Capital Intensity🤝Capital Light

What if everyone wins?

delayed onset regime change

the change is coming from inside the tech

software, not dead yet?

discount shopping on aisle hyperscaler (maybe)

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.Capital Intensity🤝Capital Light

Continuing on the theme of regime change, but shifting gears.

The rotation to tech continues to embigger, but within tech, the laggards have become the leaders. Low-capital software—the darling of the old regime—has given way to high-capital hardware.

The rotation from capital light to capital intensive is something Random Walk has written about before, but here’s a few more charts on that theme, plus a little wrinkle.

Delayed onset regime change

First, one “table-setting” observation on the current cycle.

While the inflection points for new market regimes historically tend to be recessions (reflecting the collapse of the prior regime), in this case the “regime change,” catalyst wasn’t the pandemic or the pandemic “recession,”—it was AI.1

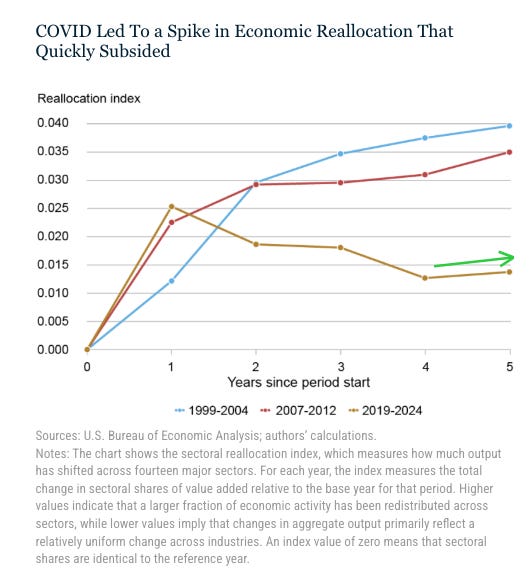

Not that that’s very controversial (even if the pandemic was a bit oversold as a behavioral shift at the time), but the NY Fed researchers have a neat visualization to that effect:

If you aggregate the total post-recession change in sectoral contribution to output (i.e. the extent to which different sectors contribute more or less to output relative to pre-recession), then the “economic reallocation” post-pandemic was both less substantial, and less-enduring that the previous post-recession recoveries.

After Dotcom, the economy became asset-heavy and financials-oriented (i.e. financing the labor-intensive housing boom).

After the GFC, the economy became semis- and then software-oriented—the iphone, apps, cloud and saas booms.

After the covid-recession, the economy didn’t actually change all that much . . . until year 4 (2023), when rates went up, and the AI Capex surge began shortly thereafter.

And boy did the Capex rotation change some things.

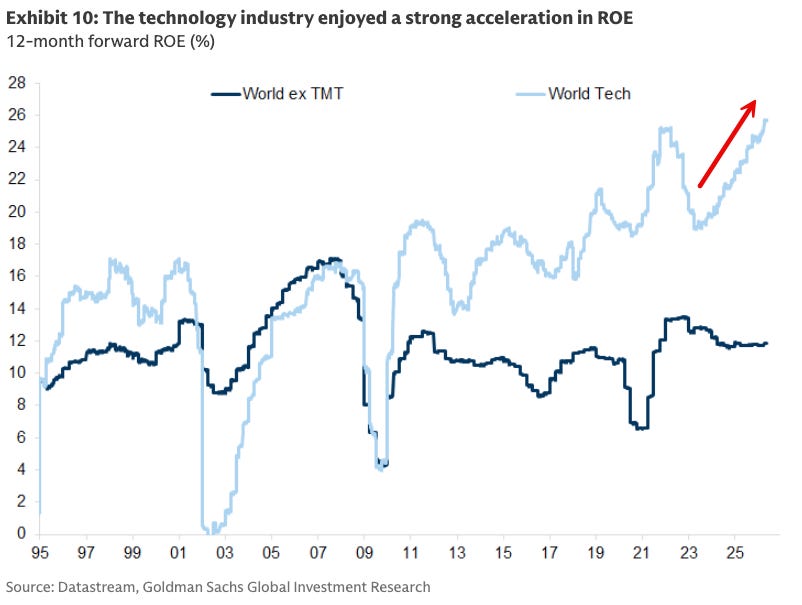

At the sector level, you might say “nothing has changed,” because tech itself is still running away from the field:

Fwd ROE for tech has continued to accelerate, while the world-ex-tech is basically stagnant.

Notice, however, the ZIRP-peak in ‘21, followed by the rate-hike valley in ‘22, followed by the ‘23-present reacceleration. Something definitely changed, but the change is coming from inside the Tech.