Oil Shock or Nah (and the Machinations of Iran's Biggest Customer)

Riffing on the oil shock that isn't (yet), and a 'Beggar thy Neighbor' reprise

oil shock or nah?

hard to bet against the invisible hand

China’s “assist”

the ‘beggar thy neighbor’ trade, reprise

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.Oil Shock or Nah?

Even more bullishness abounds, as on-again, off-again “progress” vis-a-vis the Strait hijackers switches back to “on.”1

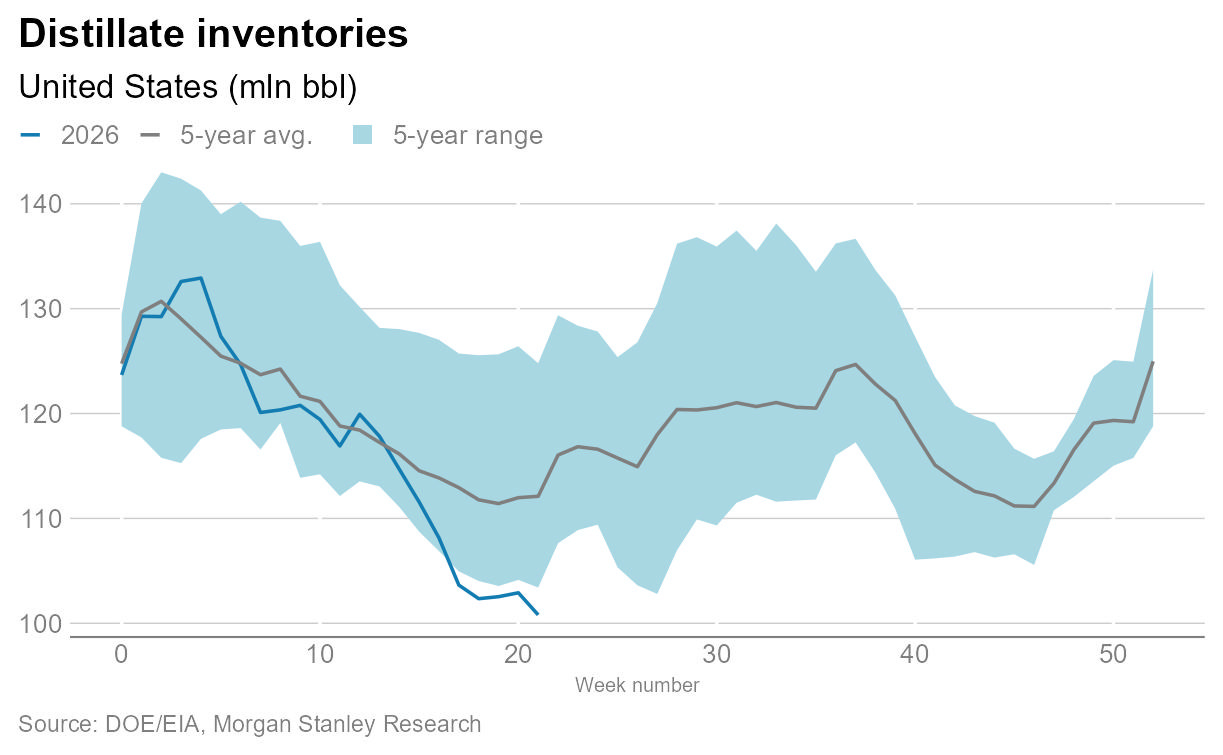

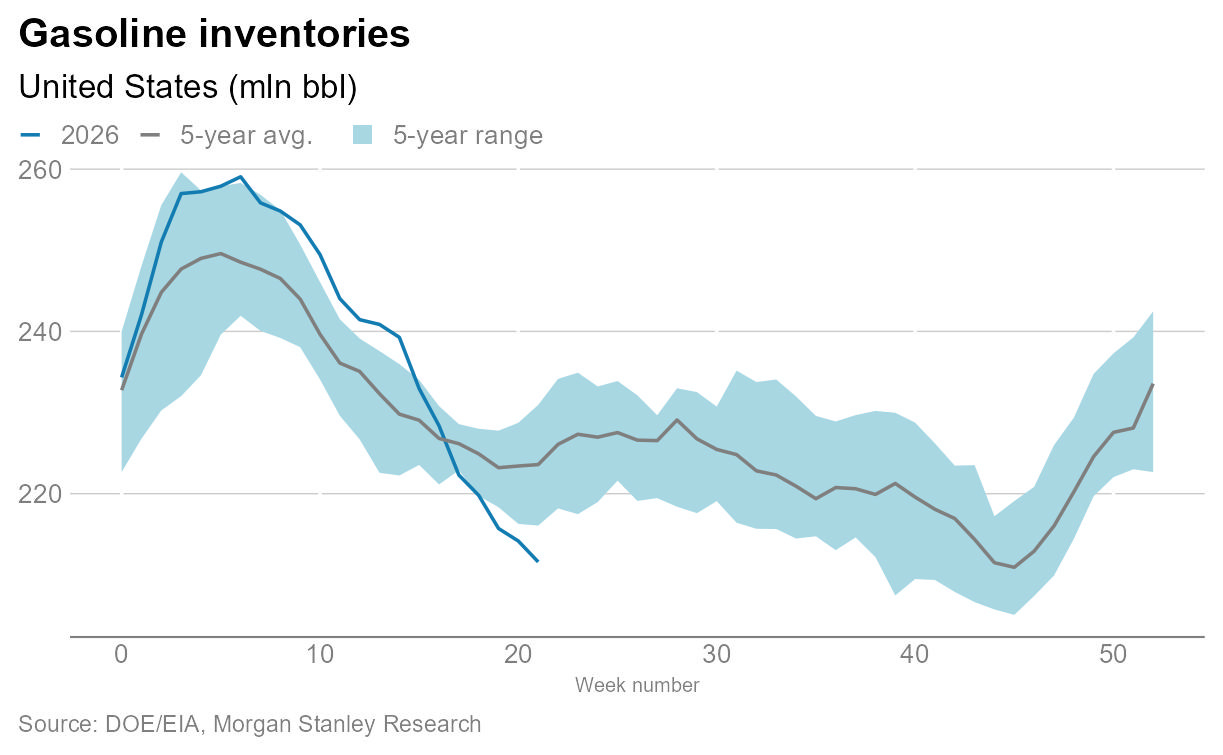

It is pretty remarkable how bullish everything has been despite the clear deterioration in supply of a (supposedly) non-substitutable global commodity:

Supply buffers are what they are, but it does seem reasonable to suppose that there’s an outer limit to how much of a supply-side disruption the world can actually withstand without some real pain.

It’s bothered investors somewhat for sure, but not nearly as much as perhaps it should.

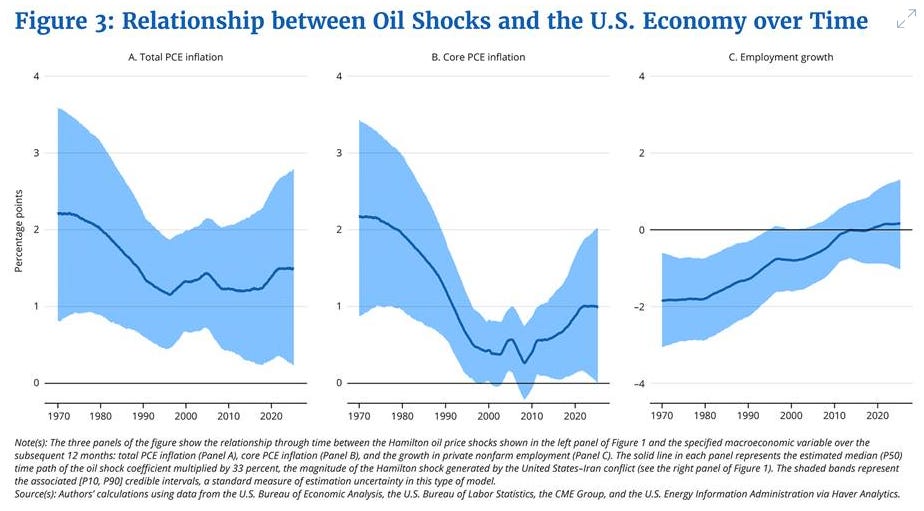

I mean, oil shocks definitely don’t matter as much as they used to . . . but they still matter:

In a less “oil intensive” economy, oil shocks just don’t hit as hard—there’s some inflation, yes, but employment effects are . . . positive?

Still, the world does need oil, and if supplies are shrinking every day, then do we run out? That seems bad, right? Unlike dollars, “you can’t borrow oil out of the ground,” as the saying goes.

On the other hand—and the reason for all the hedgy language—is that it’s also a massive mistake to bet too hard against the ingenuity and resourcefulness of the invisible hand, especially as it pertains to a global commodity. The picture looks insurmountably grim, but just because you and I can’t see a path, doesn’t mean there is no path(s). Random Walk has learned this the hard way before.

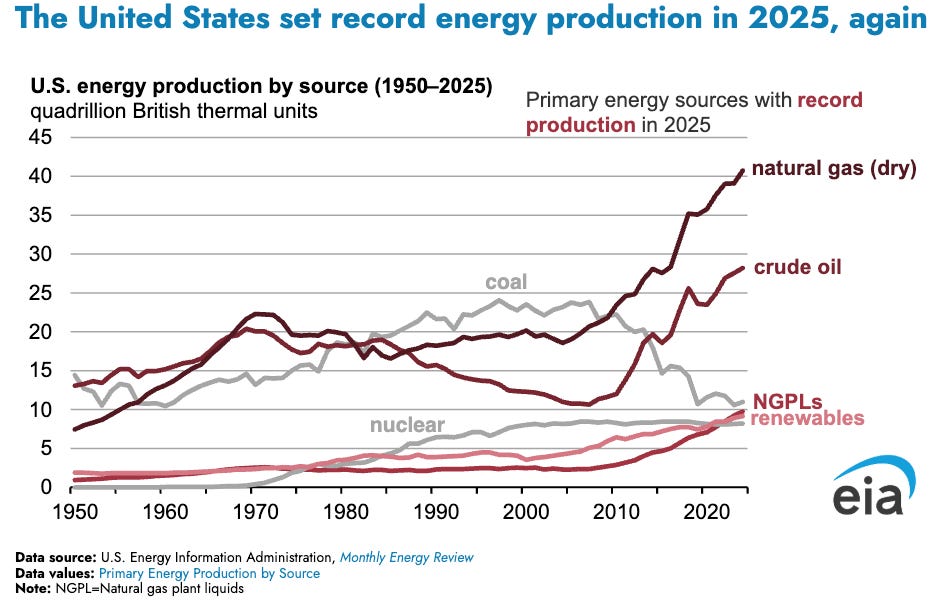

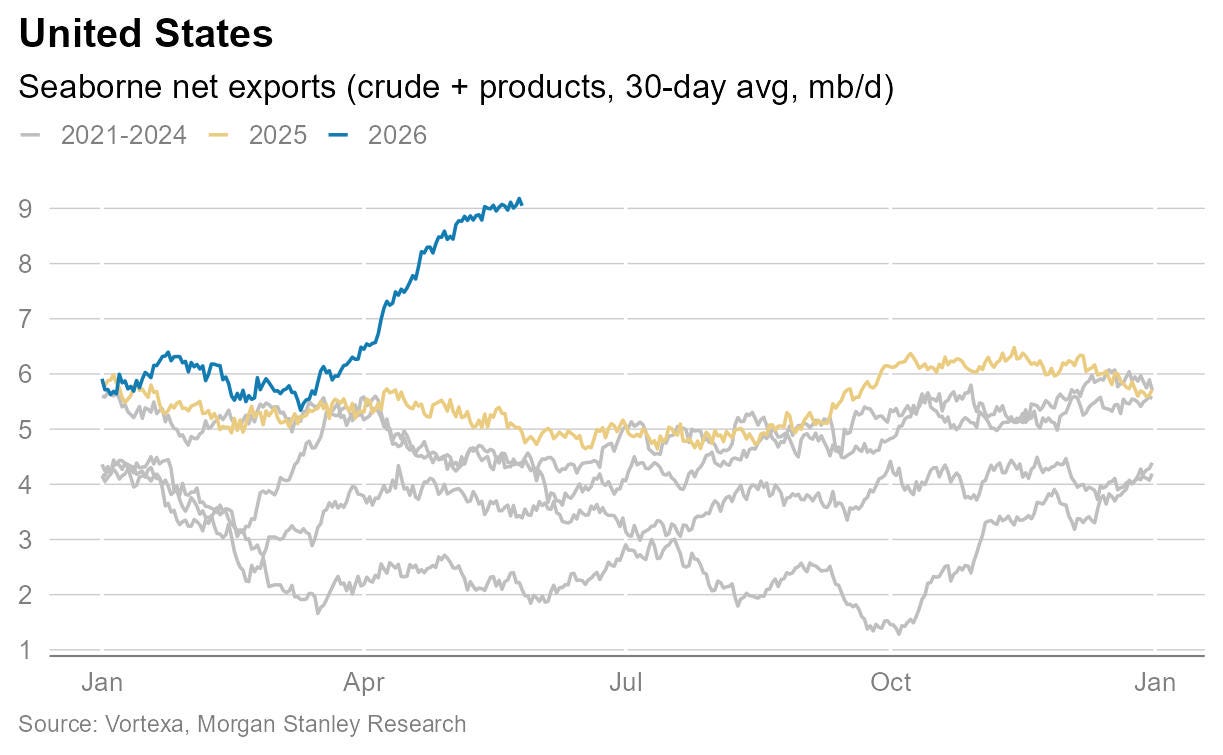

For one thing, less energy over there, means more energy here (which then gets sent over there):

2025 was (another) record-breaking year in energy production . . . 2026 will surely reflect yet another upward inflection. The US continues to grow its role as a net-exporter of energy.

What’s that? Can’t ship oil through Hormuz?

No problem—build some more pipelines, and in the meantime, load up the jumbo jets:

Seaborne net exports of oil, etc. are ~50% higher than they were last year.

The point being that when the going gets tough, the tough do, in fact, get going. And that’s all the more true when there’s lots of money to be made, which there certainly is.

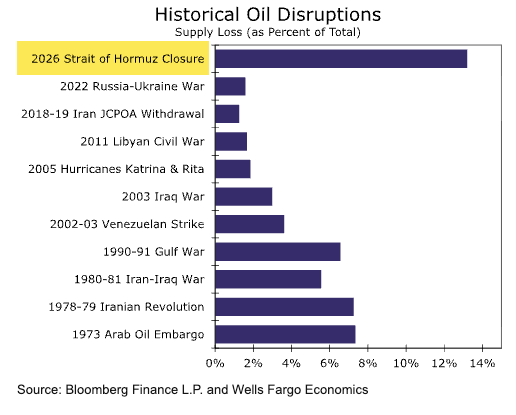

Still, impressive adaptability notwithstanding, it’s hard to escape the lurking fear that (a per above) there must be some limits to what can be done and in how much time:

A 14% supply-loss (and counting) is an all-timer for oil disruptions, and eventually storage has to hit the bottom of the literal barrel . . . right?

It’s all a bit strange. For all the apparent data pointing to an incoming shortage, oil prices (forget stock prices) seem pretty complacent. I mean, they’ve surely gotten higher, but not that high in the big scheme of things:

WTI is ~$95/barrel . . . basically the same price as it was for the first-half of the last decade, until the shale boom kicked-in.

Now, there’s of course elasticity in demand, which means at a certain price, people just stop buying oil, and so maybe that’s keeping prices in check. But I do wonder if the physical reality is just a bit more optimistic than what the data seems to show.

Anyways, puzzlement aside, oil prices weren’t really the point. The point was just a brief look at Iran’s biggest customer: China. More specifically, China’s Global Emporium to Sell Everything to Everyone (aka the “Beggar Thy Neighbor Trade”).

ICYMI

![Uncharted waters (reprise); Almighty Consumer check; Healthcare[-fraud] GDP?; AI-Lawyering for Me; Longs, but not shorts](https://substackcdn.com/image/fetch/$s_!MpiH!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F00da6c53-cccf-43f3-b00b-ba932898ae46_429x429.png)

China and the ‘Beggar Thy Neighbor’ Trade (reprise)

One quick thing on oil, but specifically as it pertains to China.