Actually, delinquent auto loans aren't consumer stress (maybe)

Another theory of rising auto loan delinquency that has nothing to do with consumer stress

Random Walk is at a conference this week, so notes will be shorter and lighter.An interesting thing about Ally’s delinquency trend

If it’s subprime or low FICO borrowers, it’s not showing up (yet) in the data

A collateral issue, not a credit issue (reprise)

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Actually delinquent auto loans aren’t consumer stress (maybe)

Last week, the auto lender, Ally Financial ALLY 0.00%↑ told the world that “defaults are trending worse than we expected.”

The question then is “whether things are, in fact, worse than we thought.” Rising defaults is obviously not a good thing, and could be indicative of consumer stress. Stress is, of course, different (and worse) than cautiousness, and while there is plenty of evidence of the latter, there isn’t that much evidence of the former. But perhaps Ally was telling the world otherwise.

Random Walk is still of the view that caution, rather than stress, presides.

Now, in furtherance of that view, it occurs to me that there’s reason to think Ally’s delinquencies have nothing to do with stress.

If not stress, then what?

It’s actually something that Random Walk speculated about a while back: credit quality hasn’t gotten worse, it’s just that auto prices are lower than anyone is letting on, and will continue to get lower.1 Ally’s problem is a collateral issue, not a credit issue.

If that’s the case, then the reason defaults are rising is the same reason that prime borrowers were struggling to get car loans: the collateral was overvalued. Car prices are coming down, and when people see that, they walk away from their over-priced loans.

Ally’s rising delinquency isn’t obviously a credit issue

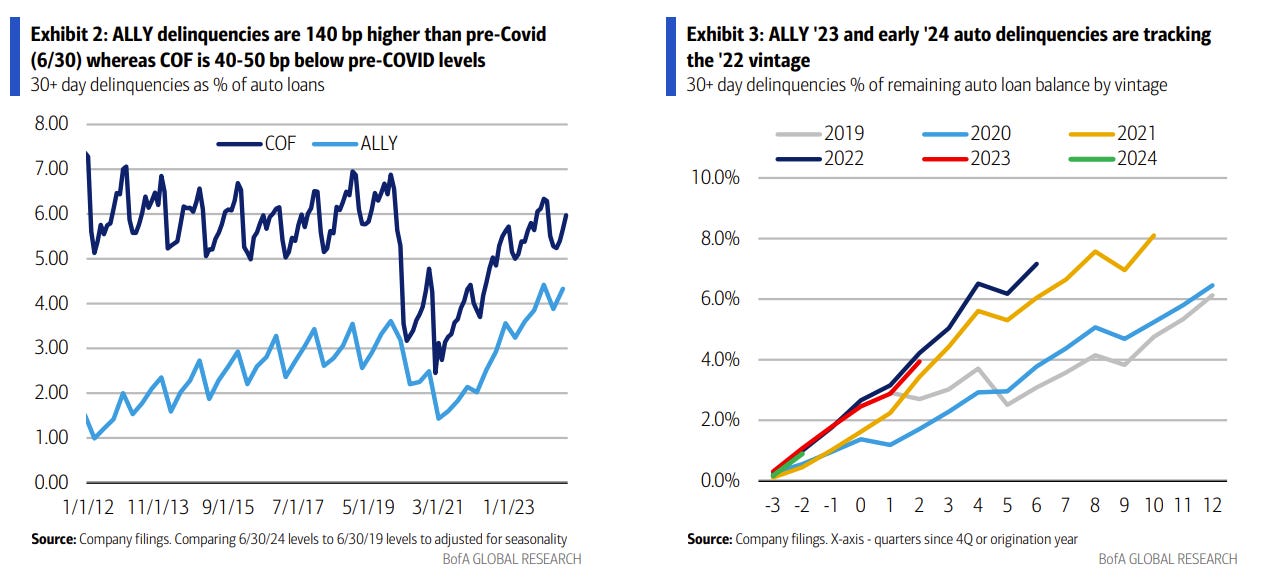

Consider for a moment Ally’s delinquency rates:

Ally’s delinquencies are definitely trending higher than pre-pandemic, but Capitol One COF 0.00%↑ (a leading subprime lender) has lower delinquencies than before.

OK, so maybe Ally got greedy and loaded up on lower quality credits.

Nope.

CapitalOne continues to have a substantially higher share of subprime borrowers than Ally:

Ally’s book is only 29% low fico, compared with CapitalOne 47% (based on BofA’s estimates).

Another clue that Ally isn’t having a credit issue is on the righthand side of the first chart.

Ally’s 2023 and 2024 problematic vintages are starting to look like the 2022 vintage, which was plagued not by credit issues—there was no widespread unemployment, etc.—but because 2022 was the peak of zirp-driven rise in auto prices.

In general, there’s not much evidence that consumers have bitten off more than they can chew.

Auto payments as a share of income are pretty much unchanged from 2019:

Lower income borrowers are actually paying slightly less in car payments as a share of income.

So, credit scores are solid (and lower quality books aren’t trending worse), the delinquency trend is following the 2022 pattern that wasn’t credit driven, and consumers aren’t paying more for their cars than their incomes suggest they can afford.

None of this suggests that Ally’s delinquency issue is a credit issue. It’s possible that somehow Ally selected for a specific cohort of borrowers that despite their credit scores is suddenly running into trouble, but that’s not obviously the case.

So, if it’s not credit, then what else might it be?