Chart Dive on Private Credit, PE/VC

20+ charts on the private side

credit check on aisle discount BDC

credit performance looks fine?

contagion risk? not likely

long, hot, private equity summer

quiet consolidation, discounts slowly, but surely (but also, the bid-ask, still too wide)

pareto distributions on steroids. the embiggering continues, apace

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.Chart Dive on Private Credit, PE/VC

A two-part chart-dive on all things private credit, and PE/VC.

Before we begin in earnest, just one point that often gets lost in the discourse: what’s happening in these asset classes is not entirely unique (even if there are plenty of esoteric think-boy takes on the specific features of their own special strategies and cultures).

Reality is that it’s tough out there for pretty much everyone (with some exceptions, of course):

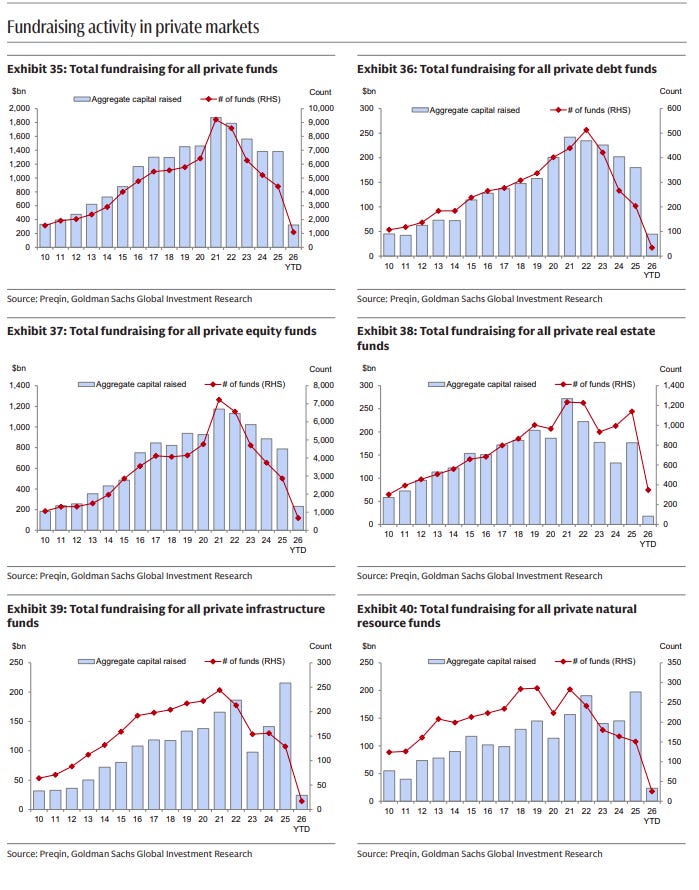

Fundraising has been tough-sledding across the board.

The exit-backlog is ubiquitous. Repricing, especially off of pandemania peaks, is ubiquitous. Concentration is ubiquitous. Zombie-funds (and zombie-assets) are ubiquitous. The new cycle is not like the old cycle, and that’s ok.

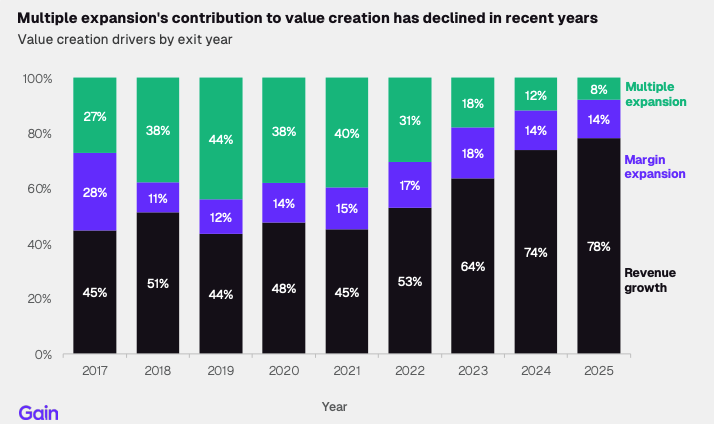

What worked before, just doesn’t work now:

Just using PE as an example, revenue (and earnings) growth is now ~2x the value driver that it was. Multiple expansion, by contrast, plays far less of a role—and this chart ends in 2025—in 2026, (contracting) multiples are almost certainly a headwind to enterprise value.

It’s not bad or good, but it is definitely different, and as per always, the only way forward is through!

ICYMI

![Uncharted waters (reprise); Almighty Consumer check; Healthcare[-fraud] GDP?; AI-Lawyering for Me; Longs, but not shorts](https://substackcdn.com/image/fetch/$s_!MpiH!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F00da6c53-cccf-43f3-b00b-ba932898ae46_429x429.png)

Credit Check in the Discount BDC Aisle

Rightly or wrongly, private credit (and especially software-backed loans), continue to get hammered by investors:

~70%+ of Publicly traded BDCs are trading at a discount.

It’s mostly a software story, as software loans comprise the lion’s share of “distressed” loans, i.e. those trading at 70 cents or less on the dollar. It’s also mostly a ‘21-’22 era software loans story, as those were the ones made at peak pandemania, when revenue growth was ripping and credit was close to free.

Credit performance looks . . . fine?

The strange thing, however, is that credit performance is generally fine (if not improving). There also appears to be very little discernment within software loans (except perhaps on the degree of leverage):