Durable goods different; terminal values; a funny thing about energy costs; Japanese future; Hidden healthcare taxes

Five Idea Friday: Featuring "Hidden Healthcare Taxes," and other interesting, but important, asides

Durable Goods, ain’t what they used to be

price check on terminal values (reprise)

energy’s economies of scale

peaking into our Japanese future?

hidden healthcare taxes, rising

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.5 Idea Friday

Some quick-ish hitters for your weekend reading pleasure.

1. Durable Goods, Ain’t What They Used to Be

One big, but still under-appreciated change to the economy is that it’s much less dependent on big durable goods, like houses, than it was before.

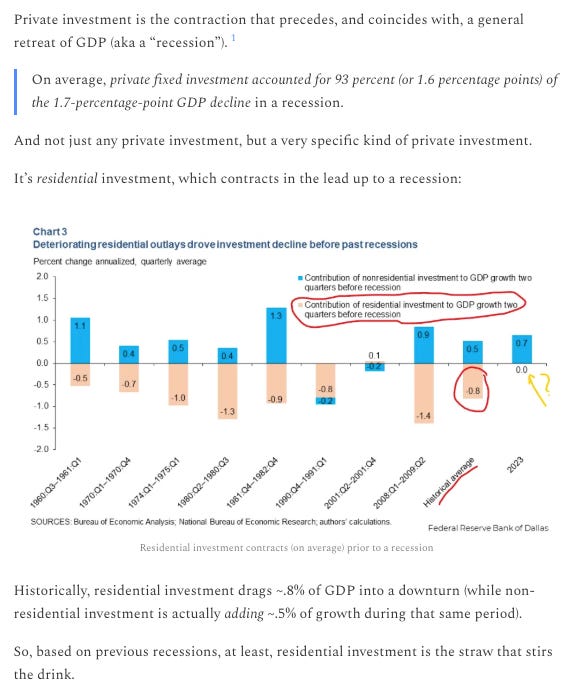

It used to be that a downturn in residential housing investment was a sure-fire predictor of recessions:

Residential investment historically drags in the lead-up to recessions, while non-residential investment actually tends to increase its relative GDP contribution.

The exception was Dotcom, a tech-driven cycle.

Well, now that everything is a tech-driven cycle, it should come as no surprise that this hasn’t been a bigger deal:

Housing’s share of GDP has been in steady decline, and has now retreated slightly below the pre-pandemic level.

An economy no-longer primed to people-growth, is also no-longer primed to homebuyer growth.

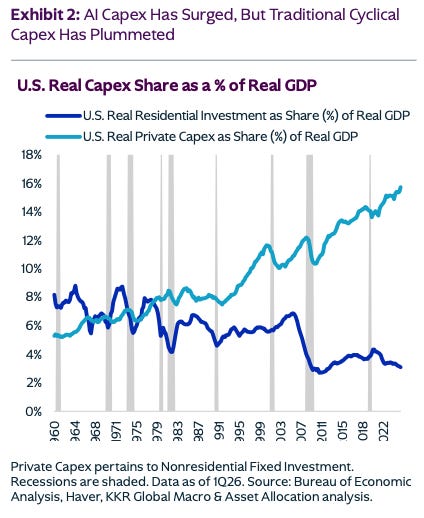

Back out the series farther, and you can see the straw that now stirs the stuff-making drink is of a different variety:

Private Capex as a % of GDP has climbed, while residential investment has really been flat-to-down for a while.

And, of course, as of this moment, it’s just any private capex, it’s one particular kind of capex that makes the world go round:

Tech-related Capex is the Captain Now.

That manufacturing boom-let? It’s definitely real (contra what some pundits would have you believe), but once again, AI is doing all the work:

Manufacturing production has surged, but it’s all AI & Data Centers, all the time.

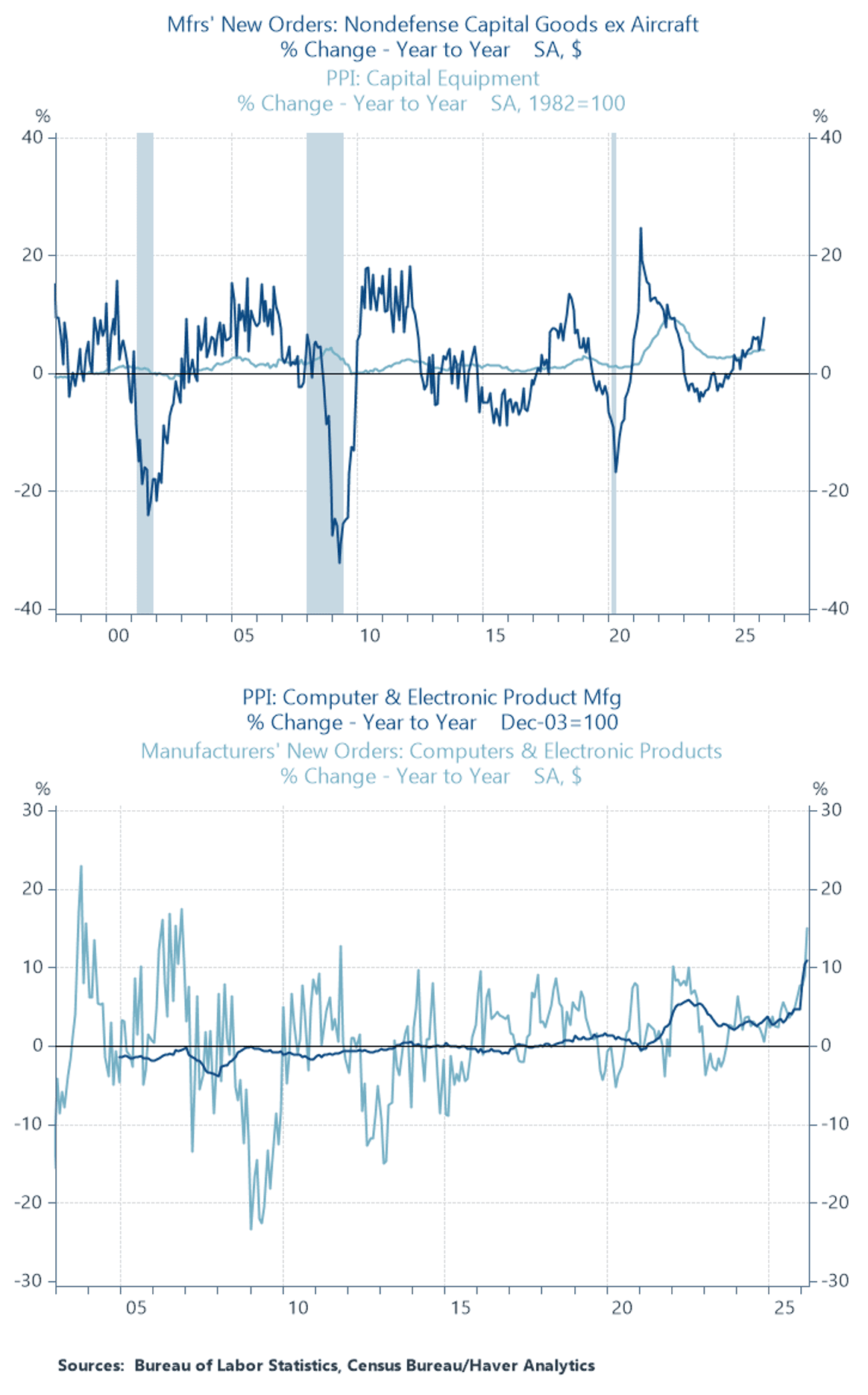

Durable goods orders, blowing out wide?

Sure. But again, it’s really just one thing:

New orders for computers & electronic products went vertical.

But, unless a hot new iphone dropped that I’m not aware of, it can mean only one thing: AI is the Capex Cycle, Now (ad infinitum).

Let’s keep it up, and hope reinforcements arrive soon.

ICYMI

2. Price Check on Terminal Value (reprise)

Earlier today, Random Walk made the following assertion about stock prices:

Bigger picture, though, if you want to be skeptical about stock prices, that’s fine, but your skepticism isn’t about present-day fundamentals. Present-day fundamentals are all screaming the same story: this train is becoming a full-bore rocketship. There is no dark fiber, and there are no empty houses rotting in the sun belt.1

Any skepticism has to be rooted in some claim about the future. The train is hurtling forward as quickly as market prices are saying it is—perhaps even more quickly. If you want to be bearish, you have to believe that something will stop (or at least slow) this train.

In other words, the current rate n’ pace of fundamentals support current valuations (and, arguably, a bit more). If you want to make an argument that prices are too high, you need to make an argument that the current rate n’ pace of fundamentals won’t last.

One can make that argument, and Random Walk has variously gestured at it in the past, but that’s not really my point. This is really just a somewhat clunky segue to a related, but different, point.

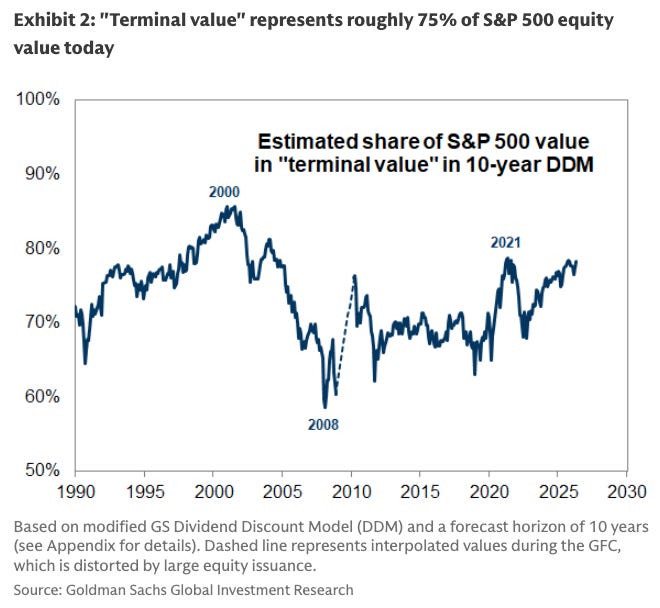

One way to think about the fraction of a company’s share price that is not priced-to-fundamentals is the perceived “terminal value.” If some part of the valuation is the net-present-value of, say, 10-years’ worth of future earnings, dividends and buybacks, then what’s left is the “terminal value” beyond that period.

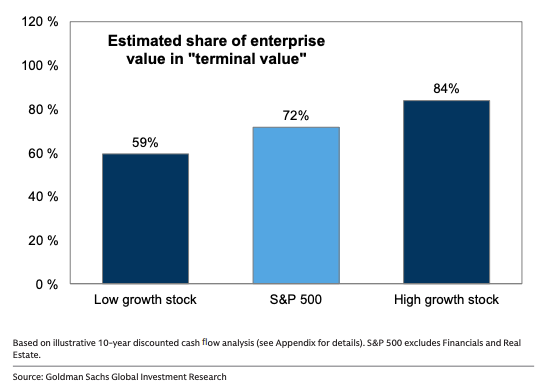

Recently, Goldman took a stab at estimating what percent of the index is attributable to that “terminal” tail. It turns out, a lot:

Terminal value comprises ~75% of the S&P’s total price.

At 75%, the terminal share is nearing the Pandemania Peak, but is still well-below Dotcom.

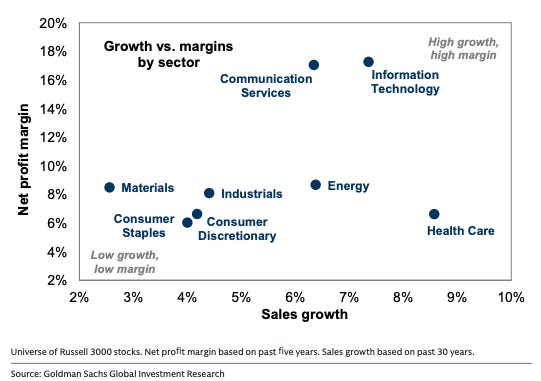

Of course, part of why the terminal share is quite so high is that the index is rife with techcos, which tend to be high-growth companies, which tend to be the sort of companies that are assigned a higher terminal value:

Tech stands alone in the “high-growth” upper-right quadrant of rapid sales and high margins, and “high growth” stocks have an ~84% terminal value share.

While it’s always a bit hazardous to extrapolate future growth-rates from present ones, one of the great investing mistakes of the last ~20 years or so was to discount that extrapolation. Tech grew bigger and faster than any sector ever had before, and the more you doubted that possibility-cum-reality, the more you missed out on the upside.

Of course, that doesn’t mean that this time will be like that last time—it could be worse or it could be better—but it does mean, once again, that whether you are bullish or bearish about current asset-values depends on whether you think techcos can keep this up (and for how long).

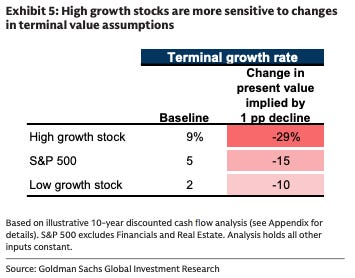

Fundamentals support the high-premium to terminal value, but if growth were to slow a bit, the discount would be substantial:

A 1pp decline in long-term growth rates would correspond to a 29% decline in high-growth share prices, in Goldman’s Terminal Value model.

Considering that the market is rife with speculation about AI’s potential negative impact on the terminal value of high growth companies, then this might give you pause. Of course, considering that the market is also rife with speculation about AI’s potential positive impact on pretty much all companies, then you might conclude terminal value isn’t high enough.

Investing is hard.

3. Economies of Scale in Energy

All things being equal, you’d think that declining demand would correspond to declining prices, but when it comes to energy, that’s not always the case.

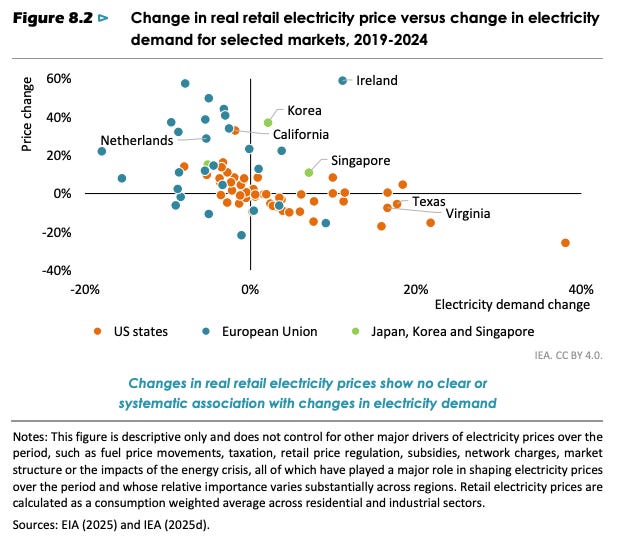

In fact, in many parts of the world, the opposite is true: more demand leads to lower prices:

Across Europe and the US, electricity prices have tended to increase with a collapse in demand (and vice versa). Ireland is a weird outlier that has more expensive energy and more demand. Too bad for Ireland, I guess.

The reason price and demand are inversely correlated is a function of grid economies of scale: more demand spreads the costs of fixed assets across a wider universe of consumption.

It’s part of why the “a solar panel in every pot” has failed as an energy policy. The grid was built for a few large sources of relatively invariable energy, which efficiently distribute distribution costs across a massive grid. Many, small and variable power sources do the opposite of that. The transmission costs alone often make the juice-not-worth-the-squeeze.

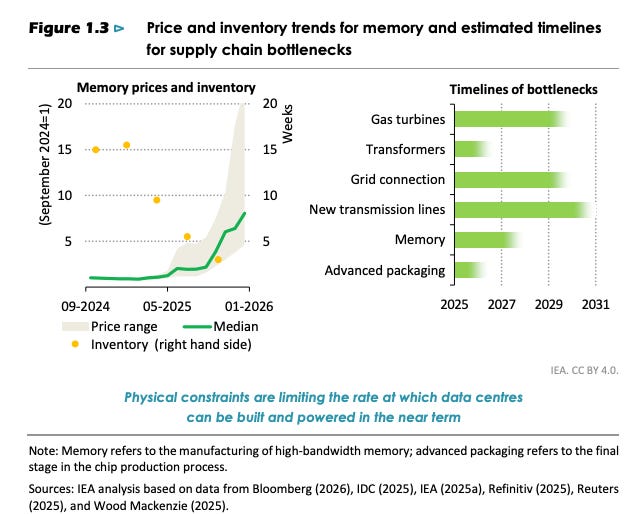

Speaking of transmission, don’t expect it anytime soon:

The bottleneck for new transmission lines has blown all the way out past 2030.

That too could put a damper on AI-related growth, I suppose, i.e. demand overwhelms supply. Of course, that would drive prices even higher and the balance is self-regulating, but it’s a thought.

4. Uncharted Waters, Previously Charted

Random Walk writes and thinks a lot about Entering Uncharted Waters, Blissfully Unaware.

The very short of it is that we’re losing a century-old demographic tailwind that’s so powerful, but also so constant, that we’ve forgotten it’s there, and we’re surely going to miss it when it’s gone.

It’s not entirely true that the waters are uncharted, though. They’re uncharted for us, but perhaps not for some other countries like China, and Japan.

At the risk of drawing spurious correlations from chart-peeping, please proceed to draw some correlations by peeping at the following charts:

Japan’s working age population:

Japan’s corporate profits as a share of GDP:

So, you’re saying that Japanese corporate profits started a relentless upward climb the moment that Japan’s working age population rolled-over?

Yes, glad you noticed, too.

And hang on, US corporate profits have more recently started a similar structural climb (and “labor’s share” of those profits a structural descent)?

That’s the gist of it.

I guess when we run out of people to hire . . . we just stop hiring, but keep finding ways to sell (maybe)? Idk. Could just be a coincidence, but it’s hard to unsee.

5. Hidden Healthcare Taxes

Last week, Random Walk wondered what non-fraud explanation could possibly explain the massive disparity in home health workers per senior in New York, but also CA, DC, and MN.

So far, I’m yet to come across anything that isn’t “well, it may not be deliberate fraud, so much as those states made it really easy to commit fraud, and pretended not to notice.”

Fine. Judge that however you see fit.

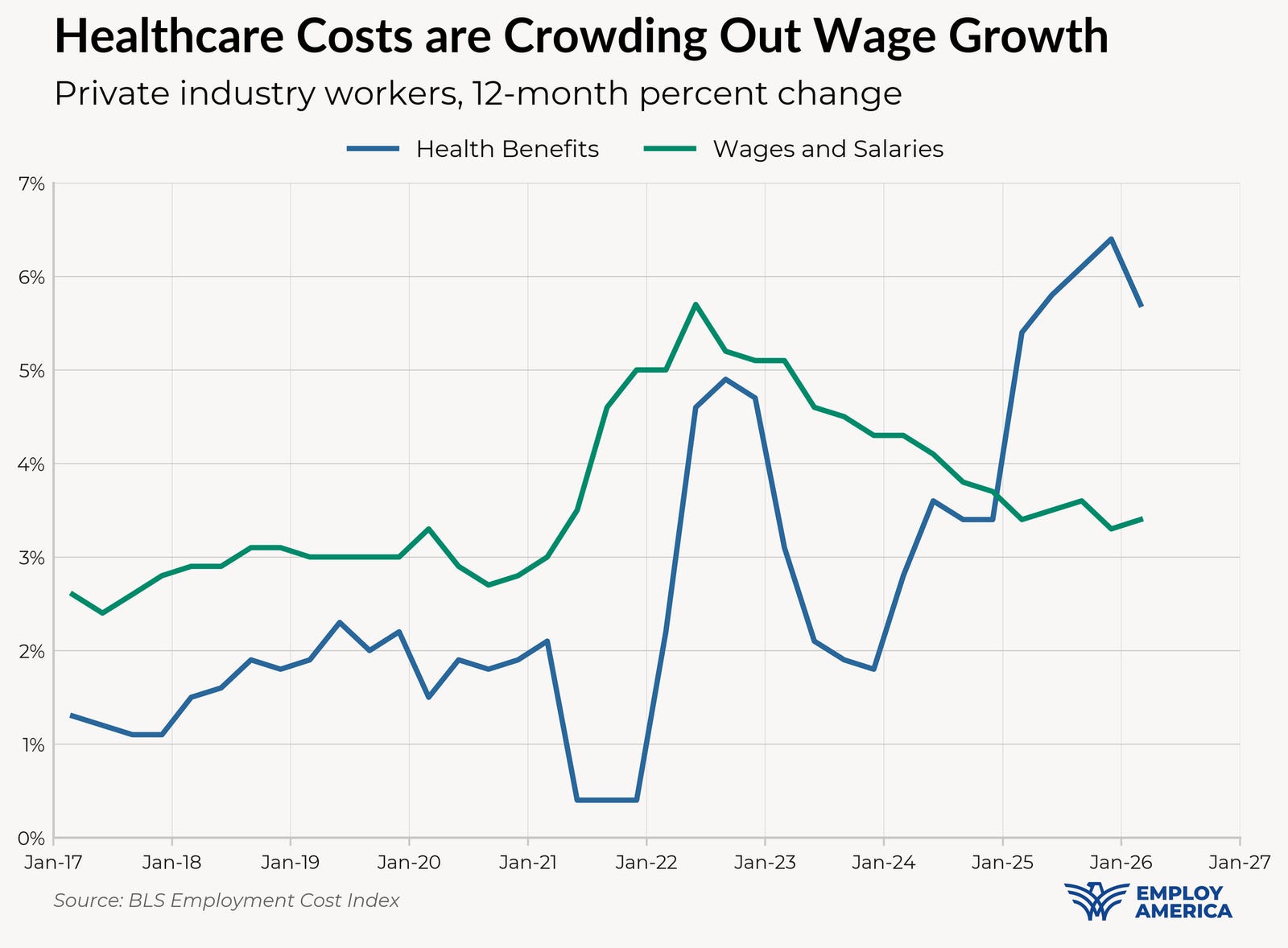

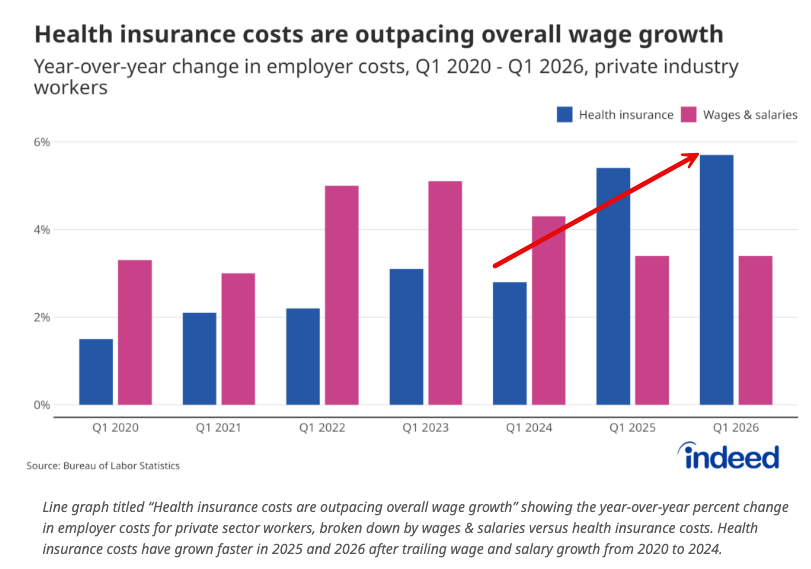

This week, I would suggest that perhaps there are some very tangible consequences of that fraud-not-fraud. And it’s actually something Random Walk has observed many times before: ‘Someone else pay for my healthcare’ is probably the worst idea ever.

Once again, the cost of healthcare is rising, and while people are paying for it, they probably have no idea because the bill is handled by their employer:

The employer-cost of healthcare is growing much more quickly than wages.

What that means is that healthcare costs are “crowding out” wage growth, and the impact is regressive, in that it doesn’t scale with incomes—the less money you make, the higher the “healthcare tax” is, as a percent of your income.

OK, but what does that have to do with home healthcare aids in New York?

I’m so glad you asked.

Well, part of why employer-based healthcare costs are rising is because of the terminally higher cost of services. Another part of why they’re “rising,” is that the Obamacare subsidies have expired, which is to say that costs aren’t rising, but now the bill is somewhat less-attenuated.

Yet another reason costs are rising, and this is the one that matters for today, is cross-subsidies.

You see, our “free” national healthcare system doesn’t fully reimburse providers for what they charge. Hospital systems et al eat some of the shortfall (which can be quite large), but the rest they foist on the private market insurers . . . who then pass those costs on to employees (unbeknownst to them) via higher employer-paid premiums, as per above.

In other words, when public health consumption increases, taxes go up to pay for it, but we don’t call them “taxes,” we call them “[some fraction of] employer sponsored health insurance premiums.”

That being the case, if, for example, you were a state with a high influx of illegal immigrants, and you wanted to create “jobs” and “growth,” by making it easy for them to get access to public healthcare . . . then you could do that, and at least some large portion of the bill would get redirected to “private” market employees. And not only would they likely not even notice—hooray for you, elected officials—those private citizens would probably blame the insurance companies for your largesse.

It’s the perfect crime.

Is that definitely what’s going on? Idk. It’s a theory though, and my guess is that it’s got legs.

Previously, on Random Walk

Private Credit and Insurance, two peas in a pod (reprise), and a chart dump on default rates

five charts on the rise of private credit in life insurance

Energy in 1776

It’s July 4th, so Happy Birthday America, and we’re going to keep it light and only semi-topical.

Random Walk is an idea company dedicated to the discovery of idea alpha. Find differentiated data, perspectives and people, and keep your information mix lively. A foolish consistency is the hobgoblin of small minds. Fight the Great Idea Stagnation. Join Random Walk. Follow me on twitter. Follow me on substack:

"Is that definitely what’s going on?"

Yes. Also the state making that choice isn't even paying the government portion, it's foisting it on the feds.

I predict the Sunbelt will cave and expand Medicaid eventually. Ideology can't compete with all those free fed bucks forever.