Random Walk at Night: Real Estate Dispatch

Checking in on some bold claims, and following the storks and smart money to great new horizons

It’s not exactly a graph-dump, but it kind of is. If you like real estate, then you’ll like the latest edition of the Real Estate Dispatch, this time in Four Dispatch-ies.

How’s the weather?

Sell while you still can, Gramps!

Where does the smart money go?

It pays to move.

Everything reads better in your browser or in the app. The footnotes especially, and Random Walk is really leaning into the footnotes. Plus, if you have the app, you can set delivery to “app only” and then my daily barrage will feel less like a barrage. Unfortunately, substack does not yet have a “Weekly Digest” option, but I’m hectoring them aplenty.

If this email was forwarded to you, please click the shiny blue button:Random Walk at Night

Real Estate Dispatch

#1. How’s the water? Get in, it’s freezing!

The dynamic in the residential real estate market remains largely unchanged, i.e. exactly where Random Walk said it would be.

For the new folks, here’s the rundown. For the existing folks, skip ahead.

I. What Random Walk doth foretold

Higher rates mean that homes are worth less than they were before because that’s what happens when the purchasing power of your would-be buyers takes a header. This is simply true. Don’t fight it. It just is.1

Home equity is unequivocally less valuable than it was before, but it will, however, take some time for those declines to be reflected in price indexes.

Why?

For one thing, there’s very little buying and selling.

You see, no one likes to sell at a loss, if they don’t have to. Homeowners would rather stand pat (until either rates go back down, they lose their patience or lose their jobs).

This isn’t a “supply shortage” (because no homes have disappeared), it’s just loss-aversion, and hope for a better tomorrow.

For another thing, the industry is well-practiced at hiding price declines.

Rather than lower “comps,” sellers will use various concessions to lower the price of a home (without appearing to lower the price).

Eventually, though, slowly but surely, prices will start to come down and price cuts will creep up.

Why?

Time. People get impatient, need to move for professional or life reasons, or maybe lose their jobs (but thankfully that hasn’t been an issue). People also die, and older folks own a lot of homes.

Supply builds. Homebuilders are still out there putting new inventory on the ground (because they don’t care about asset appreciation), and as they get a larger share of the action, price discovery will find a way (although homebuilders are also hiding price declines with regular use of rate buydowns).

How far prices fall depends on how high interest rates are, but my guess is at least some mean regression (if rates are 3-5%) or lower (if persistently higher than that).

In the meantime:

homebuilders will continue to clean up, as the only game in town;

Likewise, if you were a “Build to Rent” or Single Family Rental operator who snapped up inventory when rates were still low, then you start raising rents—but still nothing close to the monthly mortgage payment someone would have to pay to actually purchase the home at the price it’s supposedly worth;

refinance activity will be non-existent because despite all the equity supposedly trapped in homes, no one will touch it at prevailing interest rates.

II. What has been said, has come to be

So, how we doing?

Existing homes continue to not-sell:2

Refinancing is nonexistent:

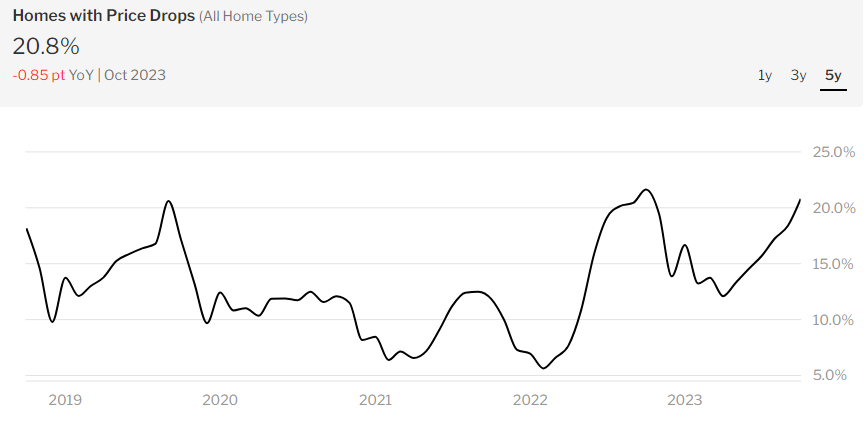

Price drops continue to rise (and realtor’s data was substantially higher at 37.6%)

Seller concessions remain elevated (although not as elevated as before):

Cancellations are higher than they’ve been (although that could be because people think rates are going down):

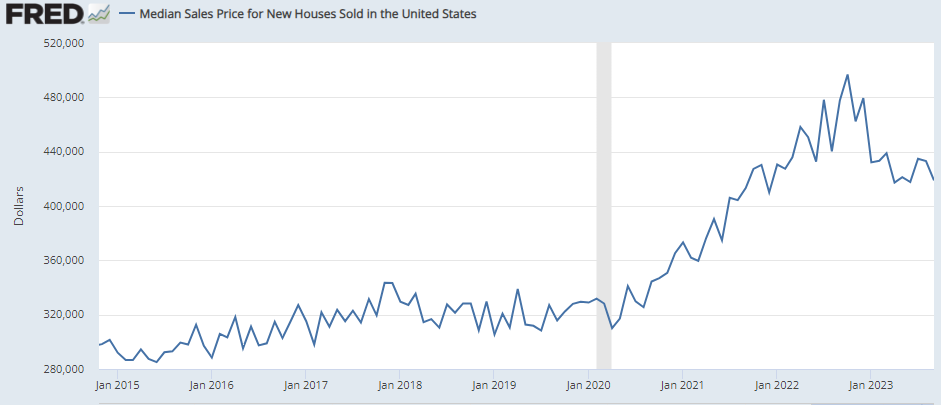

Homebuilders are ~35% of the single family inventory and using buydowns of 250-300bps to disguise discounts, and the median “sales” price of new builds continues to fall (albeit with some seasonality):3

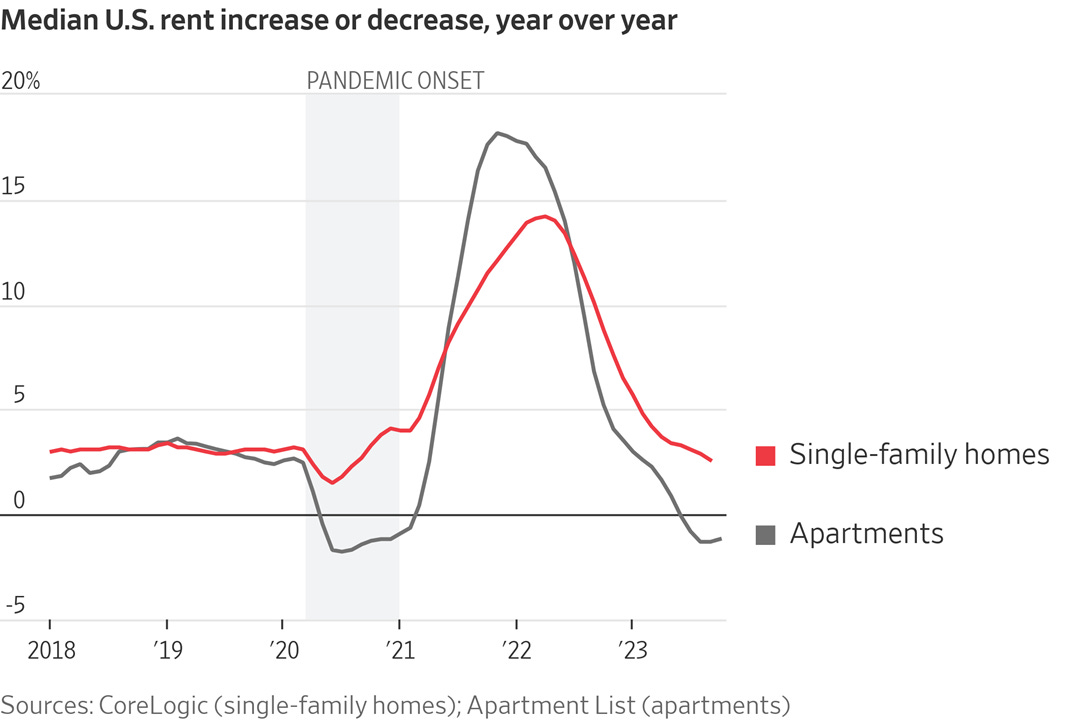

Finally, while institutional investors have mostly stopped buying homes at these prices (more on that below), the rents they charge creep up ever so slightly, and certainly more so than multifamily rents:4

The last point about rising rents for single family rentals is interesting and a thing to watch. Institutional borrowing costs are not protected by the 30-year mortgage, so they will go up, and those costs will be passed to renters (eventually).

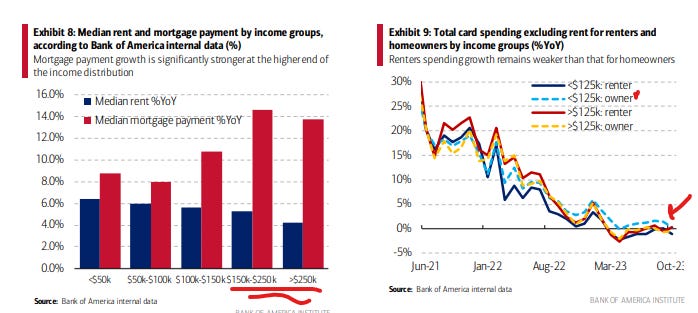

For now, basically the only people buying homes are relatively wealthy people, who hopefully can afford it (likely with the help of their wealthy parents):

All the major mortgage payment increases are concentrated in high income households (who, interestingly enough, have cut their spending elsewhere to compensate)—the dashed blue reflects card spending by owners, which until recently, had some cushion on renters, but that cushion has now disappeared.

Anyways, put it all together, and I think we’re doing alright.

Where might things go from here?