Paying top dollar because no price is too high

Two of the GOATs ruminate on the state of the stock market

what’s a bubble, anyway?

nowhere up to go . . . but who said anything about reaching the top?

the greatest earnings show on earth

the $400B AI revenue gap

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. Paying top dollar because no price is too high

Two of the GOATs of market commentary, Michael Cembalest and Howard Marks, published new memos recently, and naturally they are both worth reading in full.

Cembalest’s especially is so chock-full of goodies, that I’ll likely do a separate post, but for now, I’ll focus on one specific thing: bubbles.

Or rather, in contrast to Optimism Unbound, both Oaks and Cembalest raise some good questions about the enduring nature of today’s skyhigh valuations. Neither is explicitly bearish—pretty much every Cassandra has learned their 2023 lesson—but they do variously wonder how much longer this could go on, and what sort of room for error might there be.

Starting from the top

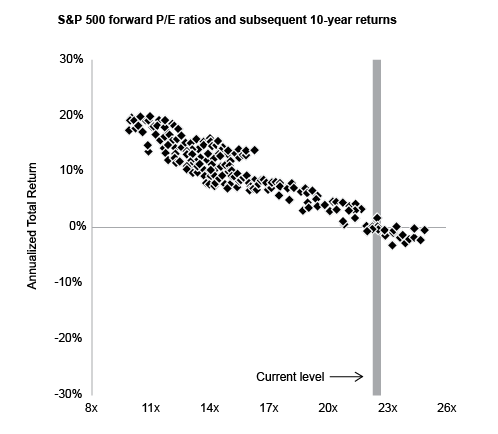

A good place to start is where Mark’s memo ends: a striking chart.

Mark’s memo is a rumination on the nature of bubbles, which he believes bear the following characteristics:

It’s the last point—the “conviction that there is no price too high”—that’s most instructive for present purposes.1

“No price too high” is most instructive because, as Marks points out, it’s very hard to generate returns if you start from a high price, and today’s prices, are quite high.

As it happens, starting from a high price does, in fact, precede poor returns:

The 10-year returns from a starting price as high as ~23X earnings—which is the price we’re paying today—is almost always flat or negative (and never very good).

In other words, if you’re buying a share of future earnings (which is what buying stock is), then paying 23 times present earnings is (a) in the top decile of price; and (b) historically followed by little or no appreciation.

And the relationship between price and future returns is pretty darn linear—the higher the price, the weaker the returns.

Now, past performance is no predictor of future results, but it does mean that present-day stock prices are vulnerable to any downward revisions in price and/or a slowdown in earnings growth (which is also the kind of thing that leads to a revision on price).

But who said anything about reaching the top?

The good news—and now we move over to Cembalest—is that earnings growth for the beating heart of the S&P (i.e. tech) is outta this world.

Bet on earnings growth? Don’t mind if I do!

Just look at these charts: