Marks are [High][Low][Just Right]

5 Idea Friday: Public marks, private marks, credit marks--all the marks

A valuation edition of 5 Idea Friday

sticky car prices

public markets: anything but bubbly

for pe, the song remains the same . . . selection effects drive the rest

vc is doing fine where it matters (sort of)

private credit narrative v. fundies

👉👉👉Reminder to sign up for the Weekly Recap only, if daily emails is too much. Find me on twitter, for more fun. 👋👋👋Random Walk has been piloting some other initiatives and now would like to hear from broader universe of you:

(1) 🛎️ Schedule a time to chat with me. I want to know what would be valuable to you.

(2) 💡 Find out more about Random Walk Idea Dinners. High-Signal Serendipity.1. Car prices are remarkably sticky

Random Walk has made this observation before, but when it comes to asset prices, there is perhaps no pithier example of how looks can deceive.

If you can believe it, the price of a new car rocketed up during the zero-interest rate period, and then just hit a plateau:

The average price of a new car has been remarkably stable at just under $50K.

Pretty wild how low interest rates can make the price go up, but high interest rates do not make the price go down, right? And all of that while disposable income ebbs and flows, and gas prices go up and down, and auto sales themselves have been pretty soft. It’s almost like the price is impervious to supply, demand, and most importantly, the customer’s ability to pay.

Well, it’s less wild when you appreciate that that’s not what happened, at all. Of course auto prices went down.

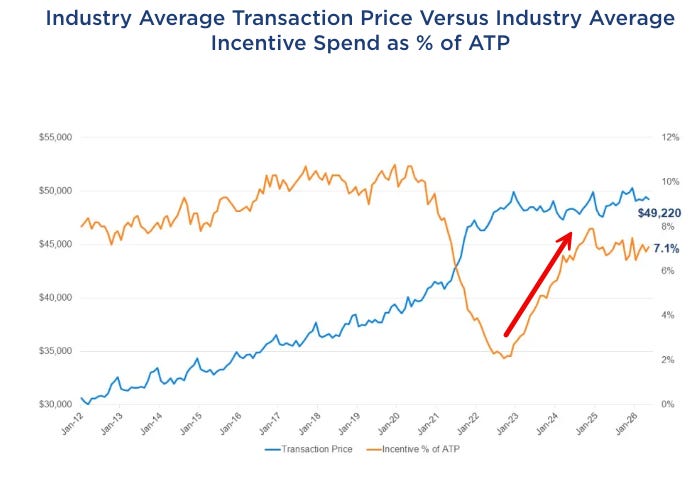

Cars are heavily financed assets, like houses and private equity, and when rates went up, prices most definitely tumbled . . . even if the auto dealers don’t want you to know:

The headline price stayed flat because rising discounts soaked up all the depreciation.

Autodealers surely know the psychology of auto-buyers better than Random Walk, so I’m sure they have very good reasons for staying anchored on a high watermark of headline prices. Maybe it has something to do with dealer financing lines, as well, I don’t really know.

Mostly, it’s just a brief intro into today’s theme: how are the asset prices, really? Is the price signal telling you what you need to know, or does something else lie beneath the surface?

ICYMI

2. Public markets are anything but bubbly

Say what you will about the state of the stock market, but there’s very little evidence of a “bubble,” at least not in the traditional sense.

Earnings led

If anything, the stock market has become substantially more cautious—multiples have contracted, and performance has been entirely profit-driven:

In comparison to the Dotcom boom/bust, when multiple-expansion accounted for 73% of the returns, it’s EPS doing all the work (especially for tech). And again, the prices paid for those earnings have declined pretty substantially, which is just a very weird thing for an earnings acceleration.

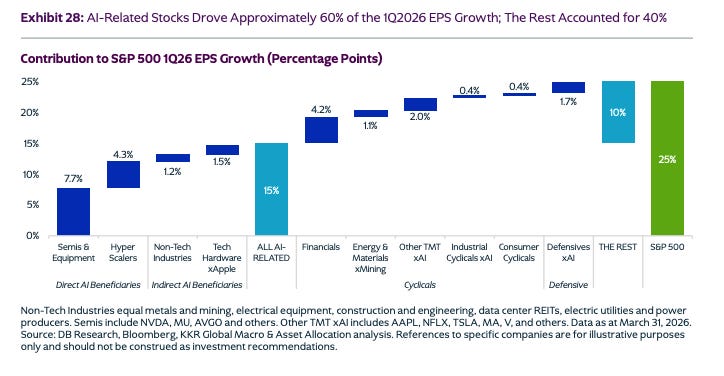

It’s somewhat less weird—and further evidence of the market’s “rationality,”—when you consider the narrowness of earnings growth. While it’s true that margin-expansion is expected to be pretty broad-based, the bulk of the earnings growth is concentrated in the AI buildout.

~60% of the S&P’s Q1 eps growth (15pp of 25pp total) is attributable to AI Capex mostly (plus some hyperscaler cloud acceleration).

In other words, profit growth is largely (but not entirely) a function of the largest companies ever spending north of a trillion dollars on traditionally cyclical hardware and services. But that’s still earnings growth—real profits, not just hoped-for profits.

Capexapalooza, but also caution

It’s actually a fun little exercise to think how big Capex could get.