Uncharted waters (reprise); Almighty Consumer check; Healthcare[-fraud] GDP?; AI-Lawyering for Me; Longs, but not shorts

Five Idea Friday: Musing again on growth without growing, and other tidings, good and bad

Uncharted waters, still unawares

almighty consumer, running on gas and ecomm

healthcare[-fraud] domestic product?

AI lawyering for me, but not for thee

the long, but not shorts, of rates (or just a weird thing that perhaps means nothing at all)

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.5 Idea Friday

Some quick-ish hitters for your weekend reading pleasure.

1. Uncharted Waters, Still Unawares

Just briefly revisiting Uncharted Waters, Blissfully Unawares.

First, a nice illustration of just how unusual it is to have such a yawning gap between GDP growth and employment growth:

GDP and employment growth tend to run together, except (1) now; and (2) in the lead-up to the Dotcom Bubble.

Interestingly, the Dotcom bubble was followed by a “jobless recovery,” until a rate-driven real estate cycle kicked-in, which helped drive employment up (for a bit). Draw your own conclusions.

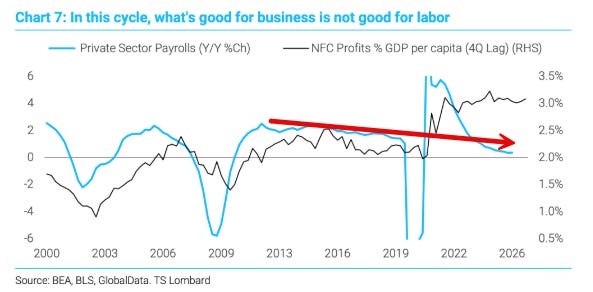

Here too, is another look at current weirdness of “growth without growing:”

Private sector payrolls showing steadily declining growth, accompanied by a huge jump in profits.

It’s a very odd thing, and without the AI Capex boom, it’s really hard to imagine where the economy would sit right now. All that cash would have to go somewhere, perhaps in the form of even more buybacks, but man alive, all chips are on . . . chips.

Second, while I stand by the descriptor “blissfully unawares,” Nick Eberstadt of AEI published a 63 page paper Can a Depopulating America Still Flourish? and I thought perhaps “unawares,” was not entirely fair.

I did, however, settle-in to read the whole thing, and while it’s not bad, per se, it’s mostly . . . besides the point?

Read it yourself, but the gist of it is:

we defeated Malthusian predictions before because see, e.g. the extraordinary productivity gains of industrial farming, in which fewer people produced much more food;

the problem though is that too many people are out of the workforce, we’re too old, we spend too much on healthcare, and the deficit is unsustainable.

I mean, sure, but . . . that still doesn’t answer the question of whether or how we grow without growing?

At the outset, it’s very odd to begin with a heart-warming resolution to a Malthusian doomscape for an inverse-Malthusian problem. Yes, we have lots of precedent of producing more with less . . . which precipitated a massive population boom, which led to massive growth. What we’re now wondering is if we can produce ‘more with less’ to keep economic growth humming along without a population boom.1

Eberstadt doesn’t even address the core relationship between people-growth and economic growth, in any meaningful way.2 Nor does he look at any of the attributes of the current cycle, e.g. supercore inflation, tech-driven earnings, healthcare’s share of the labor market, etc. It’s mostly just, “well, not to worry, we’ll be able to create enough stuff to feed and supply everyone, but mind the deficit” and it’s like, “thanks, dude, no one was really worried about that, but glad to hear it.”

Idk. Maybe I’m being unfair, but “blissfully unawares,” remains apt and correct, imo.

ICYMI

2. Almighty Consumer Doing Gas and E-Comm

On the Almighty Consumer, it’s been a gas and ecomm story of late:

Transit, Gas, and e-comm (and I suppose lodging), are the only categories comfortably in the green.

Higher gas prices are clearly effecting other categories of consumption.

Unsurprisingly, discounters have been having a run, lately, as well:

Average transaction values at discount stores has been growing at a healthy clip since the middle of 2025.

The implication is (perhaps) that people are doing more of their shopping at the discounters.

In general, on an inflation-adjusted basis, there’s been something of a slowdown:

Real retail and food-services sales are flat-to-down since October.

Income growth has lagged inflation for a bit longer than is comfortable, as well:

Real wage growth has been negative for ~half a year, although I suspect the gap has closed somewhat recently (especially, accounting for fuel costs).

Anyways, it’s not a great look, and I’m not really sure what to make of it all, but things have held up, and a temporary energy shock isn’t the worst thing in the world. Plus, there’s been recent evidence of an uptick in hiring and wage growth, so some of this might be a bit lagged.

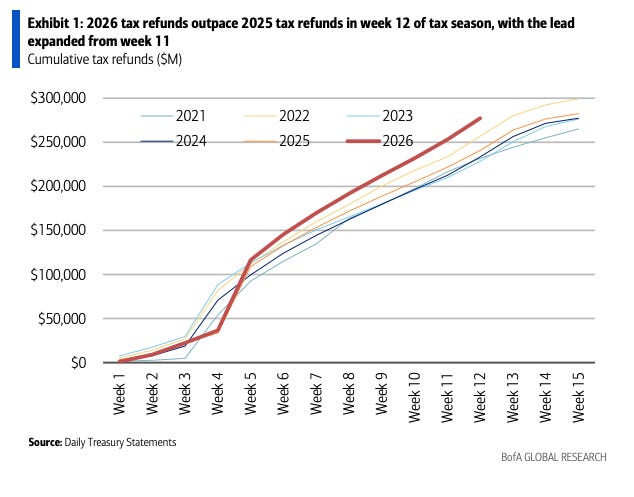

Probably tax refunds have helped somewhat:

Tax refunds are running ahead of years prior, and other stimulants may be helping the Almighty Consumer along.

But, bigger picture, as long as everyone stays employed (and they have), I don’t worry too much about the Almighty Consumer.

3. Healthcare[-Fraud] Domestic Product?

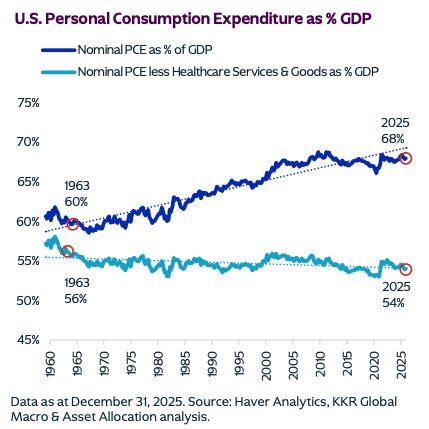

While on the subject of consumption, and particularly the growing importance of healthcare to consumption (and thereby, job-growth), this too was a striking chart:

Non-healthcare consumption as a % of GDP is actually lower than it was in the 1960s, and it’s been getting steadily lower (with the exception of Pandemania and Dotcom).

Put another way, without healthcare, we’ve been doing less and less personal consuming (as a share of GDP) for almost 70 years!

That’s pretty wild. It’s not an understatement to say we’ve been taking our wealth and plowing it straight into healthcare, and we’ve been doing it for an awfully long time. And, of course, given how unsustainable all that debt-financed spending actually is, it presents quite the pickle.

Random Walk has written at-length—and well-before it cycled into the mainstream—about how Healthcare Makes All the Jobs. Home health aids, specifically, have been the “private sector” jobs engine, especially in places like New York (but really everywhere). It’s part of what I’ve called the Rotation to the National Nursing Home and/or Healthcare Domestic Product.

That dynamic has helped disguise some underlying structural weakness in the economy because (a) healthcare isn’t really “growth” (let alone a pro-cycle);3 and (b) we’re paying for it with borrowed money that we can’t afford.

Even Random Walk, however, may have under-estimated the extent to which the home health hiring bonanza was disguising structural weaknesses.

I mean, how does one explain this chart with reasons that don’t sound in “fraud”:

New York has ~3X the number of Home Health Aids per senior than the US average (which includes New York)!

I’m taking the math at face-value, but assuming it’s right (and I haven’t seen anything to suggest otherwise), what innocent explanation could there possibly be for such an incredible discrepancy?

I mean, yes, New York made it dramatically easier to sign-up for “Consumer Directed Personal Assistance,” (i.e. relatives getting paid to provide elder care), which perhaps makes fraud extremely easy, but opening-up a self-checkout grocery store and pretending not to notice that the shelves are bare and the till is empty, isn’t really an excuse.

This is just staggering:

New York spends 85% more per resident in Medicaid than the national average.

And for an already-cash-strapped state (and city), the economic picture would have been even grimmer without letting healthcare go brrrr:

New York’s Medicaid spending per resident is already the highest in the country at $4,942 as of 2024, nearly $1,000 more than the next highest state. We estimate that if New York’s per resident Medicaid spending was the same as the U.S. average, they would have spent nearly $43 billion less in 2024. While it is a state program, it is a matter of federal concern as the federal government bears 57 percent of the cost.

New York unleashed a ~$43B stimulus in 2024 alone by lavishly spending taxpayer money on healthcare.

I know it’s partisan-coded, but it doesn’t make it any less-true: chase-out your productive, tax-paying residents and cover the shortfall with federally-funded medicaid fraud just isn’t a sustainable model.4

4. AI Lawyers for me, but not for thee

On the subject of AI-lawyering, this too, was hilarious.

AI-drafted pleadings have apparently exploded in recent years:

The share of filed complaints with “detected AI text,” is approaching 20% (and looks to be doubling every year).

Lawyers are very concerned about non-lawyers using AI for the “unauthorized practice of law,” but there is very little hesitation about super-charging their own outputs with LLMs.

Truthfully, this is probably a good thing. Well, not this specifically, because this finding is focused on complaints, and the last thing we need is to lower the cost of filing complaints below what it already is.

But let’s assume that this is true of the broader universe of pleadings (because I suspect that it is). In that case, my actual view is that AI isn’t going to displace lawyers (with or without regs), but it will increase their throughput (and perhaps automate and/or simplify some of the less-fun stuff). If AI is drafting a lot of the boilerplate recitations that lawyers require (by their own conventions) then there’s an element on ongoing absurdity, but at least it’s less strenuous and expensive.

This, however, is a less-promising (but unsurprising) development on the AI-generated text front:

“AI-Assisted” text on the internet is (supposedly) going parabolic.

So, it’s not exactly Slop-to-Table output, but it’s Slop-to-Table with a human-in-the-loop.

Let’s hope this is all some collection of necessary-but-boring text summarization that wasn’t all that high value in the first place, but I’m ever-reminded of this quip:

Obviously a lot has changed since March ‘22, but “the more summaries you consume in your life the stupider you become,” still rings true.

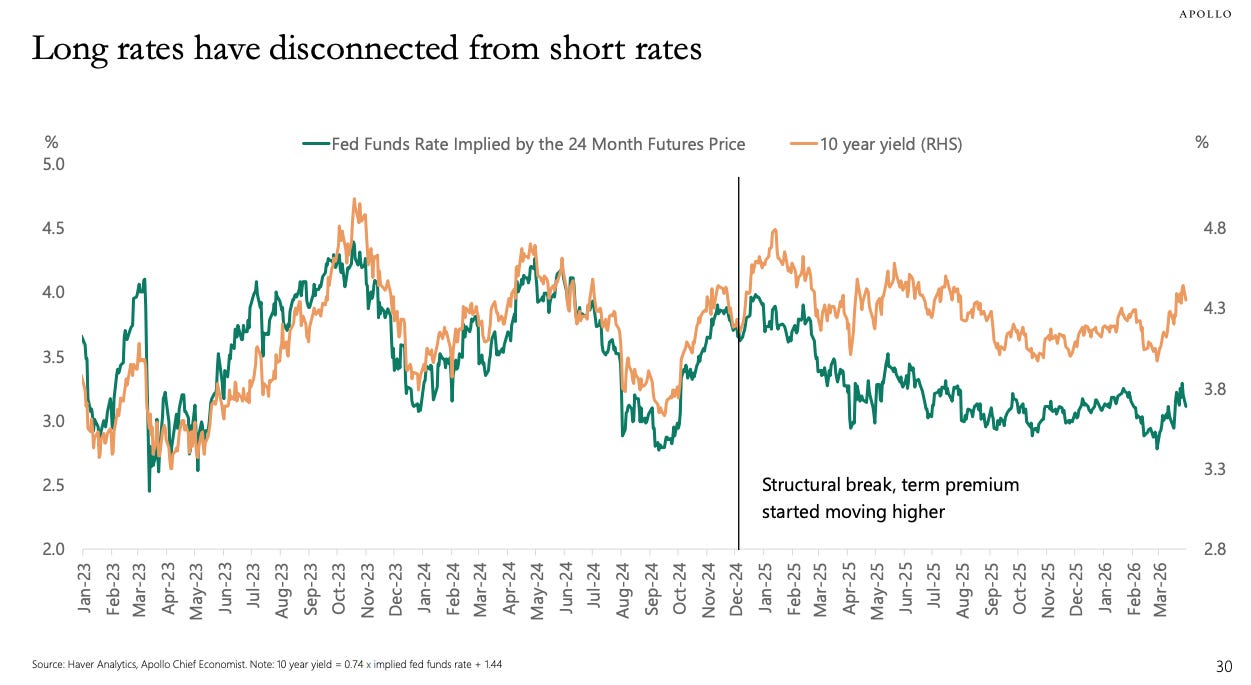

5. Long but not short

And, to wrap this up, an observation that probably means something, but what, I can’t really say.

Long-term interest rates have separated from short-term rates:

Short-term and long-term rates are still moving together, but they’re just dancing farther apart . . . and it all seemed to start with Trump’s election, or thereabouts.

I’m not really sure how to interpret this. Really, feel free to let me know what you think, because I’ve got only bad guesses.

I’ve long wondered whether higher long-term rates are just a thing, and the Fed can’t do anything about it (because long-term rates are driven by supply-and-demand, and the marginal buyer of US debt is looking at the deficit and demanding yield). In other words, the Fed can lower short-term rates, but long-term rates are whatever the market demands.

Idk if that’s what’s happening, or why it should specifically have started in Dec. ‘24 . . . maybe the market just decided that Trump was going to run the deficit structurally higher for ever? Again, idk. I just thought it was an odd thing.

Previously, on Random Walk

Private Credit and Insurance, two peas in a pod (reprise), and a chart dump on default rates

five charts on the rise of private credit in life insurance

Energy in 1776

It’s July 4th, so Happy Birthday America, and we’re going to keep it light and only semi-topical.

Random Walk is an idea company dedicated to the discovery of idea alpha. Find differentiated data, perspectives and people, and keep your information mix lively. A foolish consistency is the hobgoblin of small minds. Fight the Great Idea Stagnation. Join Random Walk. Follow me on twitter. Follow me on substack:

There’s a deeper, unconsidered observation in that the industrial revolution was a productivity leap-forward that unlocked massive population growth, whereas our more recent productivity-leaps have mostly done the opposite. Something about Maslowe’s Hierarchy there, I’m sure.

As an aside (to an aside), I found this result on AI productivity and hiring to be somewhat surprising:

Mining is a standout for AI adoption (with above-trend productivity), but has done little in the way of extra hiring (in fact, hiring is below-trend). Mostly, the point of the research is to show no-correlation between AI Adoption and Hiring (for better or for worse) because AI is a Job Maker, Not a Job Taker, but if you want to be gloomy, well the miners are going to be SOL.

Certainly it can be—extending the useful lives of productive workers is growthy—but that’s not what we’re doing, in the main. We’re doing elder care, which may well be an important and ethical thing to do, but it’s still not growth.

It’s also yet another reminder that the next time Liz Warren or one of her henchmen in the the FTC, PCAOB, SEC, DOJ, etc. put on a big show about how Wall St. Fat Cats make it hard to cancel their Amazon Prime Subscriptions or make a web browser that’s too free for everyone, or worry that credit is both predatory and exclusionary at the same time, and ‘oh the horror,’ you should feel revulsion and contempt.

Home health aids can generate coding.

Also a request: charts on the shadow economy please!