Mind the lag

Mean regression in VC; Rates cause effects that lag; Wages not growing; India likes gadgets; Anxiety for sale; and finally, Money is moving.

Did you know which fast-fooder opened the second-most stores in the country? Here’s a hint: it’s a goods baker. Yeah, I didn’t know that either. I suspect it doesn’t matter much.

On to the show!

Scatterplots: the datas that delight!

Mean regression in venture

Mind the lag (between interest rate causes and interest rate effects)

Wages not growing and other good things

India likes gadgets, and some other less good things

Anxiety for sale

Great Wall of Text: the words, with pictures, that . . . um, also delight?

Money is going South and other observations from the movement of people and things

If you like RW, I have a simple request: please share it with some people who are smart, curious, like data, and are bored of the usual mix. Just push the button, it’s easy:

I love you all!

Random Walk is an idea company dedicated to the discovery of idea alpha. Find differentiated data, perspectives and people, and keep your information mix lively. A foolish consistency is the hobgoblin of small minds. Fight the Great Idea Stagnation. Join Random Walk.

Scatterplots

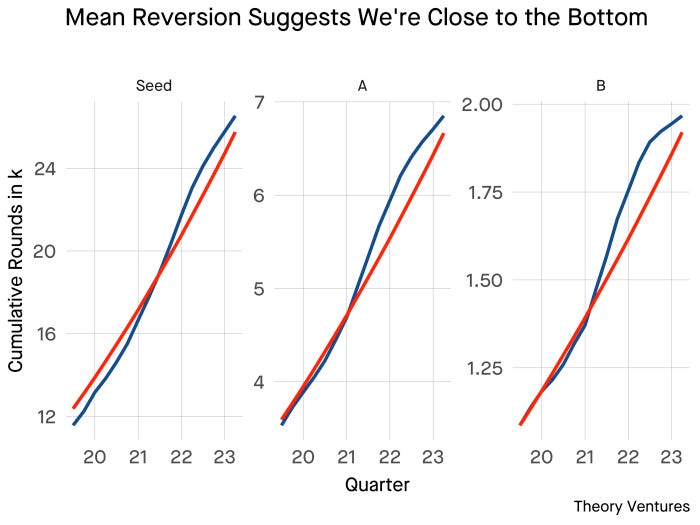

Tunguz on mean regression in venture

Theory Ventures’, and friend of Random Walk, Tomasz Tunguz sees startup investing returning to normal by the second half of the year:

Surge, followed by a dip, followed by a return to normal:

Means are regressing everywhere, so there’s certainly some truth to what Mr. Tunguz is saying.

Personally, I’m not sure that indexing to the ZIRP (zero interest rate period) is the way to go here—because (again) the big thing that’s not reverting to the mean are interest rates—but I will be happy to be wrong.

Mind the lag

There are many reasons why a drastic rise in interest rates can take their time to wreak havoc destroy demand. Here’s another one: it turns out that public companies at least borrowed for the long-term and won’t have to refinance for a while:

I’m not sure whether these are fixed or floating rate bonds, but unlike Real Estate, the “Wall of Maturities” is apparently not due for some time, so as long as they don’t need more credit, they can hang in there (even as defaults and distress creep steadily up).

Visual Capitalist is good at what they do, what can I say?

Now, it bears mentioning that someone else is on the other side of this trade—if companies are benefiting from below-market costs of capital, then their lenders are suffering from having lent capital at below-market rates (and no, the lenders aren’t out of the woods, yet).

Similarly, here’s another thing that attenuates cause from effect.

As a reminder, the majority of additional consumption during pandemania was driven by the lower 80%:

These aren’t the people most immediately impacted by the sort of demand that higher interest rates destroy (and indeed, they’re still buoyed by wage gains, as per below). Lower income brackets drove the recent consumption binge, and higher rates don’t mean a thing (to them, yet, for the most part).

It’s the titans of leverage (i.e. folks at the high end) who benefited the most from free money over the longer haul, and therefore they will feel the most (relative) pain. Their spending habits, however, can take some time to adjust—and weren’t driving the most recent surge, in any event.

More simply, the most proximate effects of higher rates do not impact the most proximate causes of the recent boomtimes.

Real estate and cars (and other financed stuff)? Sure. The finance industry itself, i.e. banking? Also sure.

But the overwhelming majority of consumers and (apparently) companies? They’re a step or two removed from interest rates. They got a lot of stimmy money, but interest rates aren’t going to unring that bell.

Wages not growing and it’s good

As per before, if wages grow at 5%, the likelihood that inflation grows at 2% is low. Goldman Sachs sees wage growth as slowing, albeit stubbornly plateauing between 4-5%:

The Atlanta Fed sees a fairly precipitous decline in wage growth for job-switchers (and a more modest one for stayers):

Of all the prices, people prices are an important one to watch.

There’s still some extra money floating around out there, but not all that much more, at which point it will be higher wages (or not) that will drive MOAR CoNsUMptIoN (excluding the bottomless pit of the Federal Government’s consumption, of course).

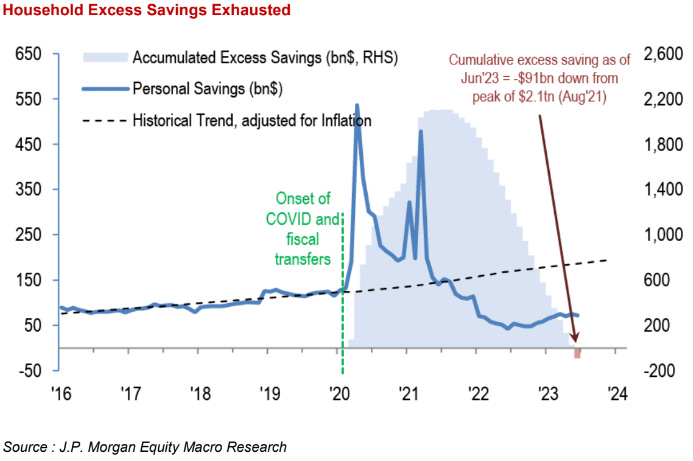

“Excess savings” (as calculated by JPM) are now gone (via Daily Chartbook):

“Excess liquidity” (as calculated by JPM) has another few months left to go:

Once the pandemania money is spent and gone, the consumers will have to stand on their own. We shall see.

India likes gadgets

Continuing with the almighty consumer!

Similarweb did a big state of e-commerce report a little while back.1 RW will have more on that in the next edition, but just two little tidbits that would otherwise be non-sequiturs in the next edition, and even RW has standards about non-sequiturs.2