K-Shape *Poof*

Banks report, lower-income households on a tear, and (maybe) the Wealth Effect is realish

banks can confirm the Almighty Consumer is A-OK

K-Shape, we hardly knew ye’ — lower income households are on a tear

spending more than wages, but how?

coda, ‘housing isn’t the cycle, anymore’

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.K-Shape Goes Poof

The notion of a “k-shaped” economy just won’t quit the zeitgeist.

Whenever there’s the barest inkling of a k-shape, everyone seems very eager to opine on however which ways the middle- and lower-classes are falling behind the wealthy.

It’s hard to otherwise explain why the K-Shape is such a recurring theme, other than the obvious slopulist appeal. Random Walk has touched on this before, but the K-Shape is structurally implausible—the shape of the labor market and other cyclical factors favor the bottom, relatively. But, also, the data doesn’t support the K-Shape, either.

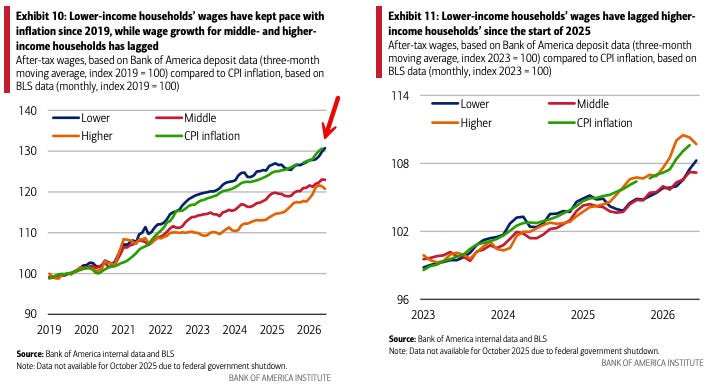

Did you know that lower-income households are the only post-pandemic real income winners? Well, it’s true (although other data sets vary a bit):

“Yay, the lower and middle classes are doing pretty great!” is apparently a dog that will not hunt [headlines].

Anyways, it’s bank reporting week, so it’s a good occasion to remember that the Almighty Consumer is A-OK, there is no K-Shape, and while there is at least one curiosity, there may be a contra-Random Walk explanation.

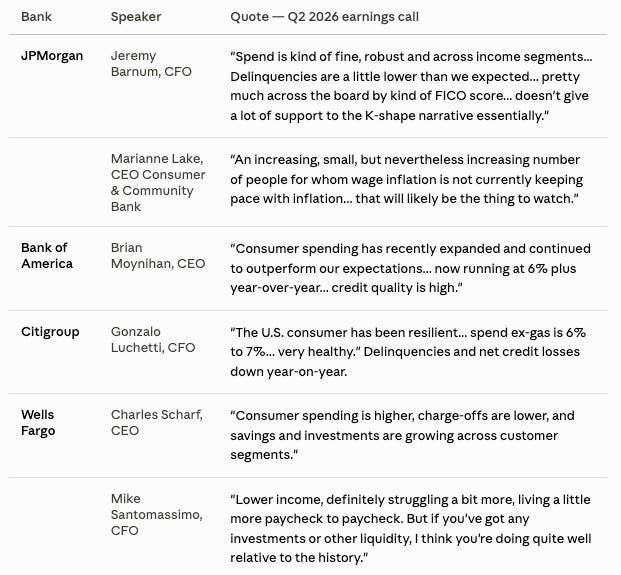

First, from the banks:

Everyone paints a pretty rosy picture of the Almighty Consumer. Only Wells Fargo hints at anything K-shaped, but (as per below), I strongly suspect that’s an artifact of higher gas prices.

In general, the banks are doing pretty well. Credit has grown, they’re making a ton on trading fees, an un-inversion has been good for the biz.

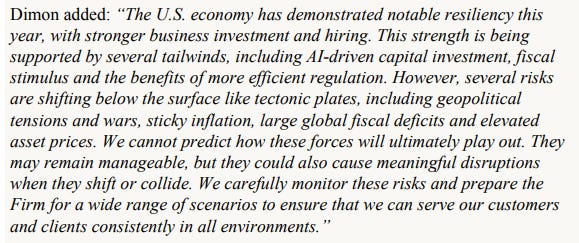

Also, I love a good bedtime story from the most consequential man in global finance, Papa Jamie Dimon:

“It’s great, but it could be terrible, any moment.”

Thank you, JD, for those illuminating comments.

ICYMI

Started from the bottom (reprise)

As for the data itself, well, whatever K we might have had, has become an E, which itself has become just a squished line.

It starts with hiring and wage growth.

Payrolls, looking pretty good: