Thread's dead, baby, thread's dead

6 datas to learn new things: WFH is good; Start-downs, Students of Peloton; BYD; the Ozarks, Thread's Dead. 1 reminder that high prices still don't mean everything is fine.

Welcome back, my best beloveds, and welcome anew to the newest best beloveds. It’s Tuesday, which means, it’s a Scatterplots and Great Wall of Text Day.

The six sacred scatterplots:

WFH is good (reprise)

Start-me-up, start-me-down!

Students of Peloton

Bretty-Young-Dhing (BYD!)

Something about the Ozarks

Thread’s dead, baby, thread’s dead

The one mundane Great Wall of Text:

Everything is still the same or why everything bearish is still coming to pass (more or less)

As a reminder, if you like Random Walk, please do tell your friends. Like, share, both, whatever. Most of all subscribe, ideally with a paid subscription, because you know, I need that too.

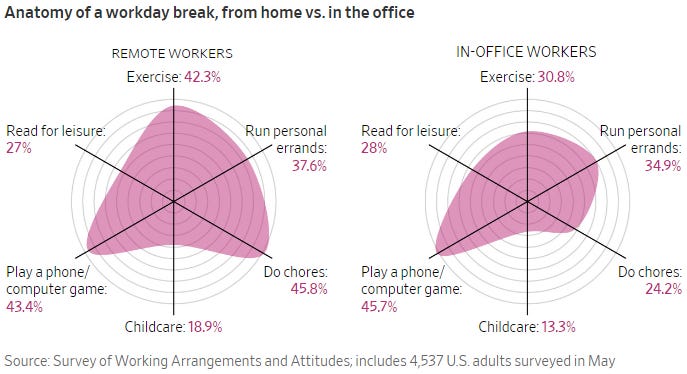

WFH is good (reprise)

Office occupancy went back to half-full (as expected).

Unimaginative managers are pushing back-to-the-office, while inspired employees fight for flexibility. Leverage will continue to favor workers for now, but the tides are slowing turning against the forces of good, in favor of the forces of evil.

RW continues to think that WFH is good, and the quality of life tradeoffs are worth it (even if hard to measure). Every-day, all-day isn’t necessary, never was, and never will be. Harumph!

Plus, look, when you’re working from home, you exercise way more and you don’t play stupid games on your phone:

What more proof do you need?!

Start-me-up, start-me-downs

The number of startups that are shutting down appears to be rising (and has been since Q1 2022):

Taking the data at face value (and I see no reason not to), this isn’t surprising or bad (even if it’s unfortunate for the people involved). There’s been a slowdown in venture funding, and since most venture businesses are not self-sustaining in the early going (because otherwise why would they need venture capital?), then you’d expect shutdowns to increase. It’s a healthy correction.

What’s interesting is that venture funding recently seems to have followed some of the optimism in the public markets, i.e. it’s picked up a little of late. Given the very long time-horizon for early stage venture that puts years between investment and returns-on-investment, there is no reason that the QoQ performance of the stock market should matter. It’s like checking the traffic for a trip you’re planning 7 years from now.

And yet, the spirit compels us.

Speaking of time-horizons, love this chart from Pitchbook that records the 1-year IRR for 8 different asset classes (with the 15-year IRR at the righthand side):

What jumps out (other than time preferences matter):

venture and growth have had good runs;

2021 everyone was really good at investing . . . 15.2% IRR was the worst you could do;

2022 was a throwback year, where real stuff (commodities, infrastructure) and old school finance (private credit) carried the day, while “casino investing” took a back seat;

oil and gas takes some serious mettle, with very little middle ground;

private capital, on the other hand, lives in the middle ground . . . maybe why it’s often called a “hedge” fund;

Anyways. I don’t have anything profound to offer. I just thought it was a fun chart.

Students of Peloton

It’s unsurprising, but good to see, that wealthier student borrowers tend to have the larger monthly student debt payments:

Most of the payments bunch around $200/month (or less), i.e. the red and green bars. That’s not-nothing, but it’s not a gamebreaker either. $1,000/month (the light purple bar) is most definitely a gamebreaker for some people, but it’s a relatively small part of the picture and is most prominent among the wealthiest group, who ought to be able to bear it.1

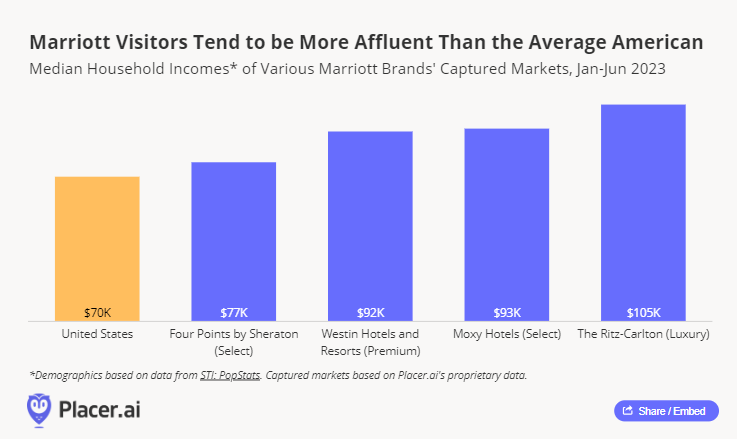

It’s a bit cute, but Earnest took a stab at estimating which retailers would be most harmed by the resumption of student loans. If you’re in the top left, you’re in the “most trouble” because (a) more than 10% of your spend comes from borrowers (above the line), and (b) borrowers increased their spending more so than non-borrowers (to the left).

In other words, if you’re in the top left, you have many student borrowers among your customers, and when repayment was suspended, they increased their buying more than the rest of your customers.

Peloton jumps out, as does Frontier Airlines, which is almost a mirror image of Delta, JetBlue and United. Spirit Airlines is plain weird insofar as it’s definitely preferred by student borrowers, but non-borrowers increased their spending on Spirit much more so. AirBnb also—very popular among borrowers, but it was non-borrowers who increased their spending more. Marriot Hotels simply pays no nevermind to the student borrower cohort whatsoever.

‘It’s easier to find something to sell, then find people to sell it to’ or so the saying goes. Customer segmentation works in mysterious ways.

Bretty Young Dhing

I’m still wildly impressed by BYD’s—the Chinese EV maker—incredible growth. It took about three years to become the world’s #1 exporter of cars:

It also took a lot, a lot of Chinese subsidies to get there, but still, wow.

I don’t purport to know what China is actually doing, but it sure looks like they’re preparing for a less finance-driven asset-based world, and moving hard to real stuff like minerals n’ things, especially the kind we use to make “green” things.

Something about the Ozarks

FactSet published a little piece with the enticing title “Deposit Data Debunks Conventional Wisdom.” I like debunkings. I’m interested in deposits. I will click.

Bank runs at SVB, Signature, and First Republic gave rise to a new tenet of conventional wisdom: deposits share is shifting from community and regional banks to the too-big-to-fail cohort, dimming the prospects of smaller banks and nudging them to sell. It’s an elegant, intuitively appealing theory.

It’s like they’re talking directly to me. I am one of those fans of the “elegant intuitive theory.” Go on, Mr. Factset, go on.

The one, tiny objection we feel compelled to offer is that, based on the data, it isn’t actually true.

Wait, what?! OK, now you really have my attention.

So is the elegant theory wrong? Are deposits not in fact running?

Well, no, as much as I like being wrong, most of what Factset showed was that deposit flight was basically ongoing, but instead it wasn’t limited to just regional banks, but big banks too were feeling it a bit. I admire the hustle, in all events.

Anyways, my disappointment in not-being-wrong notwithstanding, what was interesting is that one regional bank is in fact doing something very different. Bank OZK, fka Bank of the Ozarks, is in fact growing deposits, including non-interest bearing deposits (i.e. the kind that don’t require paying savers 5%) by an industry leading 2.6%.

Ignore factset’s highlighting (meant to show that big banks are also losing deposits to prove deposit flight isn’t real(?)) and focus just at the top:

Why that is, I don’t really know, but I’m very interested to find out. Funnily enough, the coverage I was able to find is from 2018. It’s a post by noted market monetarist Scott Sumner calling attention to Bank OZK for—get this—its outlandish exposure to real estate projects and the attendant risk of rising interest rates. Predictions are hard, even when you’re as right as you can be. 2

Anyways, I genuinely don’t know what’s going on, but it sure is curious. Maybe they’re the only RE lender in town? Maybe they’re just really skilled managers conquering new lands, just like they did back in 2018 when they ran laps around more established RE lenders? Maybe they just didn’t restate their deposits downwards, like some other banks? Maybe they got a few chunky deposits and it’s messing with the data? Idk.

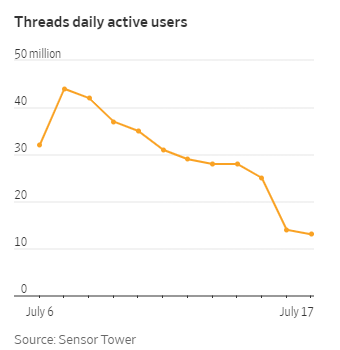

Thread’s dead, baby, thread’s dead

Personally, I wouldn’t have killed the bird and replaced it with an X. I also think there are lots of reasons an “everything app” will fail, even if it succeeds in China. But that’s just my opinion and frankly it doesn’t matter much. “Tech CEO does something hubristic and risky!” can you imagine?! What’s the world coming to? Smdh.

You know who’s opinion really doesn’t matter much? All the people who have declared TWITTER IS DYING!! OMG ELON SO STUPID!! and have been wrong every single time, who are once again making the same fevered declaration.

Is Threads really dead?3 Who knows, but it’s certainly not going great:

That was similarweb, but Sensor Tower tells the same story:

It was only two weeks ago when Threads definitely killed Twitter, which is the 19th time twitter was definitely killed in the last year, so you’d think the X prognosticators would take a cold shower or something, but no. It’s getting hard to keep track of all the ways they’ve been wrong . . . twitter didn’t need 75% of its staff, it didn’t need legacy blue checks, and it definitely didn’t need its “content moderation” team. (Is it too soon to tell whether those claims might be true? I don’t think so, but I suppose maybe.)

The bigger lesson is that mood affinity bias is powerful and you should ignore these people on any subject about which they have an emotional investment.4 Why people get emotional about Elon, one can only speculate, but it really is impressive to watch smart people lose their minds repeatedly without contrition over-and-over again, time after time, repeatedly, the same thing on repeat.

Great Wall of Text

Everything is still the same

There’s a lot of “will it won’t it” recessionary talk around, including some mea culpae from prominent bears. The story is roughly “the us consumer is more insulated from interest rates than we expected.”

Personally, I continue to think that nothing has changed. That doesn’t mean bears like me are right, but it certainly doesn’t mean we’re wrong.