But who will lend to the lenders?

Are banks becoming shadow banks by lending to shadow banks? Is that even bad?

checking in on banks playing it safe

turns out, banks are lending to non-bank lenders a lot, including private credit a lot, a lot

turns out, defaults are, in fact, rising (especially when you know where to look)

turns out, this all appears to be just fine, actually

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. But who will lend to the lenders?

Random Walk has written variously about banks getting boring.

Or rather, banks ceding a substantial amount of lending activity to non-bank lenders, aka “private credit” aka “shadow banks.”

It’s an evolving landscape, with more than one underlying cause, but certainly part of shift is/was driven by a desire to make banks safer, or really, to make deposits safer, by limiting what kinds of risks lenders-who-use-deposits-as-a-source-of-capital (aka “banks”) could take.1

The goal would be to leave the more exotic risks and financial engineering to the non-bank lenders. Put investor capital at-risk, instead of depositors, and we still get credit-creation, without all the devastation to savers, if things go wrong.

It’s not an all-bad idea, by any stretch, and it’s kind’ve “worked” in the sense that private credit has taken on an increasingly large role in net-new lending (and the biggest private credit platforms are developing the kind of scale and sophistication that used to be the exclusive dominion of the largest banks).

Anyways, one wrinkle in the “leaving banking to the non-banks” safety effort is that age old question “but who will lend to the lenders?”

It turns out that banks aren’t lending directly, but they are, in fact, lending to non-banks, with increasing frequency.

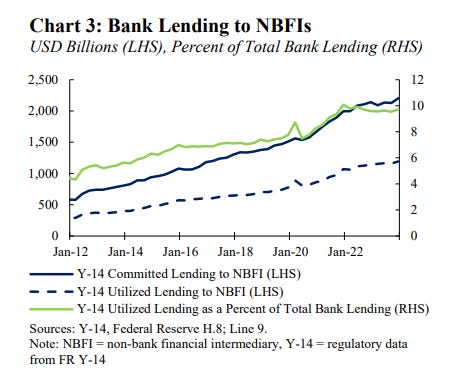

Banks increasing their exposure to SHADOW banks

Another recent report by the Boston Fed puts some more data around bank exposure to non-banks.

Lending to non-banks is now at ~$1.2T (with committed, but unutilized financing at ~$2.2T):

~$1.2T in lending to non-banks is ~2x what it was before the pandemic.

The $1.2T is ~10% of overall exposure for the banks, so that’s not that bad. If you account for the committed, but unutilized funding, it rises to 32% of overall exposure, and that’s quite a big more.

That a lot of that committed-but-uncalled capital is likely “break in-case of emergency” contingency financing, e.g. letters of credit, means that the fat-tail risk is, well, fat.

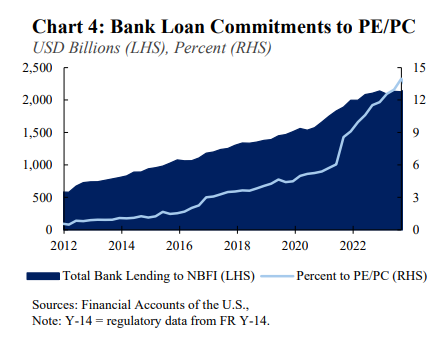

To be clear, however, only a small fraction of lending to non-banks is going to private equity/credit sponsors specifically, i.e. the Apollos, KKRs, and Blue Owl’s of the world.

Bank loans to Private Equity/Credit are about $300B, or ~14% of that ~$2.2T (and 25% of that ~$1.2T).

OK, so maybe not a “small” fraction, depending on how you feel about ~14%. Plus, that’s ~2x more than it was in 2021, so bank lending to PE/PC has grown rather quickly.

But, it’s manageable, and regulators are very much on top of this, in a fashion befitting regulators: doing research, disseminating information, generating public goods. Apparently the IMF is doing a deep-dive on PIK loans, so that’s good too.

Credit markets seem just fine

Also, as best as Random Walk can tell (and I do check), private credit lending seems to be performing, a-ok.

The latest cut from the leveraged loan market tells pretty much the same story: things are generally fine.