Let's see what the Cycle Dragged in

Ruminating on regime change

the two bottlenecks of the new cycle

the great industrial rotation

sectors that win (and those that don’t)

capital heavy rises again

follow the yields

workers where we need ‘em, if we can find ‘em

$killed Trade$

insurance premium premium

‘hey small spender’

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.Let’s see what the cycle dragged in

This is a long-ish one, but Random Walk invites you to take a break from the show in Hormuz to ponder the new cycle. Consider it something of a reformulation of some longer-running themes, with some fresh data to back it up.

The two bottlenecks

One way to think about the next cycle (or really the current cycle) is that there are two bottlenecks that are two sides of the same coin: (1) workers; and (2) worker-enhancer/substitutes (i.e. compute, energy and robotics, and yes, software too).

Without a steadily increasing supply of people to do things, there will be an increasing premium on the people who can do things, and/or technological alternatives to getting the work done. That premium, of course, assumes we’ll keep finding new things to do, even though the slower growth of new people will challenge net-new demand, which it surely will.1

On the other hand, what we won’t really need more of is the stuff that people buy, especially big durable stuff, like cars, houses and refrigerators. Likewise, we’ll see a (continued) shift away from big expensive goods and services, and towards cheaper stuff/experiences, and of course, healthcare . . . lots and lots of healthcare.

Finally, the stuff/service providers who operate most efficiently, will likely accelerate their share-gains relative to the ones that don’t—if the pie isn’t growing, then the inevitable move is to take a larger piece of the pie. Winners will win, but even more so than before.

Random Walk can’t/won’t noodle it all out in one post alone, but I’m planting this flag as a noodling-point for future noodling on these themes.

For now, we’re already seeing the cycle play out in a few ways, for better and for worse, so let’s dig in.

The great industrial rotation

The first sign is the great market rotation to industry, i.e. the infrastructure (and people) making all the worker-enhancement/substitutes possible. If machines are going to carry even more of the load going forward, then the mechanized substrate is in desperate need of a glow-up, and the market is all over it.

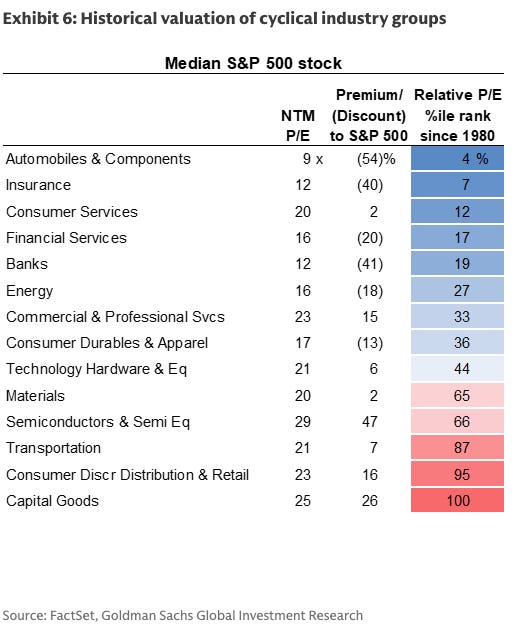

The cycle’s new winning sectors

Consider the shift in cyclical multiples and where they stand in relation to the broader market:

Of the big cyclical sectors trading at a premium to the index, we have:

Semis;

Capital Goods; and

Consumer Discretionary (which we’ll return to at a moment).

Materials aren’t trading at much of a premium relative to the index, but the relative price of their earnings is somewhat higher than its been.

In all events, the rotation leaders make sense. The premium is on the industrial glow-up.

In terms of the laggards, those would be cars, consumer services, insurance, durables, and fin-services. That too generally makes sense, insofar as those businesses are linked to the consumer economy (in the main), and that’s not the growy part.

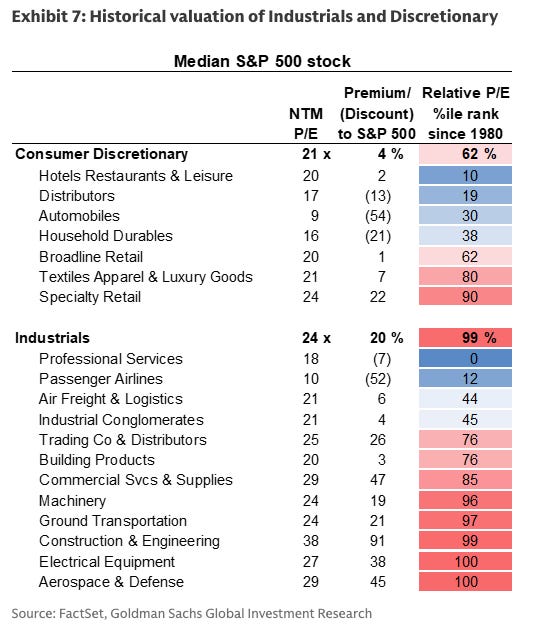

If you double-click into consumer discretionary and industrials it becomes even more obvious:

Of the winners:

it’s all the commercially oriented industrial sub-sectors, like electrical equipment, construction, etc.;

e-commerce adjacent;

aerospace & defense; and

luxury and specialty retail (again, more on those in a bit)

Of the losers:

planes, hotels, leisure;

cars and household durables; and

professional services;

That too mostly makes sense.

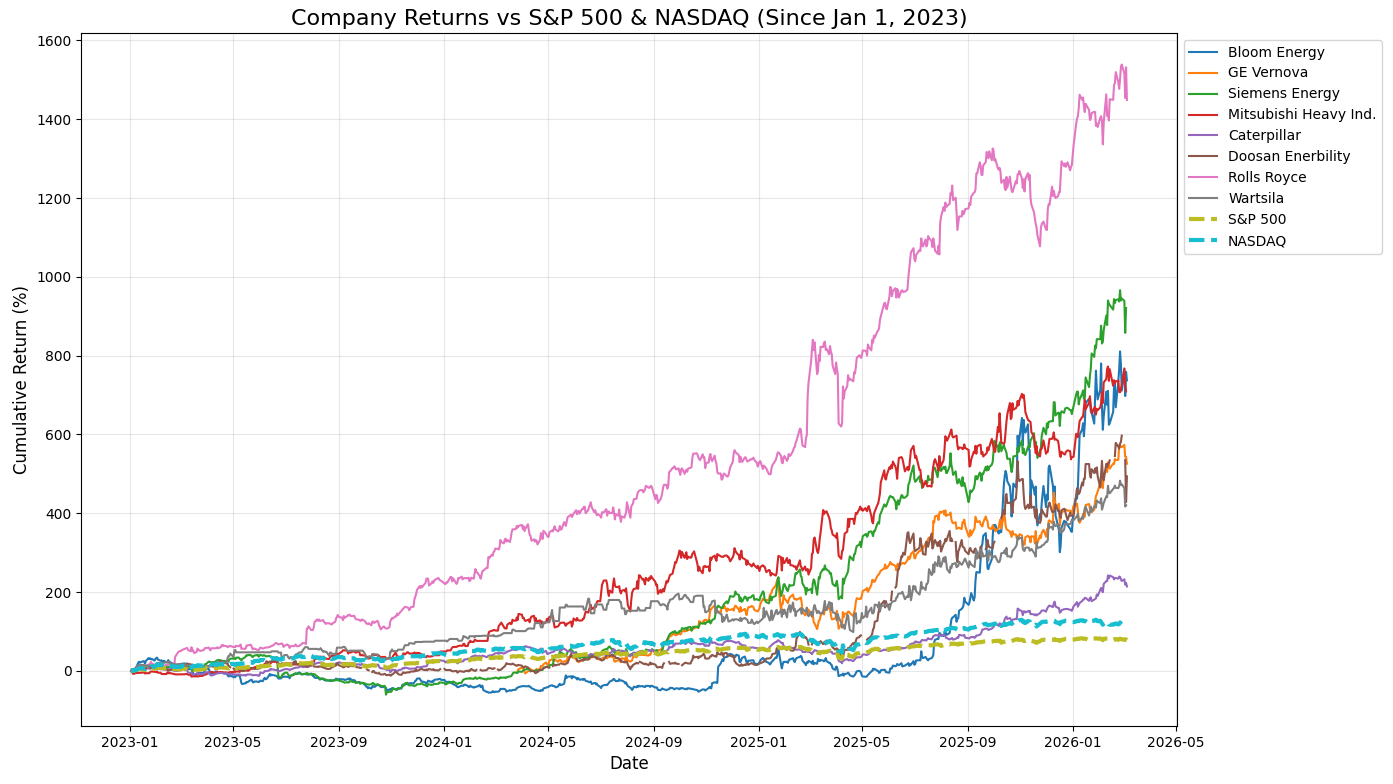

All the money flowing to the big industrial buildout, and the scarce labor to make it happen, is cooking up some big things for the gridiron heroes (and not the football kind).

You want to invest in the US industrial supply chain of goods n’ services? There’s an ETF for that ($PAVE). Oh, you manufacture gas turbines? Put on your party hats because company has arrived it comes bearing gifts:

No one can get enough of the big expensive stuff necessary to build data centers and the electrification of everything.

That’s quite the run for some historically pretty sleepy cyclical businesses (that have mostly been around for a long time). For a market that’s been dominated by high-flying tech names for so long, it’s a pretty remarkable thing.

On the other hand, for those businesses selling anything but cheap stuff to a slow-growing consumer market (ideally online), you’re not feeling the love. There are some exceptions—like luxury and the non-cheap stuff parts of retail are surprising out-performers—but personally, I’m fading those, as driven by some part misbegotten “tariff relief,” “flight to safety” and/or “lack of better ideas.”2 To be clear, the Almighty Consumer is fine, just not overly growy.

Bigger picture, I think the market has got this mostly right, but not entirely right. Money is flowing to cap-intensive builders and sellers of cheap tchotchkes, and away from high-end consumer services and big expensive goods. Smart.

ICYMI

Capital Intensity is back (and a Capital-Light era fades)

Let’s ruminate for a moment on the market’s newest high-fliers (that are actually pretty old) because the gravity of the thing shouldn’t be underestimated.