The marks aren't high enough?

Notes and charts on the current price(s) of equities

tech is cheap(?)

unprecedented weirdness (with perhaps good reason)

terminally less-impressive?

it’s memory all the way down

private marks are too damn high and/or volatility-laundering to the downside only

. . . but maybe not?

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.The marks aren’t high enough?

Ruminating briefly on equity values, public and private.

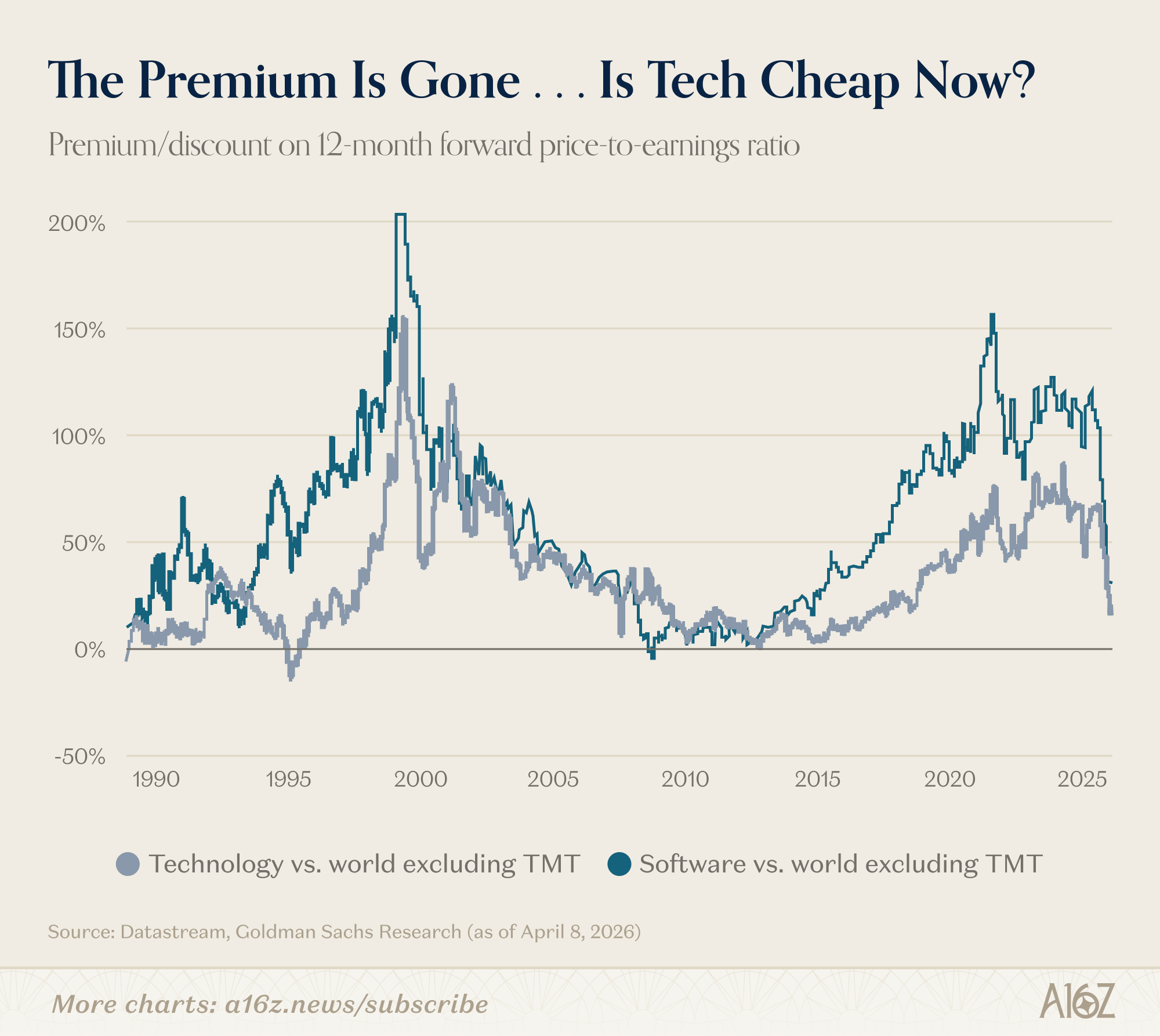

Tech is cheap?

Random Walk has alluded to this before, but the stock market has been a little odd lately.

It’s somewhat less-true recently after the big ceasefire(ish) melt-up, but it’s pretty rare to see earnings expectations skyrocket, while share performance scuffles. The only way that happens is if valuations collapse, given that share price is simply the product of earnings x the price of those earnings.

Unsurprisingly, valuations and earnings expectations tend to rise (and fall) together: if earnings go up, valuations rise (and vice versa). What’s happened recently, however, is the opposite of that—earnings are going up, but valuations are plummeting.

And really, it’s a tech story:

Forward earnings multiples for software have lost almost the entirety of their premium (relative to the rest of market), just as earnings expectations continue to grow—and not just grow, but grow at 2x the pace of the field.

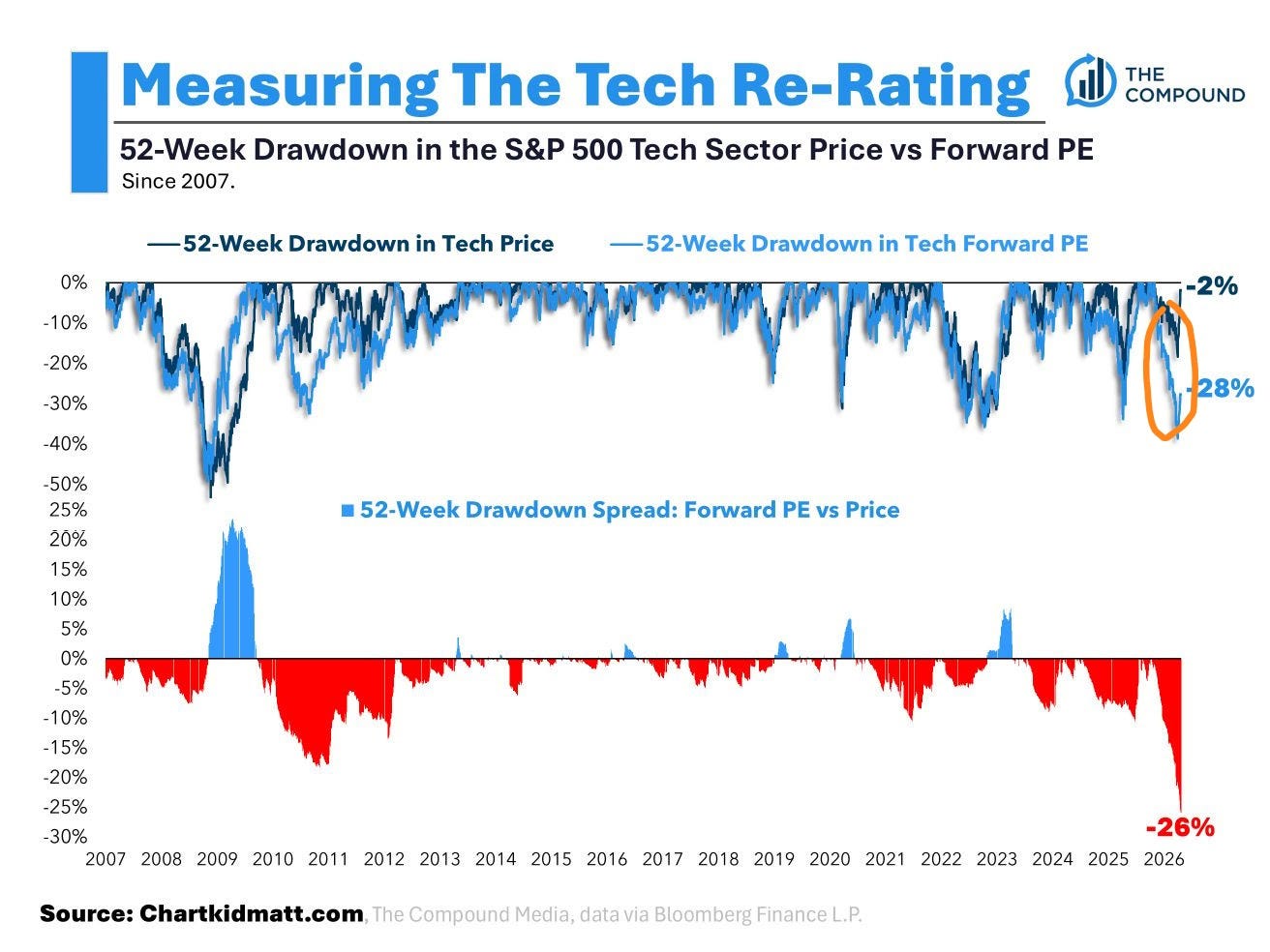

Robust profits, with declining multiples, leads to weird observations about market performance, like this one:

Multiples on tech have dropped ~28%, while tech share performance fell only ~2%, leading to an unprecedented divergence in the series.

In other words, when the light blue line falls (multiples), the dark blue line (performance) usually falls too: multiples contract on relatively poor earnings results, and so share price falls accordingly . . . but if only multiples contract (while profits stay strong), then the blue lines separate.

And, as you can see, multiples and performance generally don’t diverge like that—post-GFC is the only period that comes roughly close.

Which is to say that someone is probably wrong. Either earnings will not, in fact, continue to grow (and share prices are too high), or earnings will grow (and share prices are too low).1

As it happens, post-GFC, the bears were definitely wrong:

If you were chastened to the sidelines by the stock market collapse in 2008, you would have to admit, with the benefit of hindsight, that there was no “collapse” at all.

So, the lesson here is “buy, buy, buy,” right? Perhaps.

ICYMI

Software terminally less-impressive(?)

It’s of course not necessarily the case that “someone is wrong.”