Binge-Drinking With Your Pa

5 Idea Friday: private for longer; AI-ROI; ETFs to the moon; and China's retail winter

5 Idea Friday

binge-drinking is popular with some people

a different theory of private for longer

frictionful AI, and more tales from the ROI unlock (or not)

ETFs to the moon

China’s retail winter

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.1. Go Ahead and Binge-Drink

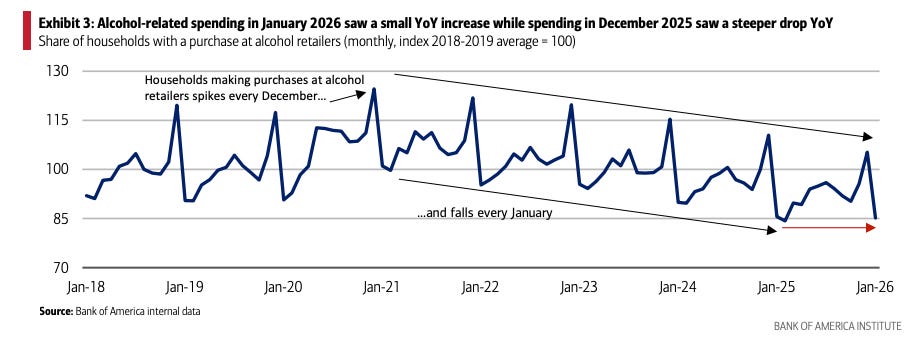

It’s father’s day this weekend, and while it’s true that drinking, in general, has been in steady decline, it’s not true for everyone.

Alcohol spending has dropped ~15% below the pre-pandemic baseline, but at least the decline appears to be stabilizing.

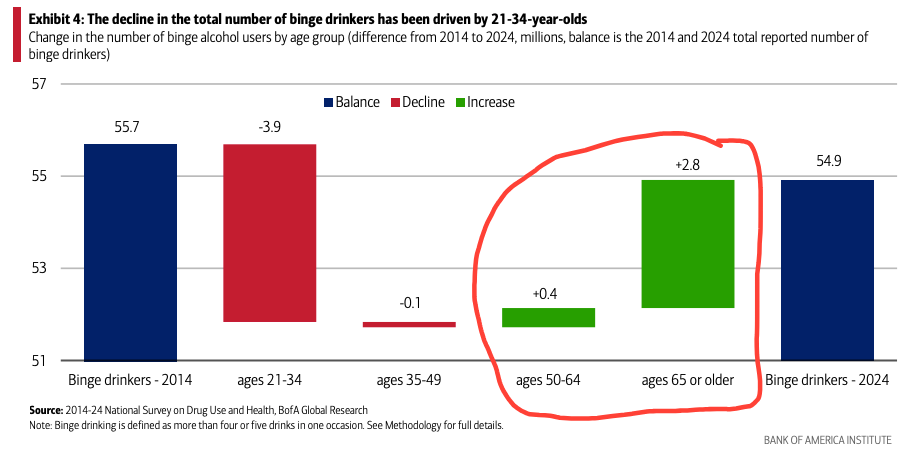

The number of binge-drinkers has also declined, but it’s the young-folks doing all the tee-totaling:

There are 3.2M more binge-drinkers aged 50+ than there were back in 2014.

So, maybe as a paean to your aged pa, tie one on for the weekend. Or something.

ICYMI

2. A theory about ‘private for longer’

Generally, there are two components to the observation that private companies are staying private longer.

The first reflects something of a structural break: private cos are ripening on the vine longer because the bid-ask on an exit price is too wide. Funds would like to sell, but not at prices that anyone is willing to pay.

The second reflects something of a structural shift in the comparative advantage (or not) of public markets v. private ones: companies are staying private longer because private capital has risen to meet the primary public value proposition (i.e. the sheer magnitude of capital needs), and all else being equal, being private is better because there’s more alignment with investors, less QoQ volatility, less regulatory tax, and less short-termism.

In other words, why go public if you don’t have to?

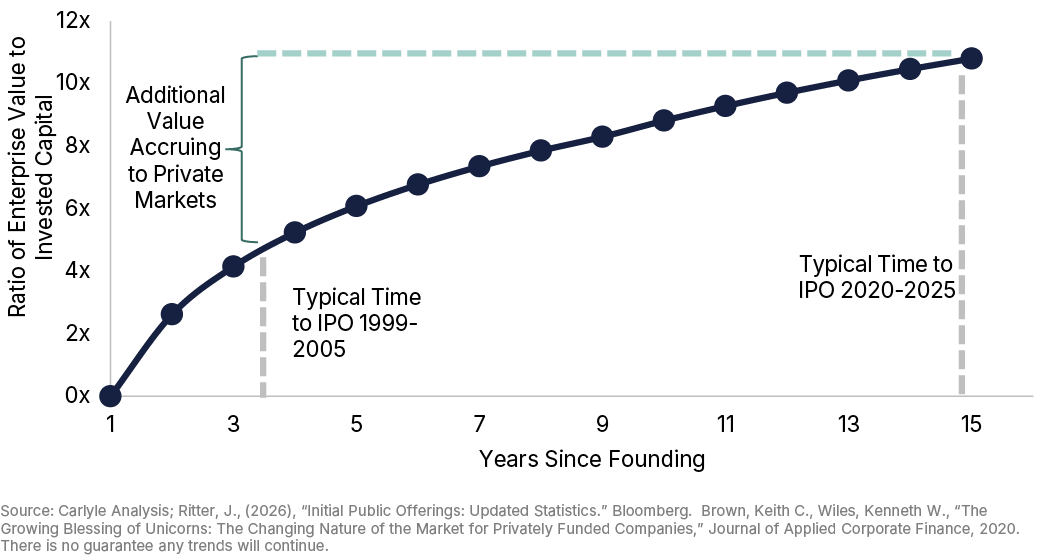

The net-result of all of this is that an increasing amount of enterprise value is accruing in the private markets:

~50% of the appreciation that used to happen in public markets is now happening on the private side (according to this analysis, at least).

Query how much of that shift is driven by the rate regime shift (that drove peak private valuations, only to be followed by a drawdown on the public side), but either way, the point stands.

There is, however, a somewhat different theory about private-for longer that I recently discovered, and it has to do with disclosure regimes.

The idea is that companies stay private to avoid sharing their intangible assets with the competition

Companies rich in intangible assets – proprietary technology (e.g. reusable rockets), production methods and know-how, advanced algorithms, etc. – want to avoid public disclosures that hand rivals (or would-be competitors) a template for expropriation . . .

Private markets resolve the tension through nondisclosure agreements. Investors can learn everything they need to underwrite the business, while preserving a degree of confidentiality unavailable in a public context.

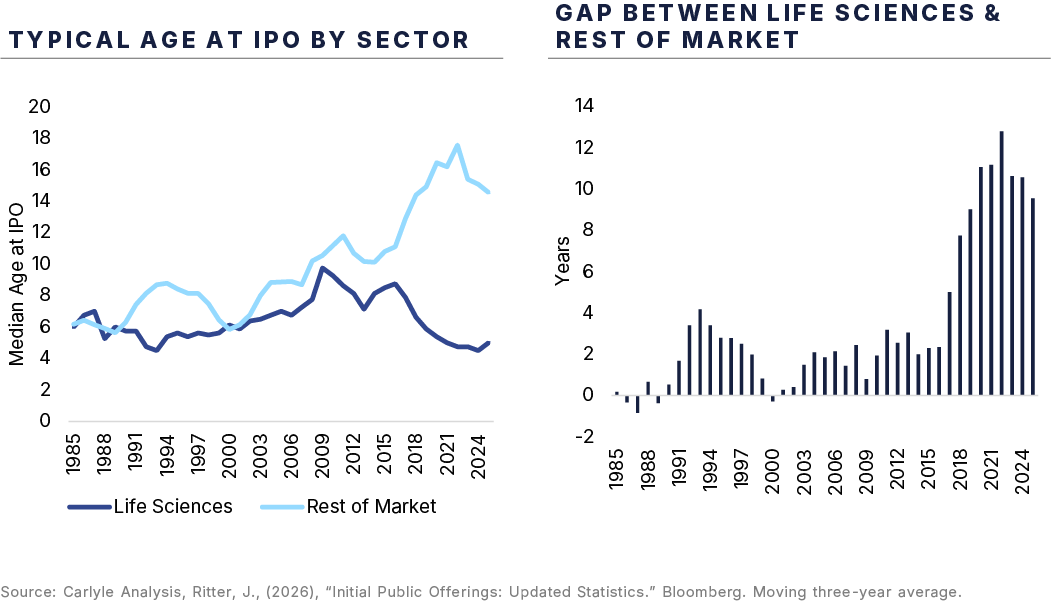

The evidence for the theory is “life sciences,” where the exception proves the rule.

Life sciences enjoy a patent monopoly on their strategic goodies, and lo’ and behold, they go public a lot sooner than the rest of the market:

Life science companies have actually been getting younger since 2015, even as the “maturation gap” blows out ~4-6x wider than before.

So, where disclosure comes with IP protection, companies are happy to go public. Where it doesn’t, they do not. So the theory goes.

I’m not entirely persuaded by the theory because life sciences are different for a whole slew of other reasons, including having their own niche pocket of the capital markets, as well as a more binary set of outcomes . . . but, I like new theories, and this one was kind of fun.

ICYMI

3. Frictionful Intelligence (reprise)

Some quick follow-on observations regarding the propensity to spend on AI, what it means for AI to drive value, and expanding the surface area of demand via the “real world,” as a crucial unlock.

Mass market tapped?

First, on the mass consumer point, Random Walk posited that it seemed likely there was less pricing power and/or room to goose to demand.

As it happens, there’s some data that households “making AI payments” declined ever-so-slightly since January: