3 observations about small banks, fintechs and BNPL

Daily Data: Where consumer credit lurks in the darkness

This one is a doozy for a Daily Data. It’s really a triple data. But it’s good. Probably.

Everything reads better in your browser or in the app. The footnotes especially, and Random Walk is really leaning into the footnotes. Plus, if you have the app, you can set delivery to “app only” and then my daily barrage will feel less like a barrage. Alternatively, sign up for Weekly Recap only.

If this email was forwarded to you, please click the shiny blue button:Daily Data

3 observations about small banks, fintechs, and BNPL

Random Walk is going to make three separate, but related observations relating to smaller banks and their fintech partners.

the most downloaded consumer app;

a small transaction between BNPL frenemies; and

a local New York Bank that did an oopsie.

The observations seem unrelated, but they’re not.

At least, not in the twisted rabbit hole that is the Random Walkian mind.

You see, if you were wondering whether financial stress was out there, but possibly hiding, BNPL, fintechs and smaller banks (whether fintech-y or not) would be a reasonable place to look.

And, in case you didn’t notice, all three observations involve some crossover of BNPL, fintechs, and small banks.

Why would those be places to look? Well, two reasons.

First, if any bit of financial engineering could orchestrate a consumer ‘dead cat bounce’—a last hurrah of orgiastic holiday spending before the gloom—without anyone knowing about it (right away), it would be BNPL.

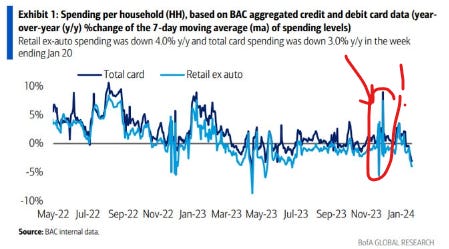

I mean, look at this . . . steady, down, steady, down, and then holidays come around and BLAM! PARTY’S ON!

And then January is back to a whimper.

In terms of why that might be, well it could be that incomes got stronger towards the end of the year, and people had a bit more pep in their step come holiday season. The reason that January spending moderated was because it was quite cold.

That’s actually a very plausible theory, and it means that everything is fine.

Another possibility, and back to the story at-hand, is that strained consumers yolo’ed one last holiday spending hurrah, using a specialty financing product, like BNPL and/or other consumer fintech loans.1

There are certainly anecdotes to support the theory, but that’s all they are, anecdotes.

The latest BNPL-inspired bouncing cat carcass? It’s called “Doom Spending” and all the kids are doing it:

Oh jeez.

Anyways, why is BNPL so ripe for this set up? It’s not because they are bad people, but because:

(a) unlike ordinary transactions, which show up in most commercial transaction panels with very little latency, and high precision, BNPL is a bit of a blindspot, i.e. no one really knows who’s using BNPL, how creditworthy they are, and how the loans are performing; and

(b) if you’re a fintech with a little ZIRP in your blood, you might be pretty motivated to grow topline, by convincing yourself that everything was fine and hope was right around the corner. Indeed, “dig the hole deeper” is a surprisingly common stress reaction.

So, motive to be a little reckless, and opportunity to keep it from showing (and mostly an opportunity for the rest of us to speculate freely).2

BNPL can’t hide consumer credit secrets forever. Eventually, the performance of those loans will show up in the earnings of some small bank that partners with the fintech. But until then, there is plenty to watch and wonder.

OK, that’s reason 1.

The second reason smaller banks (with or without fintech partners) are a potential source of hidden stress is that the BTFP is coming to an end in March.

Without the BTFP, all the small banks would have died.3

Is that still true? We shall see, but the point is really ‘here’s another reason why small banks are worth watching.’

To summarize, small banks and fintech/BNPL partners have got two signals they’re (potentially) hiding from the world:

(1) secret consumer stress, in the form of higher-than-expected defaults on consumer loans, like cars, or TVs or even clothes; and

(2) secret liquidity constraints, in the form of unrealized losses, no longer backstopped by the Fed’s emergency facility.

Unrealized losses? Oh yah, still got ‘em.

Whew. OK.

So much for the wind up, now on to the show.

Three observations about fintechs, BNPL, and small banks.