The other very expensive industrial policy

The $9T experiment in energy transition bumps along

the actual reason that the stock market sold off

a counter-cyclical indicator? finally found one

solar’s very slow (and expensive) transition to power

tariffs are a rounding error in the scheme of economic engineering

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. First, sign up for your free trial of AlphaSense, because why wouldn’t you?

A plug for our sponsor, AlphaSense

AlphaSense is actually an amazing one-stop-shop for:

expert calls (especially since it acquired Tegus),

company-filings, and

analyst research;

plus, it’s got a pretty neat generative AI-search tool that I’ve been playing with a lot (which makes searching across the corpus of information much easier than before).

It’s a genuinely fun and very useful platform, and as part of the sponsorship, Random Walk readers have ACCESS TO A FREE TRIAL, which you’d be a fool not to try (just by clicking through the link below):

FREE TRIAL! FREE TRIAL! FREE TRIAL!Give it a shot. It’s a great platform.

The other very expensive industrial policy

Random Walk continues to think that tariffs and “policy uncertainty” are closer to frenzied-media diversions than prime movers, at the moment.

Tariffs will certainly provide some near-term cost headwinds, and DOGE layoffs will make some tiny subset of the consumer population a little more cautious, but the notion that either (or both) represents some dramatic turn in economic conditions is just dumb.

I feel like a broken record, so I won’t belabor the points, but a slowing-narrow labor market was already cause for concern, and Gross Domestic Healthcare was already unsustainable.1 Those may well worsen, but (a) that’s got nothing to do with tariffs; and (b) there isn’t too much evidence that either has worsened all that much.

Working part-time for economic reasons (i.e. “need the money”) did rise a bit:

Part-time for economic reasons is back to where it was in August (and well-below historical levels).

That’s at least an actual cyclical indicator that went the wrong way. But otherwise, no sudden change to fundamentals that I can see, but feel free to correct me, if I’m wrong.

The main reason that the stock market has sold off—and to be clear, that’s really the only bad thing that’s happened, thus far—is that tech stocks were priced historically high in relation to their earnings. That only makes sense, if you expect earnings to continue to grow rapidly. That only makes sense, if you forget that 2024 was a comeback kid relative to the doldrums of 2023, and assume that 2025 will ‘meet and beat’ with the same alacrity.2

Perhaps 2025 will be another banger year for earnings growth, but in the early innings, the signs are pointing to some regression:

The median full-year guide for SaaSCos is only 0.1% higher than consensus estimates, so far.

In other words, some high fliers are telling investors to moderate their expectations, and that’s causing valuations to fall sharply.

And companies like Box, CrowdStrike, TradeDesk, and MongoDB cannot plausibly blame moderating growth expectations on tariffs. Some of the payment companies or consumer-adjacent names? Sure, ok, maybe a little. But for the rest of them, it’s just “tough comps,” as they say.

The other very expensive industrial policy

Anyways, relitigating the ‘tariff doom’ isn’t really the point of this post.

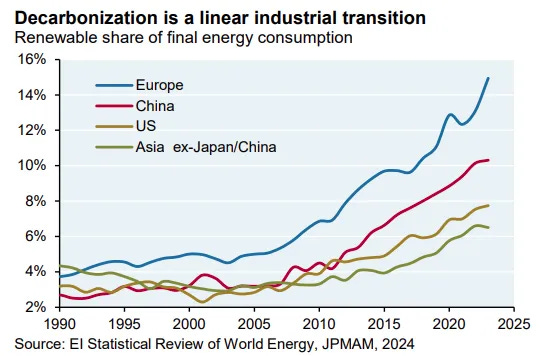

The point of this post is to remind everyone of another very expensive undertaking in social and economic re-engineering.

I’m referring to the electrification of everything, which let’s stipulate (fairly, imo) is motivated by very noble intentions, in the main.

It is also ~$9T endeavor thus far (over the past decade), and proceeding very slowly, relative to its broader ambitions:

Renewables are less than 8% of US energy consumption, and growing linearly.

Becoming “solar powered” is going to take an awful lot of time and money, unless things speed up substantially: