Secondaries, deeper, stronger, liquider

Venture secondaries markets are growing up

a watershed moment (nearly) for secondar liquidity

hunting for whales, not bargains

deeper and more liquid, first the bids, then the asks

capital markets can innovate, and innovation is good

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.Of Secondaries and IPOs

Secondary markets are getting deeper and more liquid. Rather than complain about it, adapt and survive.

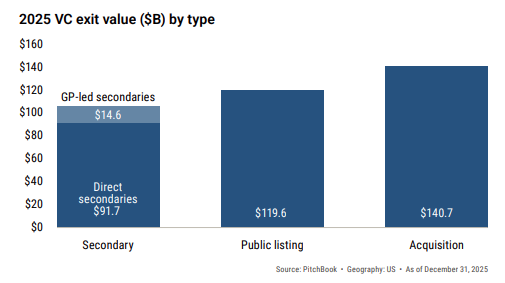

IPOs still bigger than secondaries, but barely

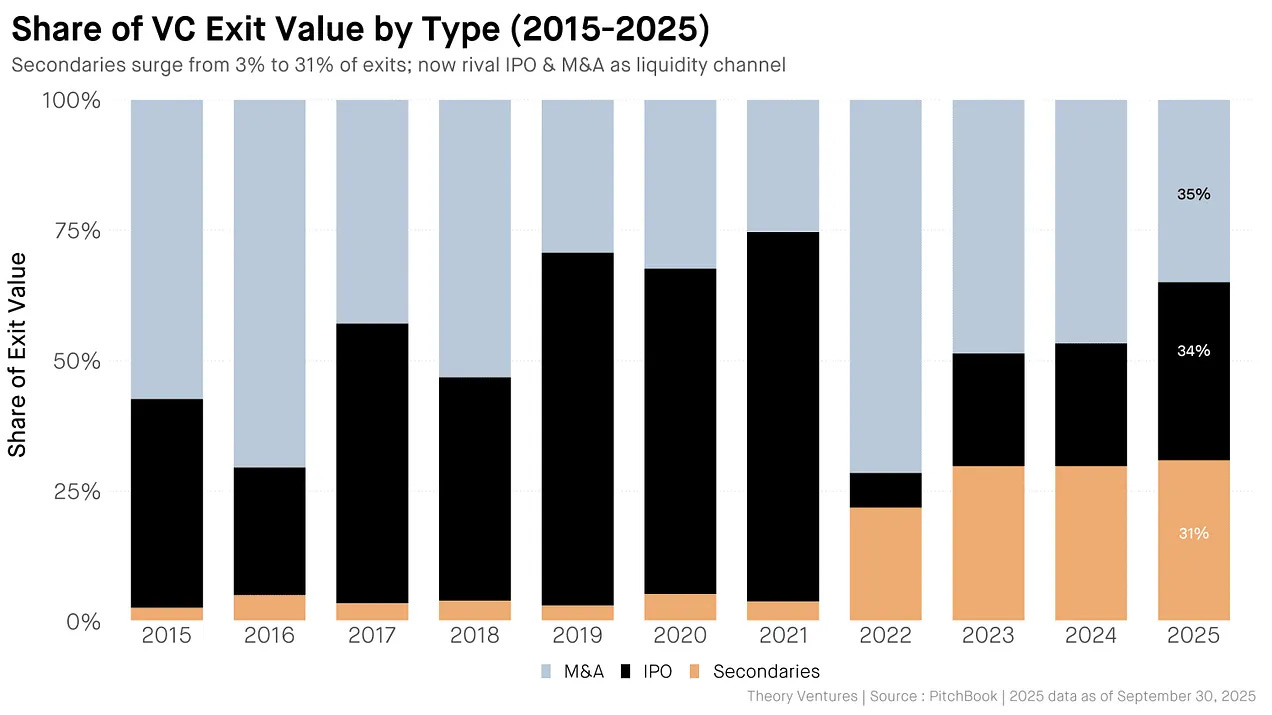

2025 was nearly a watershed moment for secondary sales.

Secondary liquidity nearly matched IPO liquidity for VC this past year:

At a 31% share of exit value, private secondary sales generated nearly as much liquidity for VC as IPOs.

Secondaries went from basically a rounding error in the liquidity picture, to an equal participant alongside acquisitions and public-market exits, in just 5 years.

Now, in the big scheme of things, secondaries are still tiny relative (~4%) to the stash of asset value currently managed by VC. As foretold, secondaries are an increasingly big deal, but they’re not an off-ramp or cure-all for the mistakes of the prior regime.

Going for alpha

Pretty much the opposite of a cure-all, really.

Secondary shares are increasingly trading at a premium, and not a discount.

Rather than go bargain-hunting (for the most part), secondary investors have trained their fire on the same 15-20 companies that everyone wants to invest in. Secondary investors are hunting whales, not charity cases.

This isn’t a bag-passing exercise. It reflects an evolution of the private side to compete with publics.

Public markets aren’t closed. Private markets have simply gotten larger to meet the capital needs of the best companies, who, all things being equal, would rather not have to deal with the headache of going public, if they don’t have to. And so they don’t.

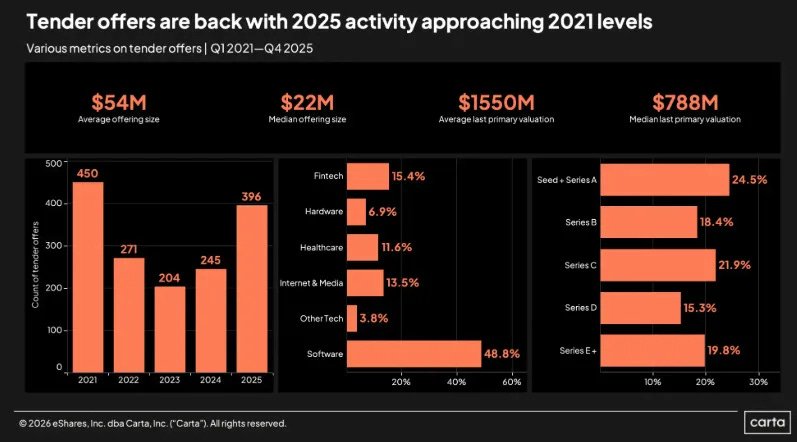

Oh, you need some secondary liquidity to keep your employees happy and fed (tired, as they are, of waiting 15 years for an IPO)? We gotchu:

2025 tender offer volume nearly recaptured peak-ZIRP highs.

By getting bigger, private investors get privileged access to the hottest action, and private companies get capital, without all the public market strings attached. Supply meets demand. Adapt or die, public markets.

Lots of people can complain about companies not going public (and want to blame VC or the companies themselves), but capital is capital, and if private capital comes with less unwanted baggage, then public capital needs to up its game.

ICYMI

Deeper and more liquid (and therefore deeper, and soon, even more liquid)

The other interesting thing is that private capital’s relative advantages are self-reinforcing (and therefore will continue to compound, with time).