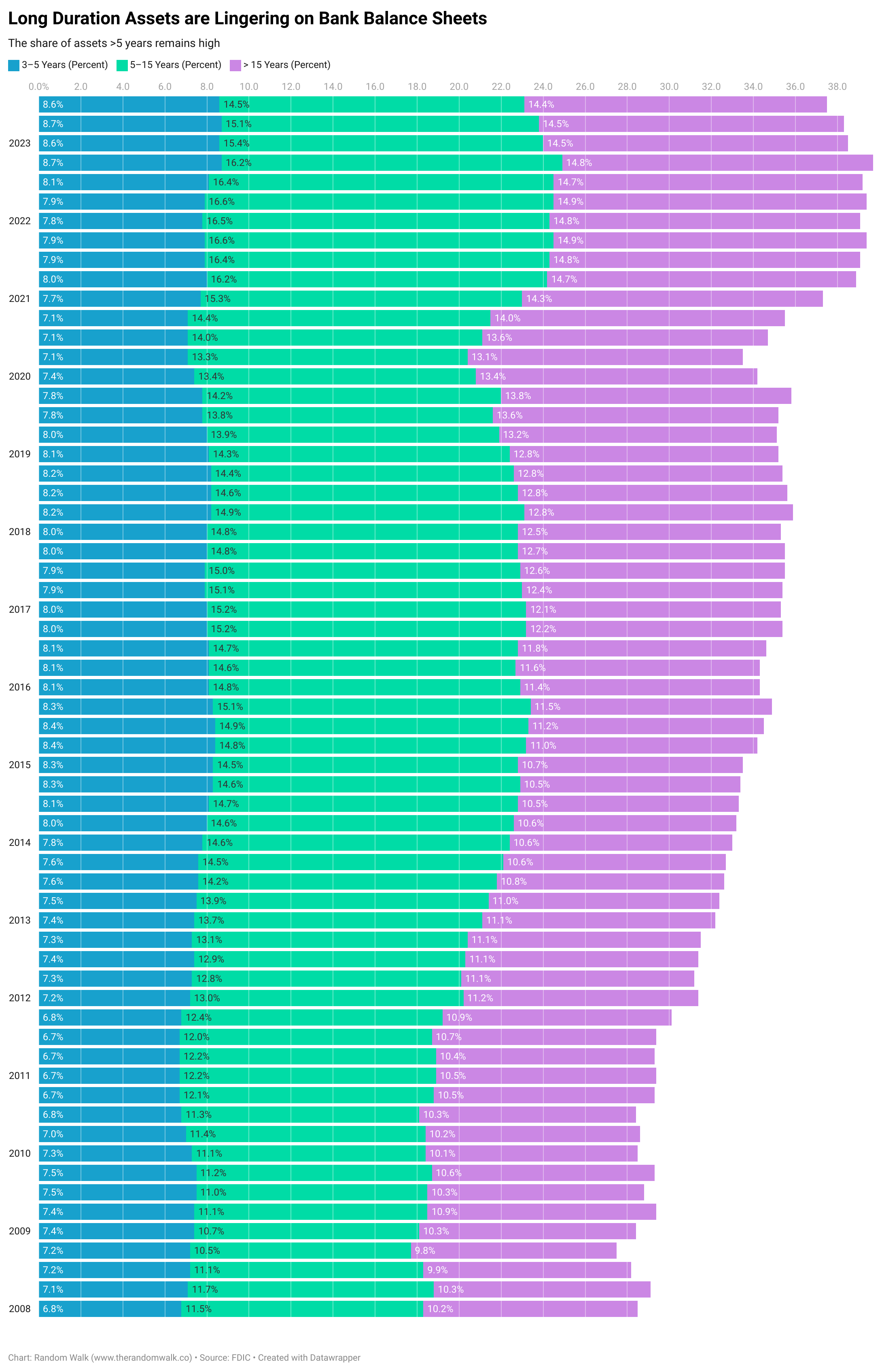

Duration continues to be a problem, to these eyes, so it’s not like those long-dated, low-yield assets are just going away:

The 15+ year stuff is holding pretty steady, but the 5-15 year assets are at least trending downwards.

Go long, or go home.

As long as there’s no sudden demand for liquidity, then what’s a little unrealized loss among friends?

Deposit flight

The other aspect of the rug pull is that high rates evaporated a cheap source of funding for banks, i.e. low/no-interest deposits.

If banks are holding lots of assets yielding ~2%, they can’t exactly pay depositors ~4% to keep their money (and if everyone pulls their deposits, those unrealized losses become realized very quickly). So, deposits fled from banks to money market funds, and the like.

That was then, but what about now?