DOGE ftw!; Luxury woes; Manufacturing Boomlet; Real AI threat; Housing Supply is *perfect*

Five Idea Friday: featuring a manufacturing boom, and 20+ charts to carry you through the weekend

DOGE success

luxury woes

manufacturing boom-let (a chart dive)

extremely well-functioning supply-demand in housing

AI’s real threat (you’ll never guess)

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.5 Idea Friday

Some quick-ish hitters for your weekend reading pleasure.

1. The Smashing Success of DOGE

The consensus treats it as a foregone conclusion that “DOGE Failed.” This was shortly after consensus was sure DOGE was causing a recession, lol.

They’re generally quite happy about that declaration, partly because of negative polarization around the guy(s) behind it (and the sometimes icky and braggadocios comms that came with it), partly because they are champions (or participants) of the largesse that DOGE undertook to unwind, and partly because it’s fun to be mean.

It’s obviously true to some extent that DOGE did “fail.” It did not cut trillions of dollars from the budget, it did not (but also did) uncover lots of fraud, and most of all, federal spending continues to grow.

Well, sort of:

If you net out interest expenses, federal outlays actually did flatten out a bit, for what it’s worth.

Well, that’s something, but it’s too bad DOGE never got the chance to do more.1

This too is something:

DOGE really did dramatically reduce the size of the federal government, in at least one sense.

Total federal employment dropped pretty dramatically. Fewer people to gum up the works, and that’s not nothing.

And hey, since output/headcount is considered “productivity,” then I guess the Federal Gov’t is more productive now, too (lol).

ICYMI

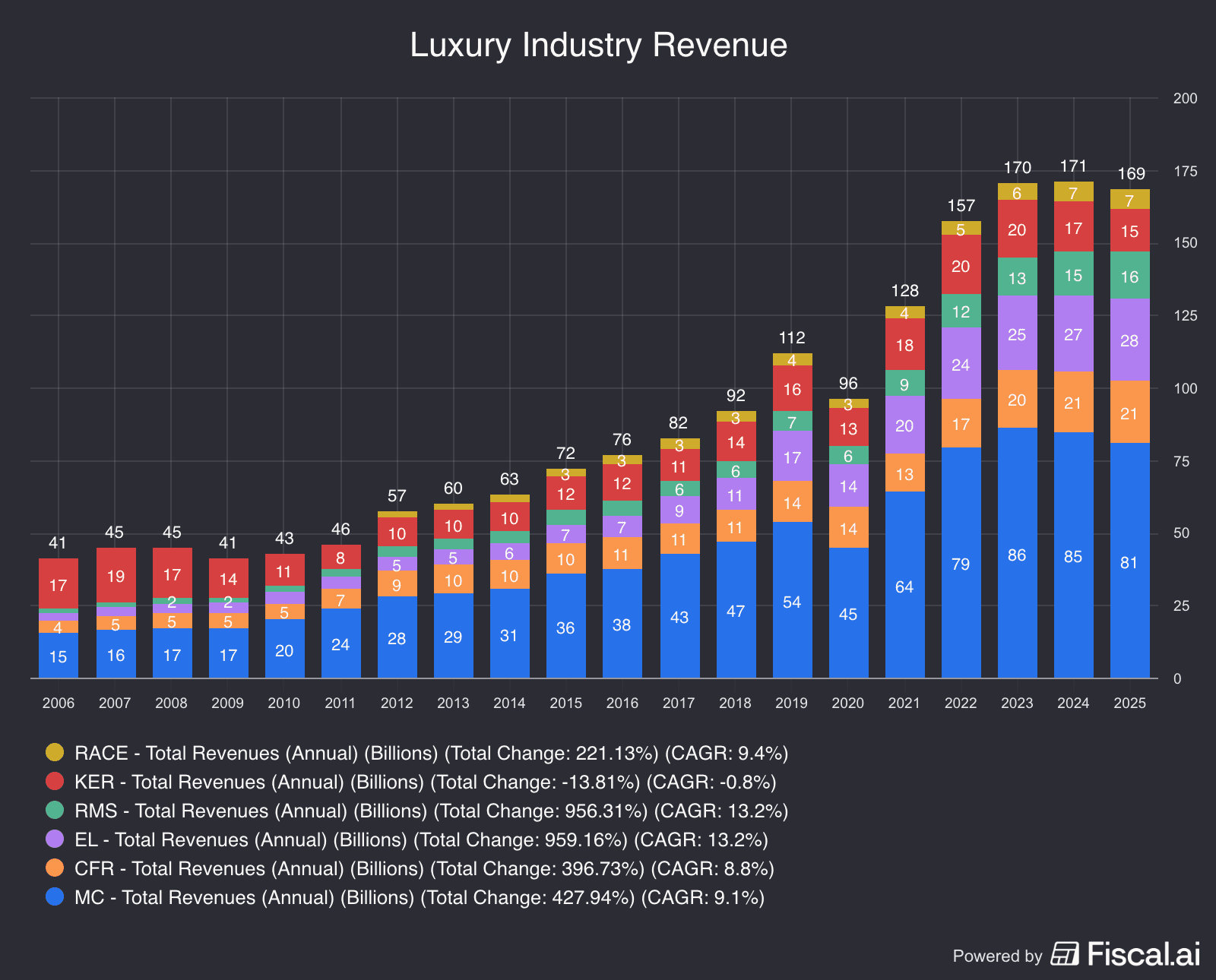

2. Luxury Woes

A few weeks ago, Random Walk laid-out the definitive take on the current state of cyclical affairs. Read the whole thing, it’s great, the best even. No need to read anything else.

But, even so, one part of my theory had some holes in it, especially with respect to luxury:

Random Walk is pretty bearish on luxury, but at the time, markets had put some wind in luxury’s sails.

Whatever. Their mistake.

Behold, luxury is doomed:

Luxury revenues have been trending flat-to-down off their peak, since ~2023.

OK, so not exactly doom (yet), but hardly an impressive picture.

My understanding is that luxury is following the airline and hospitality playbook: wring even more out of its price-insensitive wealthiest customers (while everyone else pulls back).

3. Manufacturing Boom-let

Lots of smart (and not-smart) people scoffed at the notion of “reindustrializing,” America.

We’d never bring back blue collar jobs (and who’d want ‘em anyways). Tariffs won’t make a difference—if anything, tariffs will hurt domestic manufacturing. This is all a pipedream romanticization of a bygone hard hat-era that wasn’t all that great to begin with.

There’s a lot of truth to all that, and I too share some of the skepticism.

And yet, despite all the recent turmoil (or perhaps because of it), Random Walk has some bad news for the cynics: there is, in fact, mounting evidence of something resembling a manufacturing and industrial revival.

In no particular order:

Philly PMI showing more business activity, including new orders (and more hiring and higher prices):

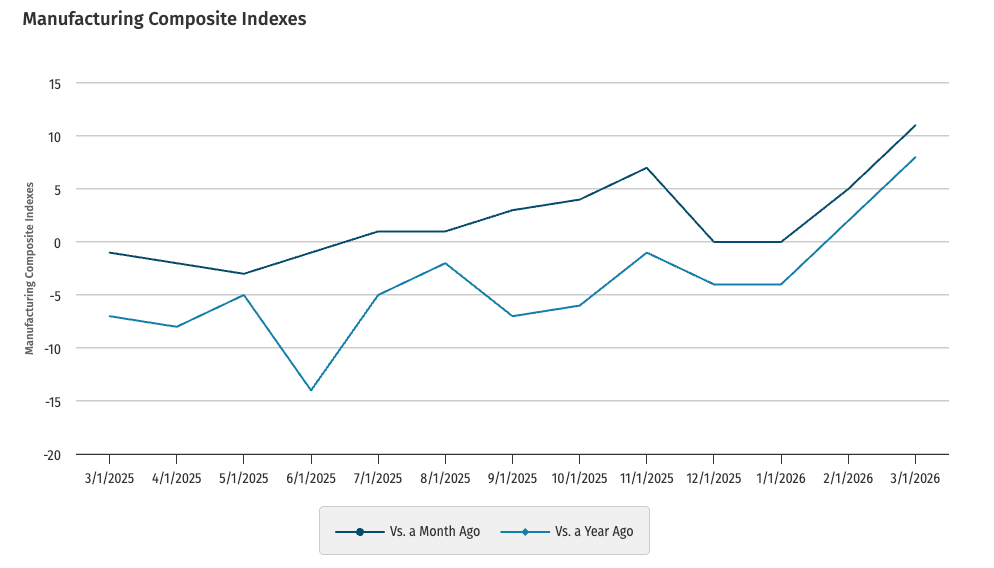

KC Fed Manufacturing Composite Index up-and-to-the-right:

Chicago Fed Survey of Economic Conditions, with yay! for manufacturing, and meh for everything else:

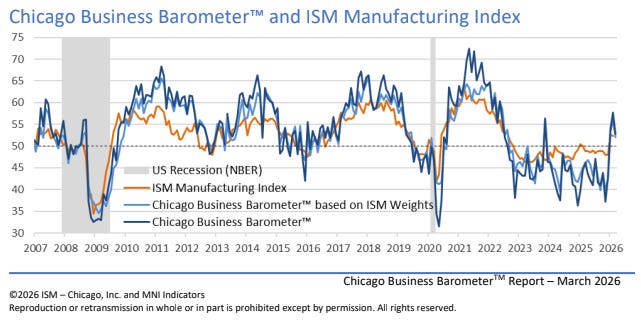

Chicago Business Barometer (which tracks the ISM fairly closely) with a big jump:

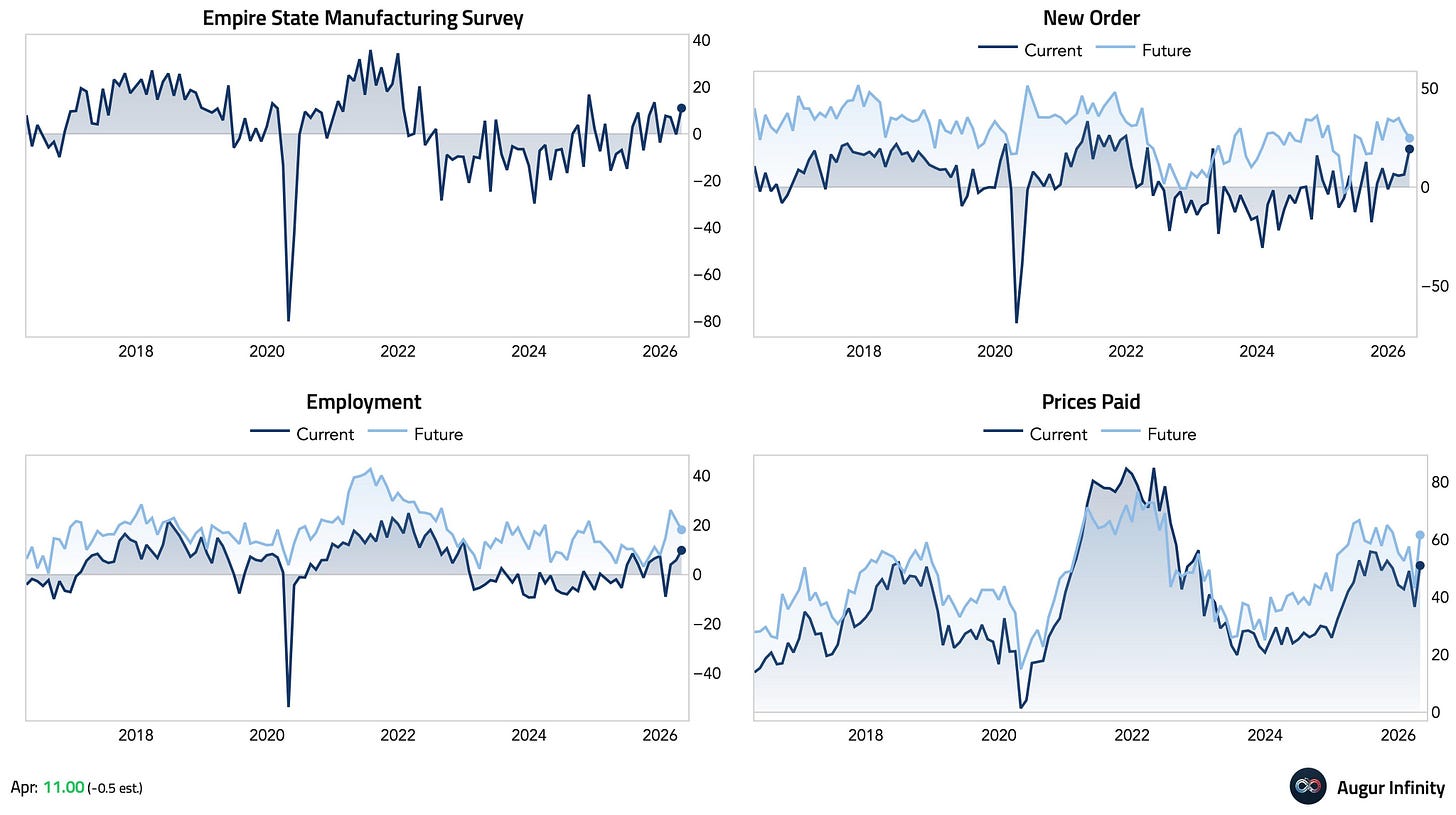

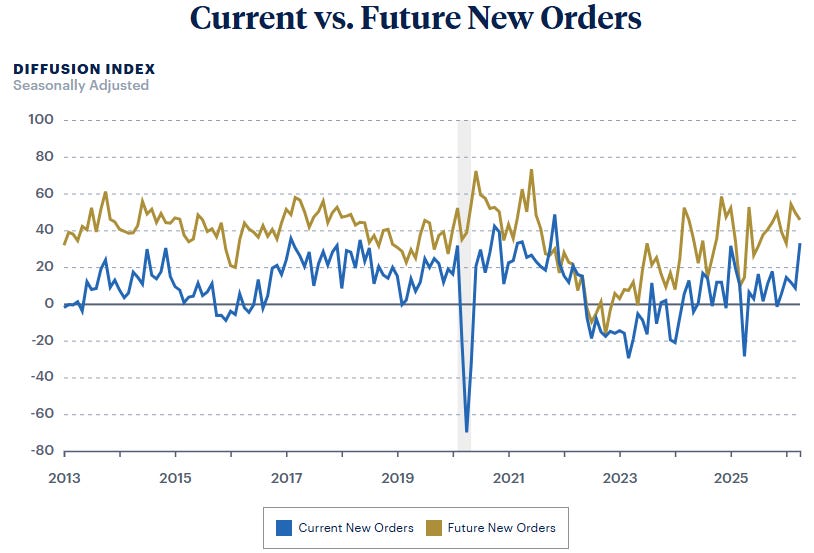

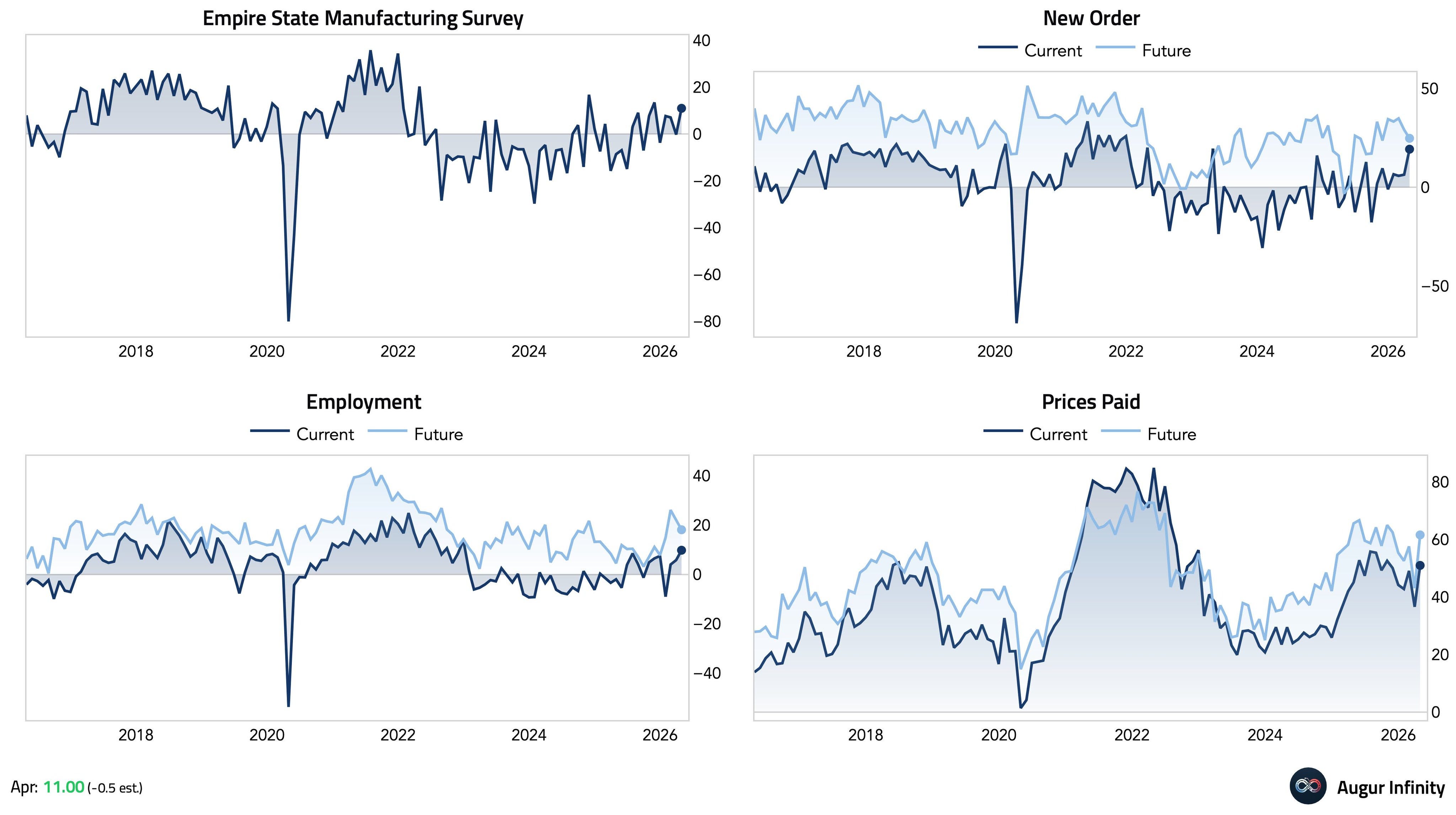

Empire State manufacturing Survey, showing a big jump in new orders, employment, and prices paid:

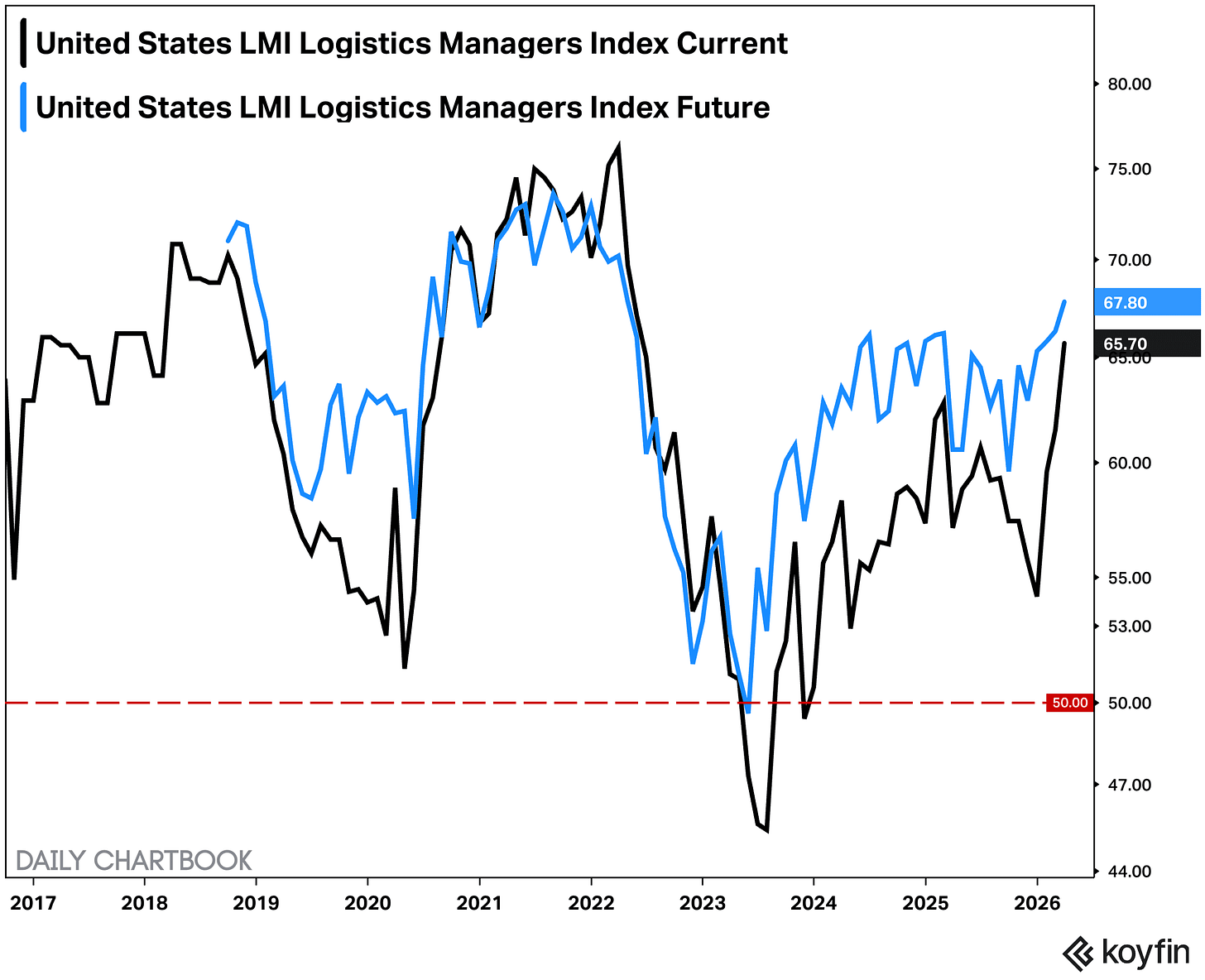

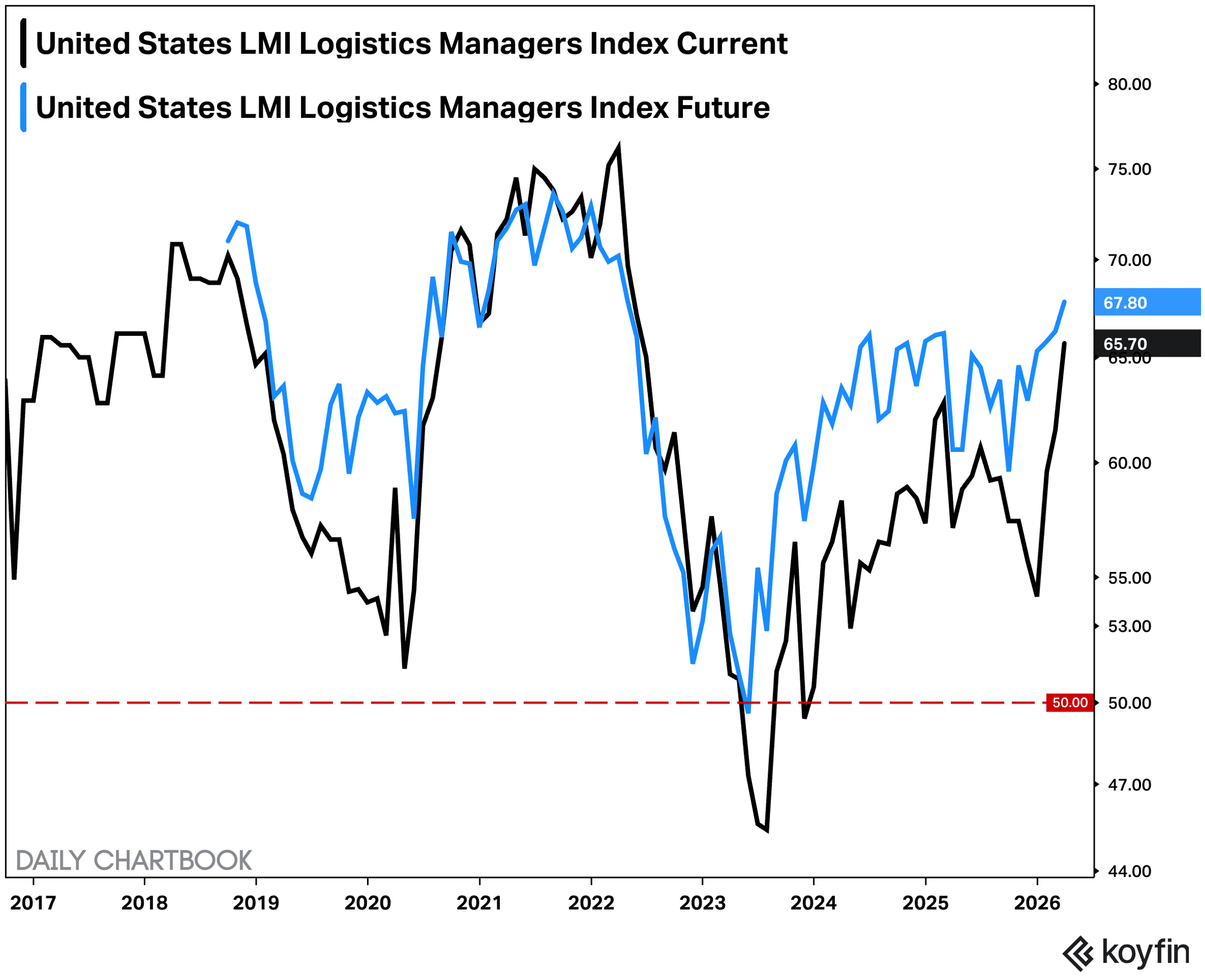

ESMS via Augur Infinity Logistics Manager Index onwards and upwards:

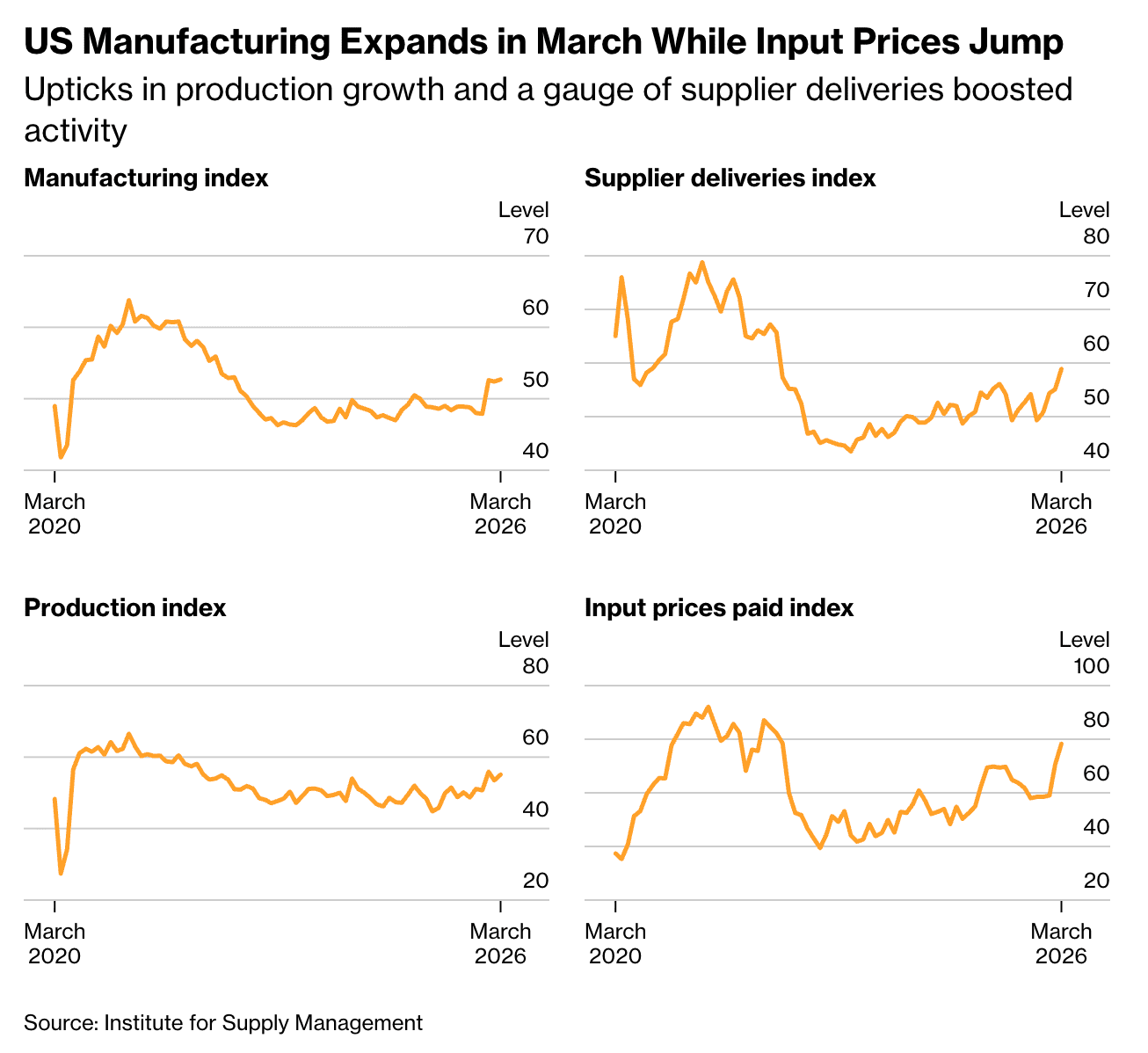

LMI via Daily Chartbook ISM Survey, with rising deliveries, production, and again, prices:

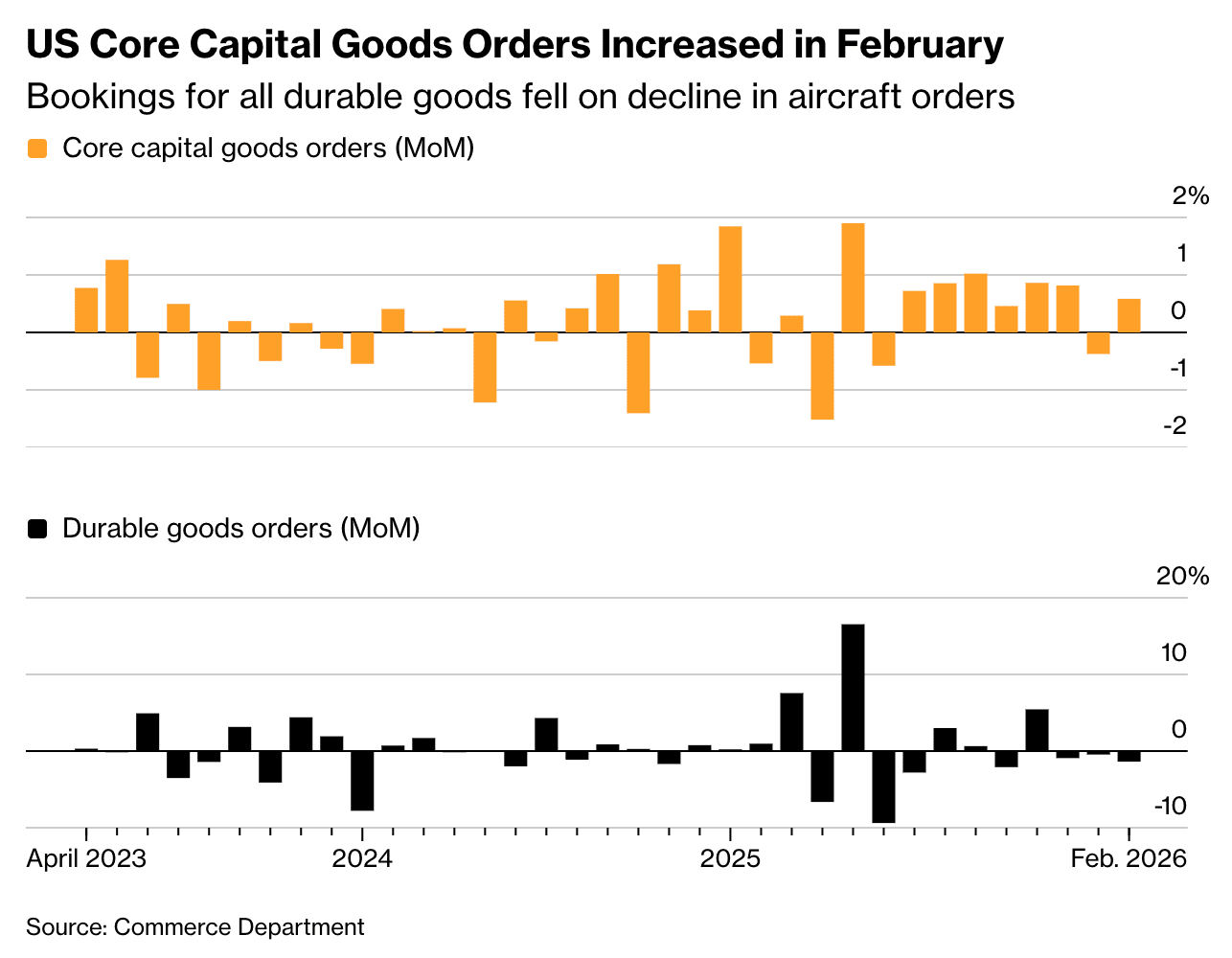

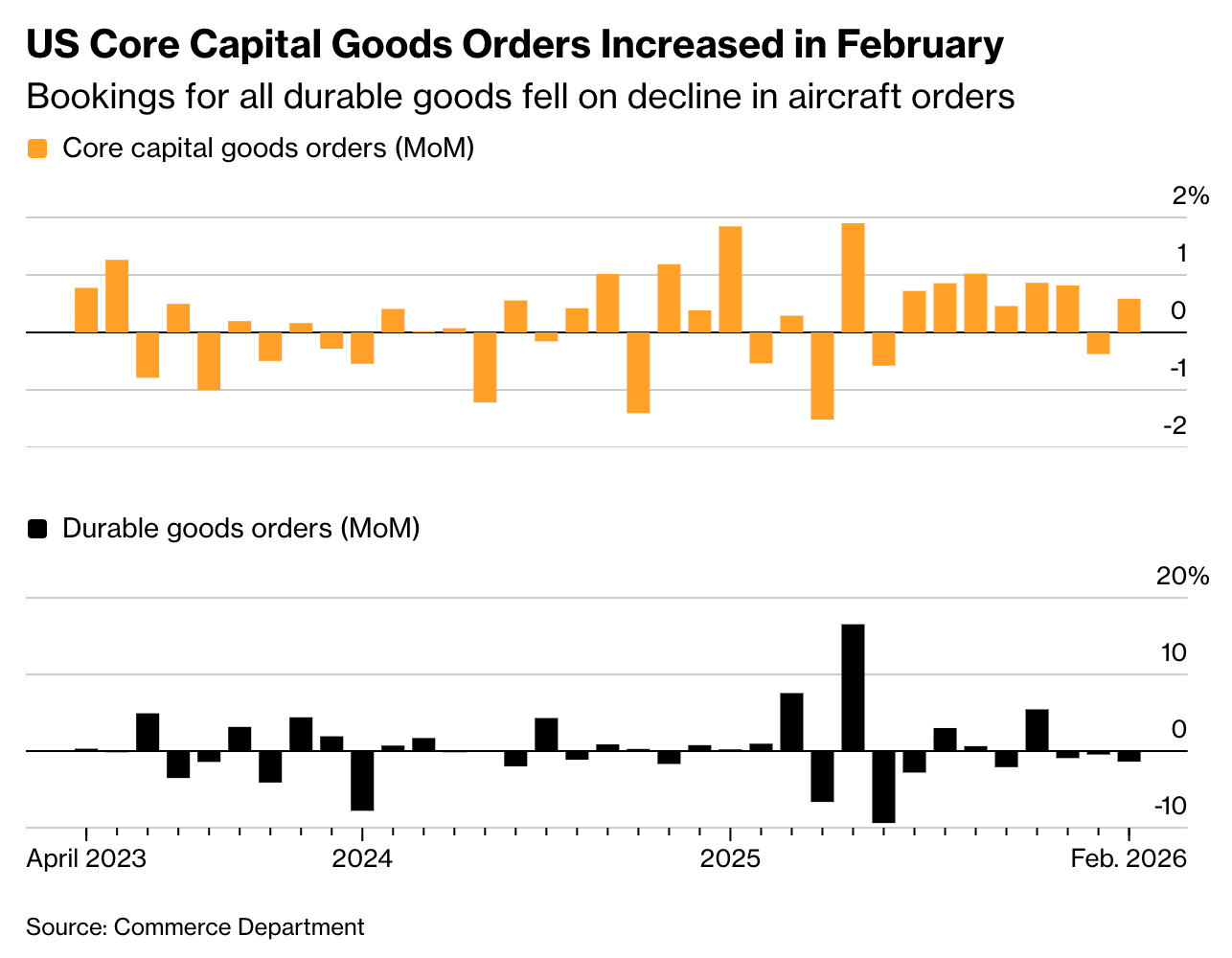

Core capital goods orders have been pretty steadily positive (while Durable Goods tread water)

Bloomberg

I could go on, but I think you get the point.

The soft stuff and even some the semi-hard stuff all point the same direction: manufacturing and industrial activity is trending upwards.

The rising demand for blue collar stuff flowed through to the freight market, as well (via Freight Alley):

Truckload volume for 2026 is trending well-above prior years:

Tender rejection rates (where a high rejection rate is usually evidence of tight supply) has climbed significantly:

Trucking rates are unsurprisingly up all over the country:

Bloomberg

Again, you get the point: there is mounting evidence that domestic industrial activity is buzzing.

It’s flowing through to employment, as well.

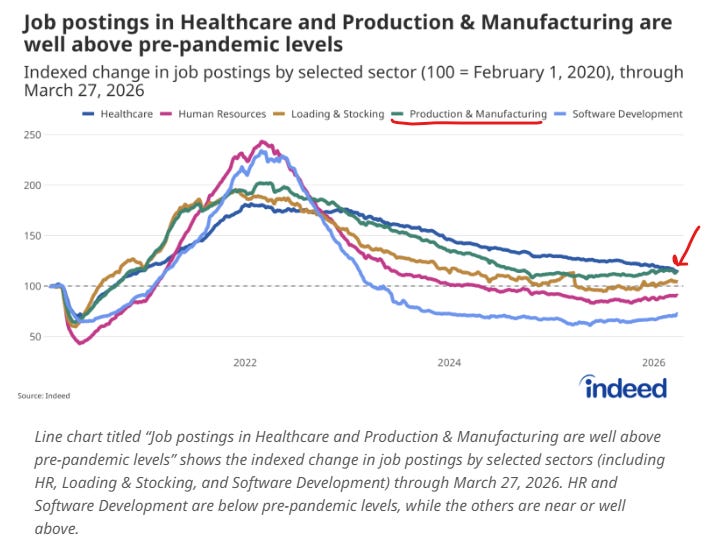

Outside of healthcare (of course), manufacturing and loading & docking are the only sectors with above-trend job postings:

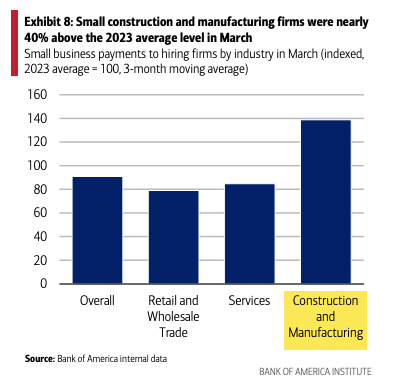

Construction and Manufacturing small businesses were the only small businesses paying more to hiring firms than they were in 2023:

Data centers have created a massive run on the skilled trades (for the umpteenth time):

Goldman Sachs

Even Jensen Huang recently noted that the real AI infra bottleneck isn’t chips, power or memory . . . it’s plumbers and electricians.

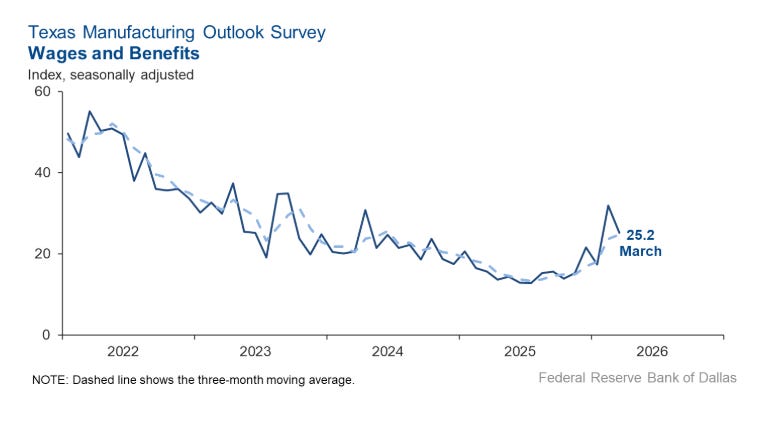

And, of course, with great hiring demand, comes great wage growth (sort of):

The Dallas Fed survey shows steady upward inflection of wage growth for manufacturing since the end of ‘25.

So, what’s going on?

Well, obviously the AI buildout surely has something to do with it. Tariffs might have something to do with it, too. There’s also probably some Hormuzian front-running, going on as well, plus some Hormuzian end-running for domestic energy.

But, also, as Random Walk has observed before, the decrease in manufacturing investment that began at the turn of the century is truly staggering, and even the slightest mean reversion—driven by labor shortages, automation, overdue glow-ups, the electrification of everything, whatever—would constitute an meaningful upward inflection in industrial activity.

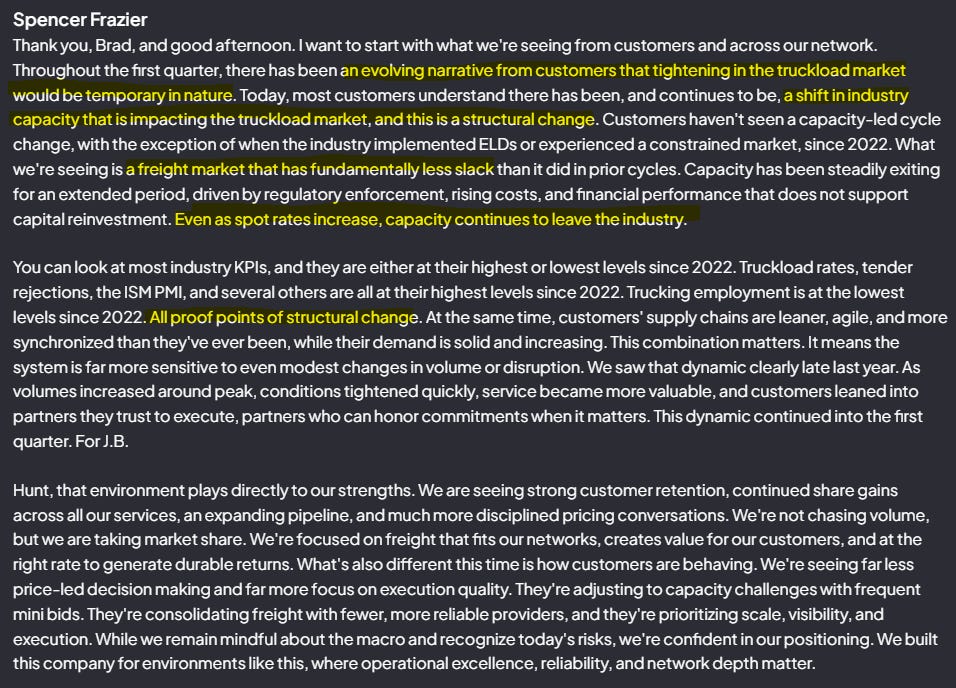

In a recent earnings call, JB Hunt’s JBHT 0.00%↑ EVP of Sales (for one of the largest freight cos) took the real or temporary question head on, and he was pretty unequivocal that this isn’t temporary:

“All proof points of structural change.”

Now, JB Hunt is talking his book. Plus, a lot of the commentary is specific to the structural changes in freight—yes, there is an uptick in demand, but there are other reasons that freight supply has decreased.

But either way, sorry haters, it seems pretty clear that industrial activity is definitely bumping.

4. Exactly the right amount of housing

Just another installment in one of the longest running Random Walk series: there is no housing shortage.

Rather than some secular shortage of housing, it turns out that housing supply is remarkably responsive to demand.

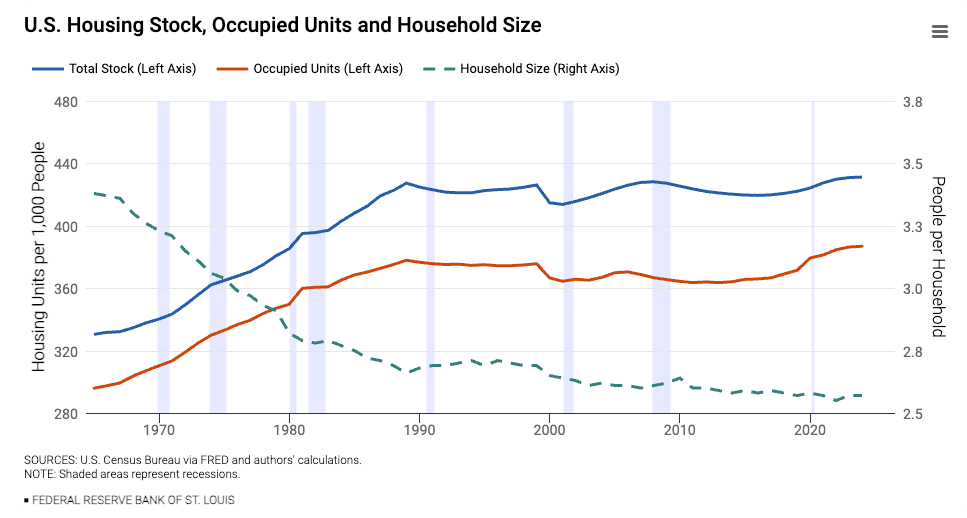

I mean, how else would housing units per capita stay so darn stable since the late 80’s (and higher than ever before):

The total stock of housing per 1,000 people peaked around 430 units in 1989 and has stayed pretty much exactly that high until the present.

Definitely no shortage there. Collapsing household size? Yeah, we got that. But housing shortage? Not a chance.

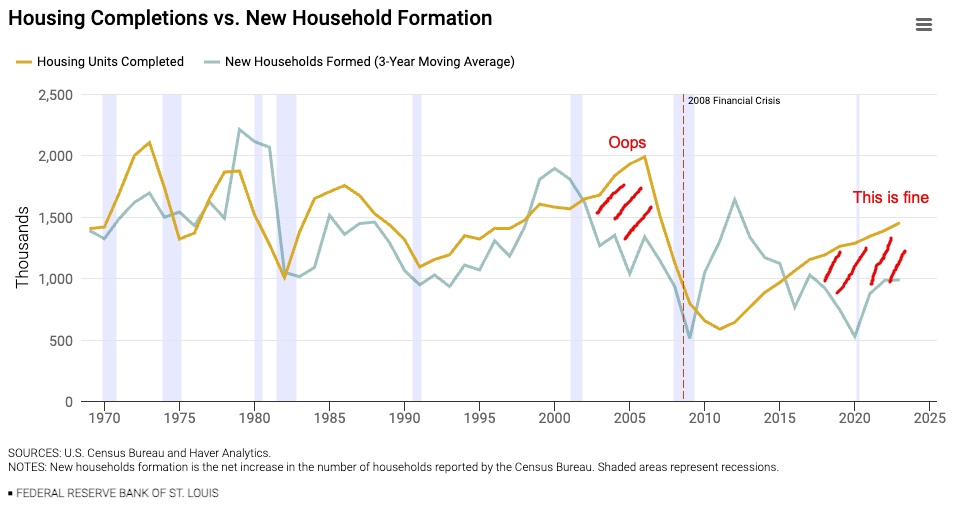

Indeed, new housing gets completed as new households are formed:

Outside of a little pre-GFC overbuilding, followed by some under-building, completed housing units have tracked household formation pretty darn closely.

. . . well, except recently, where new housing supply ran ahead of household formation, but that’s probably fine.

But yes, builders tend to build where the bodies are adding up, and when they stop adding up, they stop building . . . until the bodies add up, and then they start. Again, to wit:

Single-family permitting is down everywhere (after a big run of building, and now soft demand), while multifamily perks up (after a lull in building, precipitated by stagnant rent-growth).

They’re even building MF in the Northeast, where supposedly it can’t be done!

I mean, Random Walk told you the Palmetto State was the place to be:

Single-family permitting goes to where the people growth is, and if you think causation is running the other way, well, idk what to say.

All hail Myrtle Beach!

Anyways, more evidence of well-functioning supply-demand in housing, perhaps a moderate housing glut, and nothing at all like a shortage.

5. The real threat of AI

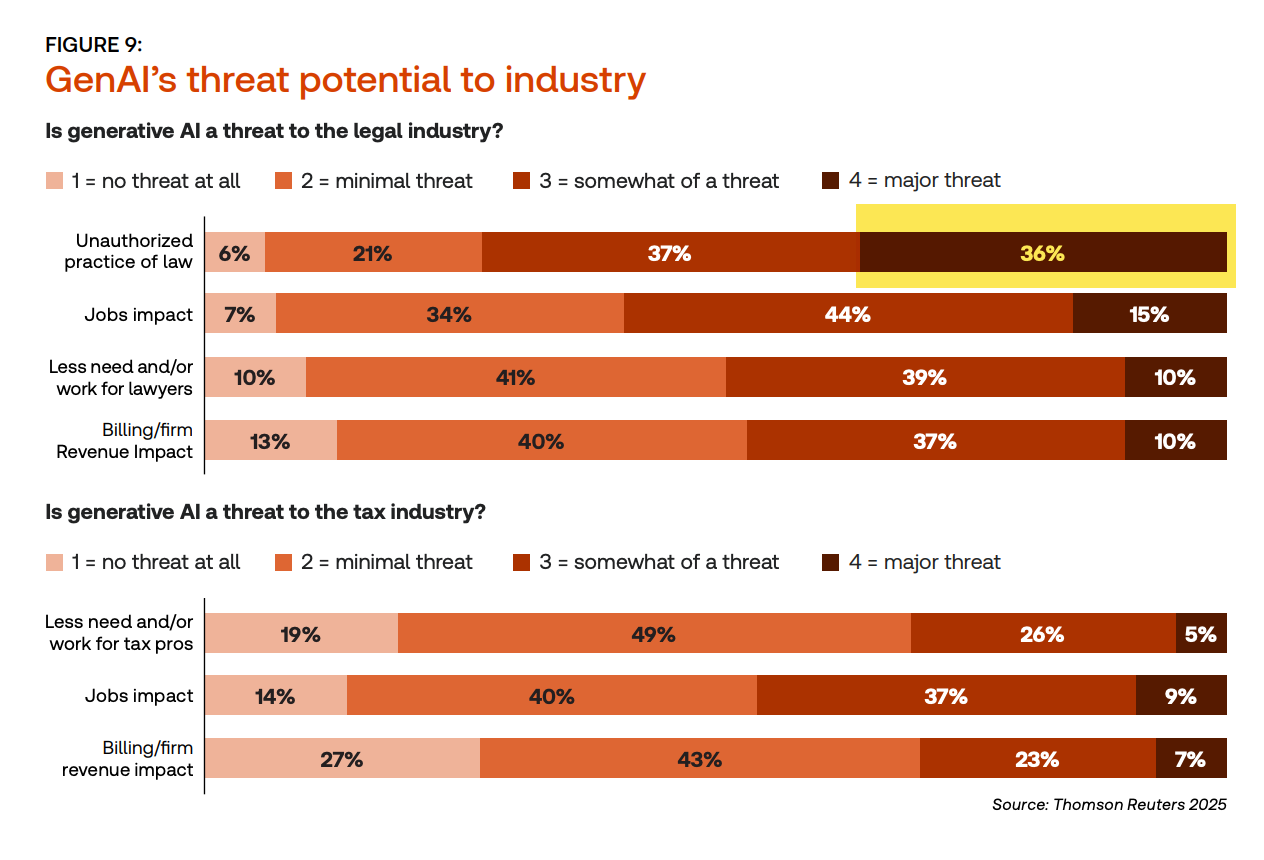

Thomson Reuters asked a bunch of lawyers about “GenAI’s threat potential to the [legal] industry” and you’ll never believe what the lawyers said:

73% said the “unauthorized practice of law,” was somewhere between “major threat” and “somewhat,” but, in all events, the biggest threat.

The lawyers are civic-minded folks, you see, and they just don’t want the normies hurting themselves by practicing law without permission. Because it’s the bar association that keeps us safe from unscrupulous lawyers, and umm, without all those horn books and law school exams, how could anyone be a lawyer in real life?

As an ex-lawyer myself, I can say with a high degree of certainty: experience definitely helps, but law school (let alone the bar or CLE) most definitely do not. Not one whit. I mean, law school is fun and interesting, but it has basically zero-to-negative bearing on real life lawyering.

A long time ago Random Walk quipped that AI would never replace lawyers because lawyers would make it illegal to do so and . . . yeah. People really don’t hate regulation enough, and professional cartels are only the tip of the iceberg.

Previously, on Random Walk

Private Credit and Insurance, two peas in a pod (reprise), and a chart dump on default rates

five charts on the rise of private credit in life insurance

Energy in 1776

It’s July 4th, so Happy Birthday America, and we’re going to keep it light and only semi-topical.

Random Walk is an idea company dedicated to the discovery of idea alpha. Find differentiated data, perspectives and people, and keep your information mix lively. A foolish consistency is the hobgoblin of small minds. Fight the Great Idea Stagnation. Join Random Walk. Follow me on twitter. Follow me on substack:

In Random Walk’s view, DOGE was (and is) absolutely a thing to root for—shedding supply-side constraints is some of the best and lowest-hanging fruit we’ve got for growth—and to the extent that DOGE did fail it reflects the treachery of its foe. The “deep state” (i.e. entrenched and sprawling bureaucracy) really is that entrenched. It’s immune to procedural change (because it feeds on process) and root n’ branch was the only chance. Plus, turn everything off at once, and see what breaks (and then turn it back on, if necessary) is a great way to unscramble the bowl of spaghetti that is federal government waste and inefficiency. I can’t find them now, but I had some banger comments to this effect on other people’s newsletters, and and I stand by every word!

I find the DOGE section unconvincing. The 2nd plots y-axis is a chart crime. I wouldn't call a reduction from ~3000 to ~2600 federal employees a "dramatic" reduction in size.

The first plot seems to flatten, but is small SNR to attribute anything to DOGE and also stabilizes at the max value? Not sure what point you want to make with the last plot.

If we take the military and transfer payments off the table, DOGE did a decent job with the rest.

I would also note that the Trump admin has done a lot in terms of cutting Medicaid, Medicare, and ACA.